Can a cosigner ruin your credit?

Can being a cosigner hurt your credit

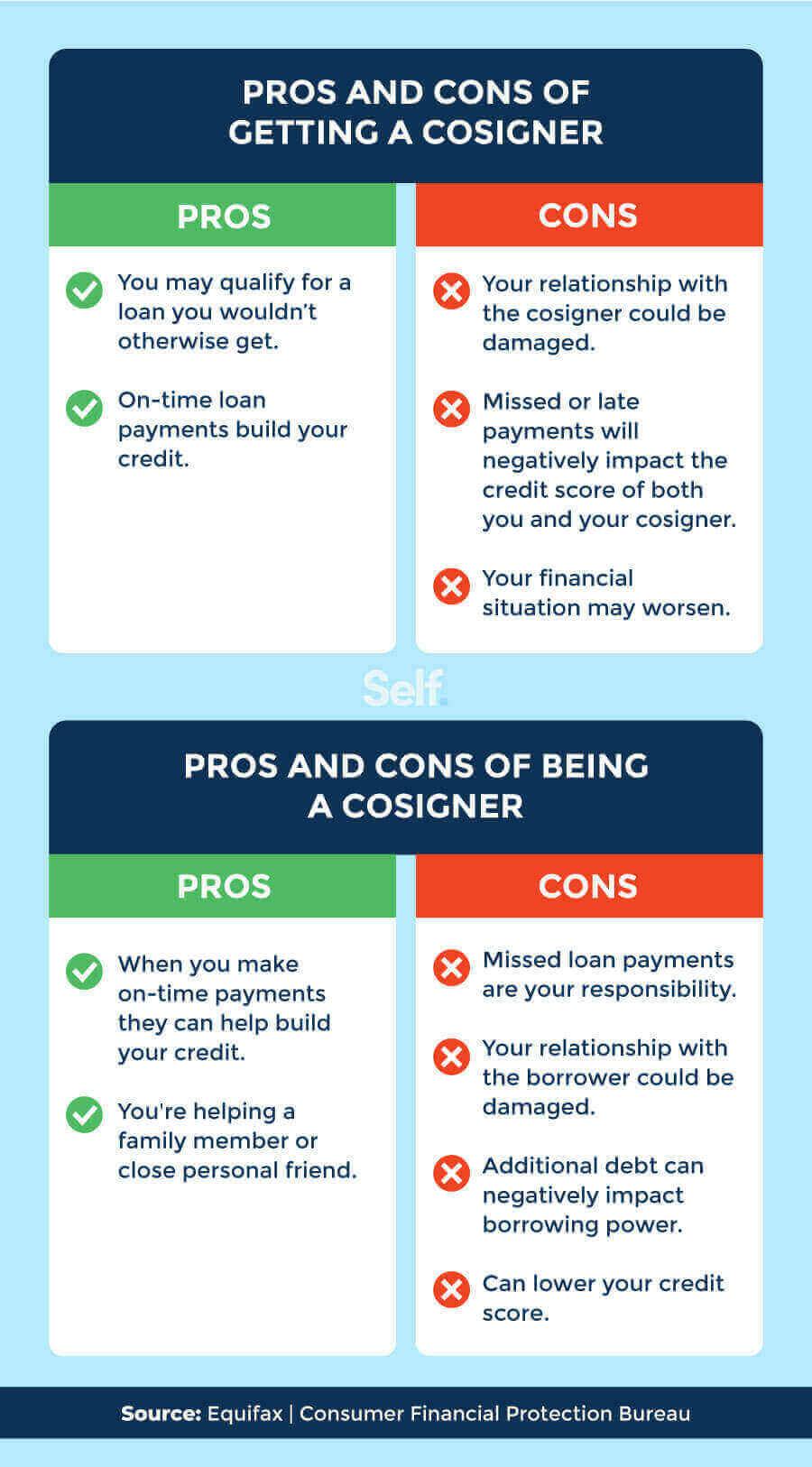

Whatever you cosign will show up on your credit report as if the loan is yours, which, depending on your credit history, may impact your credit scores. Cosigning a loan doesn't necessarily mean your finances or relationship with the borrower will be negatively affected, but it's not a decision you should make lightly.

