Can I get preapproved for a mortgage without a hard inquiry?

Does prequalification require a hard pull

Prequalification is typically considered a soft inquiry, and it won't hurt your credit all on its own. In fact, it can be a helpful tool for lowering your risk of being rejected for a new credit card.

Does mortgage pre approval require hard pull

Yes, a pre-approval is a hard inquiry. Applying for a pre-approval through a mortgage lender is a standard step in the mortgage approval process because it involves lenders looking at more detailed information. Because lenders give loans for large amounts of money, hard inquiry credit checks are routine.

Cached

How to get mortgage pre approval without affecting credit score

Get prequalified for a mortgage

To prequalify you for a loan, lenders check your credit report, but conduct a “soft” inquiry, or soft pull, in which they prescreen your report without it affecting your score.

Cached

How many pre approvals can I get without hurting my credit

While many home buyers will only need one mortgage preapproval letter, there really is no limit to the number of times you can get preapproved. In fact, you can — and should — get preapproved with multiple lenders. Many experts recommend getting at least three preapproval letters from three different lenders.

Which is stronger prequalification or preapproval

This means a preapproval is a stronger sign of what you can afford and adds more credibility to your offer than a prequalification. This will also allow you to show sellers a preapproval letter to demonstrate that your financial information has been verified and you can afford a mortgage.

Do they run your credit to get pre qualified

For some prequalifications, lenders will check your credit through a soft inquiry—the type of inquiry that doesn't impact your credit scores. Once you're prequalified, you can choose to apply and undergo a complete review process.

What would stop you from getting pre-approved for a mortgage

Too High of a Debt to Income Ratio

Most lenders want a debt to income ratio of 36% for all of your debt, and 28% for your housing. If lenders look at how much you're making and you don't fit in those numbers, and you don't have enough for a mortgage payment, it's possible that you not be pre-approved for a mortgage.

What should your credit score be to get pre-approved for a mortgage

620

It's helpful to know where you stand before reaching out to a lender. A credit score of at least 620 is recommended to qualify for a mortgage, and a higher one will qualify you for better rates. Generally, a credit score of 740 or above will enable you to qualify for the best mortgage rates.

What is a good credit score to get pre-approved for a mortgage

620 or higher

It's recommended you have a credit score of 620 or higher when you apply for a conventional loan. If your score is below 620, lenders either won't be able to approve your loan or may be required to offer you a higher interest rate, which can result in higher monthly payments.

How far in advance should I get pre-approved for a mortgage

The best time to get pre-approved for a mortgage is at least one year before you decide to purchase. As a home buyer, pre-approvals are for your benefit, so it's never too early to get one. Getting pre-approved early is an advantage because one-third of mortgage applications contain an error.

What percent of pre-approved mortgages get denied

But you might not get a mortgage at all, if you fall into some of these traps: According to a NerdWallet report that looked at mortgage application data, 8% of mortgage applications were denied, and there were 58,000 more denials in 2023 than 2023 (though, to be fair, there were also more mortgage applications).

Do lenders run credit for preapproval

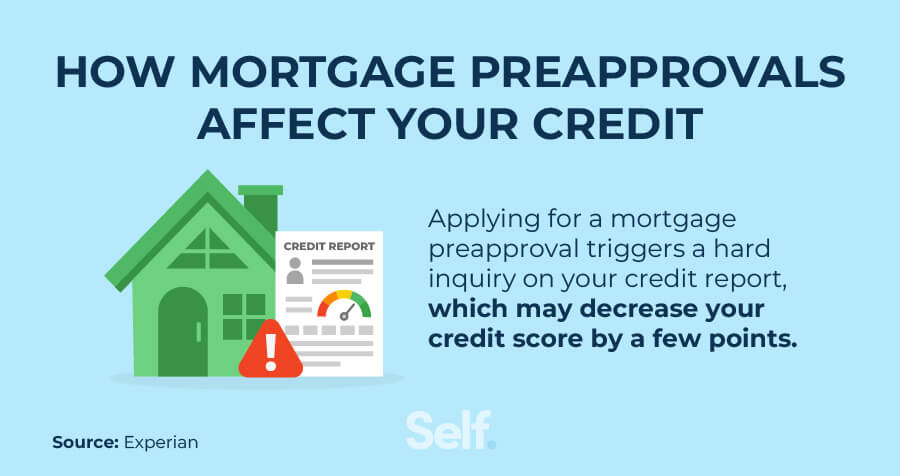

A mortgage preapproval can have a hard inquiry on your credit score if you end up applying for the credit. Although a preapproval may affect your credit score, it plays an important step in the home buying process and is recommended to have. The good news is that this ding on your credit score is only temporary.

Which is better prequalified and pre-approved

The biggest difference between the two is that getting pre-qualified is typically a faster and less detailed process, while pre-approvals are more comprehensive and take longer. Getting a pre-qualification or pre-approval letter is generally not a guarantee that you will secure a loan from the lender.

How often do preapproved mortgages get denied

You may be wondering how often underwriters denies loans According to the mortgage data firm HSH.com, about 8% of mortgage applications are denied, though denial rates vary by location and loan type. For example, FHA loans have different requirements that may make getting the loan easier than other loan types.

Do they run your credit for mortgage pre-approval

A mortgage preapproval can have a hard inquiry on your credit score if you end up applying for the credit. Although a preapproval may affect your credit score, it plays an important step in the home buying process and is recommended to have. The good news is that this ding on your credit score is only temporary.

What credit score is needed to buy a 300k house

620-660

Additionally, you'll need to maintain an “acceptable” credit history. Some mortgage lenders are happy with a credit score of 580, but many prefer 620-660 or higher.

What FICO score is used for mortgages

FICO Score 5

While most lenders use the FICO Score 8, mortgage lenders use the following scores: Experian: FICO Score 2, or Fair Isaac Risk Model v2. Equifax: FICO Score 5, or Equifax Beacon 5. TransUnion: FICO Score 4, or TransUnion FICO Risk Score 04.

What is the minimum credit score to buy a house for the first time

620 or higher

Conventional Loan Requirements

It's recommended you have a credit score of 620 or higher when you apply for a conventional loan. If your score is below 620, lenders either won't be able to approve your loan or may be required to offer you a higher interest rate, which can result in higher monthly payments.

What are the 3 steps to get pre-approved for a mortgage

How to get preapproved for a mortgageStep 1: Gather your documents. Your lender will require documentation to support the information in your loan application.Step 2: Complete a preapproval application.Step 3: Wait for you lender to process the preapproval.

Is it better to be preapproved or prequalified

This means a preapproval is a stronger sign of what you can afford and adds more credibility to your offer than a prequalification. This will also allow you to show sellers a preapproval letter to demonstrate that your financial information has been verified and you can afford a mortgage.