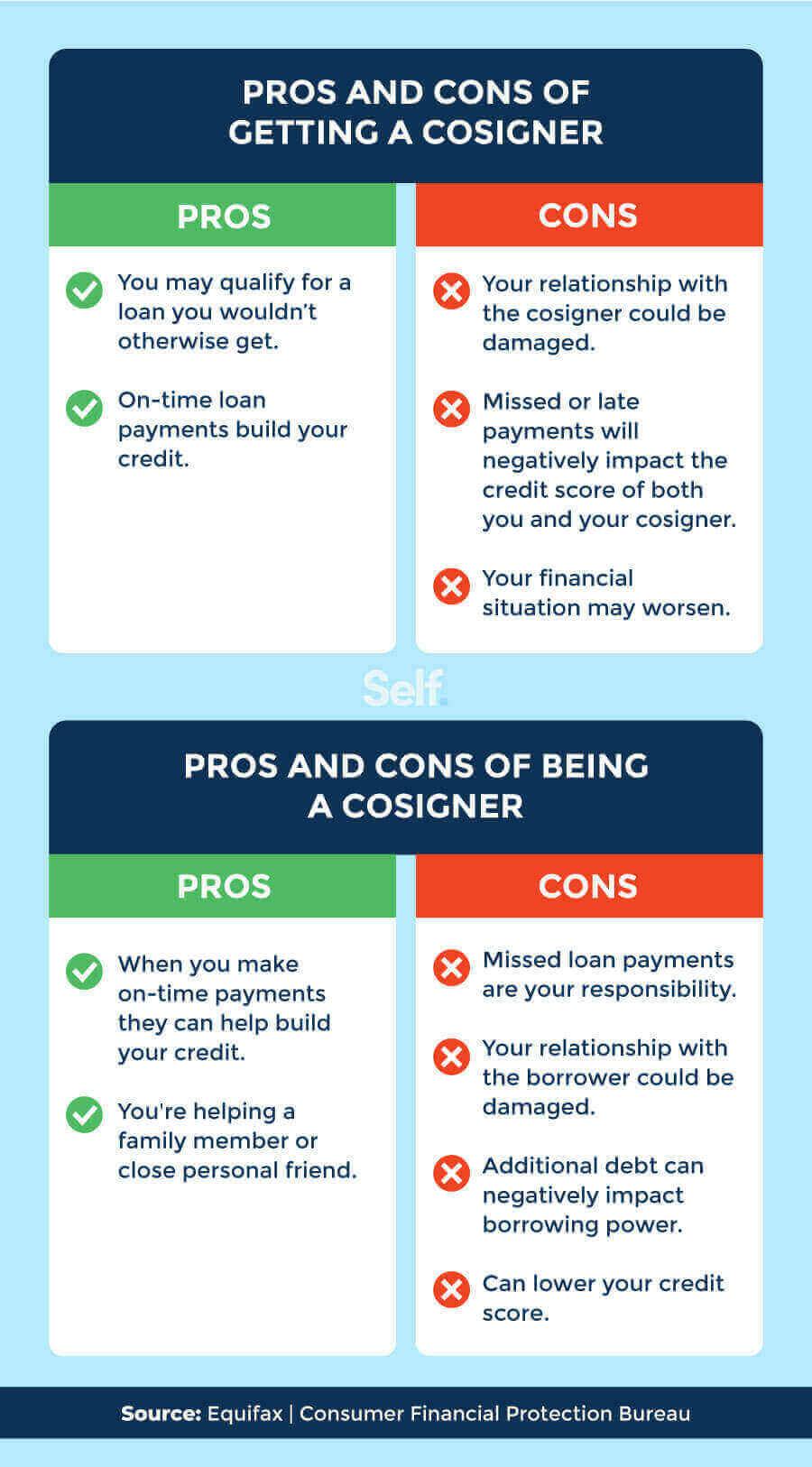

Are there any benefits to Cosigning?

Are there any benefits to being a cosigner

The benefits to the borrower

A cosigner might help: Get a reduced security deposit on an apartment lease. Get a lower interest rate and lower monthly payment on a loan for a car. Secure a mortgage with a lower interest rate.

CachedSimilar

What are the cons of being a co-signer

Cons of Cosigning a LoanIncreased responsibility — Once again, if you cosign for a loan, you are responsible for paying if the other party can't.Potentially strained relationship — Many personal relationships have been damaged or ended because of financial strain.