Cached

Can a cosigner hurt your chances

Cosigning can affect your ability to get financing.

In addition to the impact on your credit scores, lenders may include the payments you cosigned for when calculating your debt-to-income (DTI) ratio. A high DTI can make getting a loan or line of credit more difficult.

Cached

Can a cosigner have worse credit than you

Cosigning a loan can affect the co-signer's credit score—for better or for worse. The loan will be added to the co-signer's credit history and impact their credit score.

What risk does a cosigner take

If you are asked to pay and cannot, you could be sued or your credit rating could be damaged. Consider that, even if you are not asked to repay the debt, your liability for this loan may keep you from getting other credit you may want.

Whose credit score is used if I have a cosigner

Whose credit score is used when co-signing In a co-signed loan, the co-signer's credit score has more weightage than the primary borrower. This is because the primary borrower will usually have poor credit and will depend on the co-signer's excellent credit to get lower rates.

Does cosigning still build credit

Having a co-signer on the loan will help the primary borrower build their credit score (as long as they continue to make on-time payments). It could also help the co-signer build their credit score and credit history, if the primary borrower makes on-time payments throughout the course of the loan.

Can you kick a cosigner out

But if your circumstances change over time or your credit score improves and you would like to remove the co-signer from your loan, there are three primary options. You can refinance, get a co-signer release or pay off the loan.

Can I kick out my cosigner

In short, removing a cosigner is possible when: You can qualify for the loan or lease without the help of the cosigner. The lender or landlord allows for the cosigner to be removed, or. The lease is re-done or the loan refinanced, without the cosigner's name.

Who gets the credit score if you have a cosigner

Co-signing a loan can help or hurt your credit scores. Having a co-signer on the loan will help the primary borrower build their credit score (as long as they continue to make on-time payments).

How do I protect myself as a cosigner

5 ways to protect yourself as a co-signerServe as a co-signer only for close friends or relatives. A big risk that comes with acting as a loan co-signer is potential damage to your credit score.Make sure your name is on the vehicle title.Create a contract.Track monthly payments.Ensure you can afford payments.

Is it bad to cosign for someone

Co-signing a loan may help the borrower qualify, but it could also hurt your credit score and overall finances.

Can I cosign with a 650 credit score

Typically, a cosigner needs a credit score of 670 or better to be approved. This range is usually classified as very good to excellent credit.

How much credit does a cosigner get

Being a co-signer itself does not affect your credit score. Your score may, however, be negatively affected if the main account holder misses payments.

Can you remove yourself as a cosigner

Fortunately, you can have your name removed, but you will have to take the appropriate steps depending on the cosigned loan type. Basically, you have two options: You can enable the main borrower to assume total control of the debt or you can get rid of the debt entirely.

Who gets the credit on a cosigned loan

Both the primary borrower and the cosigner on a loan will get credit if the primary borrower makes the payments on time. On the other hand, if the primary borrower does not keep up with the monthly payments, both their credit score and the cosigner's credit score will drop.

How do I remove a cosigner without refinancing

A loan assumption or modification could release a co-borrower from your mortgage without refinancing into a new loan. However, lenders aren't required to grant assumptions or modifications, so be willing to negotiate.

How soon can I remove myself as cosigner

There is no set procedure for getting out of being a cosigner. This is because your request to remove yourself will need to be approved by the lender (or you'll need to convince the primary borrower to take you off or adjust the loan).

Why is it risky to be a co-signer

The lender can sue the cosigner for interest, late fees, and any attorney's fees involved in collection. If the primary borrower falls on hard times financially and cannot make payments, AND the cosigner fails to make the payments, the lender may also decide to pursue garnishment of the wages of the cosigner.

Can I remove myself from being a cosigner

Fortunately, you can have your name removed, but you will have to take the appropriate steps depending on the cosigned loan type. Basically, you have two options: You can enable the main borrower to assume total control of the debt or you can get rid of the debt entirely.

Can I get a loan with a 500 credit score with a cosigner

Apply with a cosigner

The cosigner's credit and income impact the lender's decision more than those of the primary applicant, so it can help people with a credit score of 500 get approved for loans they might not normally qualify for.