Can having too many loans hurt your credit?

Does having many loan affect your credit score

What's more, if you apply for more loans after the 14- to 45-day period is up, it can actually hurt your credit score. Multiple applications outside a short rate-shopping period may indicate to the lender that you're a risky borrower.

Cached

Is it bad to have too many personal loans

Your credit score will be affected

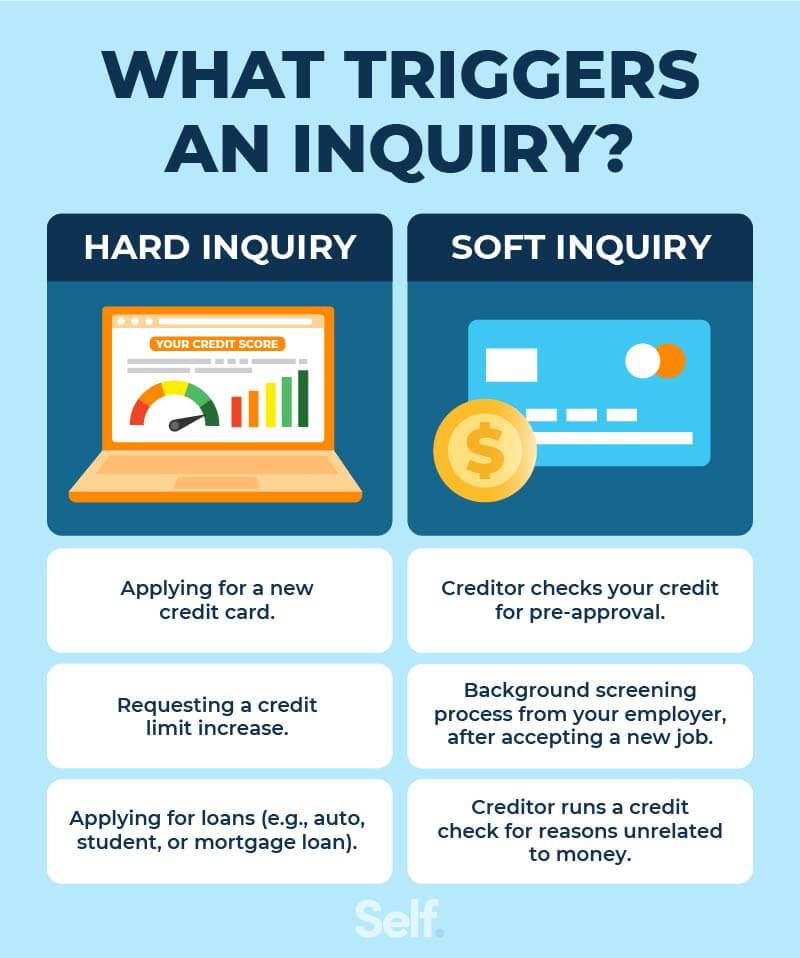

Another major downside to taking out multiple loans is their effect on your credit score. Inquiries on your credit report usually cause a small drop in your credit score. This drop might not appear immediately, but it will appear soon after you officially apply for the loan.

How many is too many loans

It depends on how you use and manage it. One guideline to determine whether you have too much debt is the 28/36 rule. The 28/36 rule states that no more than 28% of a household's gross income should be spent on housing and no more than 36% on housing plus debt service, such as credit card payments.

Is it bad to pay off a loan early

If you have personal loan debt and are in a financial position to pay it off early, doing so could save you money on interest and boost your credit score. That said, you should only pay off a loan early if you can do so without tilting your budget, and if your lender doesn't charge a prepayment penalty.

How many loan accounts is good for credit score

Credit bureaus suggest that five or more accounts — which can be a mix of cards and loans — is a reasonable number to build toward over time. Having very few accounts can make it hard for scoring models to render a score for you.

Is it bad to have 3 personal loans

If you apply for several loans in quick succession, the effect on your credit can multiply, and you could see a big dent in your score. (The hard inquiry happens whether your application is approved or not.) Just answer a few questions to get personalized rate estimates from multiple lenders.

Is it OK to have 3 loans

You can have as many personal loans as you want, provided your lenders approve them. They'll consider factors including how you are repaying your current loan(s), debt-to-income ratio and credit scores.

Is $2 000 in debt bad

$2,000 in credit card debt is manageable if you can make the minimum payments each month, or ideally more than that. But if it's hard to keep up with your payments, it's not manageable, and that debt can grow quickly due to interest charges.

Is it okay to have 3 personal loans

You can have as many personal loans as you want, provided your lenders approve them. They'll consider factors including how you are repaying your current loan(s), debt-to-income ratio and credit scores.

Is it better to pay off loans fast or slow

In most cases, paying off a loan early can save money, but check first to make sure prepayment penalties, precomputed interest or tax issues don't neutralize this advantage. Paying off credit cards and high-interest personal loans should come first. This will save money and will almost always improve your credit score.

Is it better to pay off a loan at once or over time

The faster you can pay off a loan, the less it will cost you in interest. If you can pay off a personal loan early, it can lower your total cost of borrowing, potentially saving you a considerable amount of money.

How to get 850 credit score

I achieved a perfect 850 credit score, says finance coach: How I got there in 5 stepsPay all your bills on time. One of the easiest ways to boost your credit is to simply never miss a payment.Avoid excessive credit inquiries.Minimize how much debt you carry.Have a long credit history.Have a good mix of credit.

How to get 900 credit score

7 ways to achieve a perfect credit scoreMaintain a consistent payment history.Monitor your credit score regularly.Keep old accounts open and use them sporadically.Report your on-time rent and utility payments.Increase your credit limit when possible.Avoid maxing out your credit cards.Balance your credit utilization.

Can you take out a loan to pay off another loan

Consumers often use personal loans for debt consolidation, which involves getting a loan and using it to pay off existing debt from other sources. The right personal loan can help you simplify your monthly bill paying and may save money in the long run—and that's exactly why you might choose debt consolidation.

Can you take out a loan if you already have one

Yes. Many lenders allow multiple outstanding personal loans. You can take out a personal loan from multiple banks or online lenders, as long as you qualify. If you already have a lot of outstanding debt, however, a lender might not approve you for an additional loan.

Is 30000 in loans bad

If you racked up $30,000 in student loan debt, you're right in line with typical numbers: the average student loan balance per borrower is $33,654. Compared to others who have six-figures worth of debt, that loan balance isn't too bad.

Is a 5000 loan a lot

So, $5,000 can be considered average, if not below average, for a new personal loan. For example, OneMain offers personal loans from $1,500 to $20,000.

Is $15000 a lot of debt

It's not at all uncommon for households to be swimming in more that twice as much credit card debt. But just because a $15,000 balance isn't rare doesn't mean it's a good thing. Credit card debt is seriously expensive. Most credit cards charge between 15% and 29% interest, so paying down that debt should be a priority.

Is $30,000 in debt a lot

Many people would likely say $30,000 is a considerable amount of money. Paying off that much debt may feel overwhelming, but it is possible. With careful planning and calculated actions, you can slowly work toward paying off your debt. Follow these steps to get started on your debt-payoff journey.

Why did my credit score drop 40 points after paying off debt

It's possible that you could see your credit scores drop after fulfilling your payment obligations on a loan or credit card debt. Paying off debt might lower your credit scores if removing the debt affects certain factors like your credit mix, the length of your credit history or your credit utilization ratio.