Cached

Is it smart to cosign

Co-signers also help prospective borrowers get a much lower interest rate on a loan than they could on their own. An ideal co-signer will likely have: A credit score of about 670 or higher, which is considered “good” by the two primary credit score analysts—FICO and VantageScore.

Cached

Does cosigning boost your credit

Having a co-signer on the loan will help the primary borrower build their credit score (as long as they continue to make on-time payments). It could also help the co-signer build their credit score and credit history, if the primary borrower makes on-time payments throughout the course of the loan.

Does co signing affect your taxes

Does cosigning for a house affect your taxes You can cosign for a house without impacting your tax situation. The person who lives in the home, your child, can take advantage of the tax-deductible expenses that come with homeownership. You won't be able to take those deductions.

Can I be removed as a cosigner

To get a co-signer release you will first need to contact your lender. After contacting them you can request the release — if the lender offers it. This is just paperwork that removes the co-signer from the loan and places you, the primary borrower, as the sole borrower on the loan.

How do I protect myself as a cosigner

5 ways to protect yourself as a co-signerServe as a co-signer only for close friends or relatives. A big risk that comes with acting as a loan co-signer is potential damage to your credit score.Make sure your name is on the vehicle title.Create a contract.Track monthly payments.Ensure you can afford payments.

How risky is it to cosign a car

Risks of cosigning

Credit risk: The auto loan will appear on both you and your cosigner's credit reports. If you miss a car payment or if the car is repossessed, you could do major damage to your cosigner's credit scores and cause them to be denied for loans and credit cards in the future.

Who gets the credit on a cosigned loan

Both the primary borrower and the cosigner on a loan will get credit if the primary borrower makes the payments on time. On the other hand, if the primary borrower does not keep up with the monthly payments, both their credit score and the cosigner's credit score will drop.

What are the pros and cons of cosigning

Pros and Cons of Cosigning a LoanPro: You're helping another person. Of course, you want your daughter to have a late-model car with all the newest safety features when she heads to college.Con: Your credit could take a hit.Con: You might get turned down for credit.Con: The relationship could go south.

What happens to cosigner if I don’t pay

If the borrower does not repay the loan, you may be forced to repay the whole amount of the loan, plus interest and any late fees that have accrued. With most cosigned loans, the lender is not required to pursue the main borrower first, but can request payment from the cosigner any time there is a missed payment.

Is it risky to be a cosigner

Whatever you cosign will show up on your credit report as if the loan is yours, which, depending on your credit history, may impact your credit scores. Cosigning a loan doesn't necessarily mean your finances or relationship with the borrower will be negatively affected, but it's not a decision you should make lightly.

Can a cosigner take your name off

Fortunately, you can have your name removed, but you will have to take the appropriate steps depending on the cosigned loan type. Basically, you have two options: You can enable the main borrower to assume total control of the debt or you can get rid of the debt entirely.

Why is it never a good idea to cosign a loan

Depending on how much debt you already have, the addition of the cosigned loan on your credit reports may make it look like you have more debt than you can handle. As a result, lenders may shy away from you as a borrower. It could lower your credit scores.

Can I remove myself as a cosigner

Fortunately, you can have your name removed, but you will have to take the appropriate steps depending on the cosigned loan type. Basically, you have two options: You can enable the main borrower to assume total control of the debt or you can get rid of the debt entirely.

How much of a difference does a co-signer make

A co-signer may increase your chance of approval, give you access to better loan terms and — over time — help you improve your credit score as you pay back your auto loan. Improve your chance of approval. A co-signer adds to your application if you don't have an extensive credit history or have a poor credit score.

Can I kick out my cosigner

In short, removing a cosigner is possible when: You can qualify for the loan or lease without the help of the cosigner. The lender or landlord allows for the cosigner to be removed, or. The lease is re-done or the loan refinanced, without the cosigner's name.

Can I remove myself from being a cosigner

Fortunately, you can have your name removed, but you will have to take the appropriate steps depending on the cosigned loan type. Basically, you have two options: You can enable the main borrower to assume total control of the debt or you can get rid of the debt entirely.

Will removing myself as a cosigner hurt my credit

Being removed as a cosigner from a loan with a positive payment history could potentially hurt your credit. How much will depend on your current credit history.

Whose credit score is used with a co-signer

Whose credit score is used when buying a car with a co-signer Lenders can consider the credit scores of both borrowers when co-signing an auto loan. If you have a lower credit score, having a co-signer with a higher score could work in your favor.