Can I prequalify without hurting my credit?

Does it hurt your credit to prequalify

Prequalifying, or preapproval (card issuers use these terms interchangeably), won't have any effect on your credit score — that happens once you formally apply. Keep in mind, however, that just because you've prequalified for a credit card, it doesn't guarantee approval when you submit your official application.

Can you get a pre-approval without pulling credit

With a prequalification, you won't have to provide as much information about your finances, and your lender won't pull your credit. Without your credit report, your lender can only give you rough estimates. This means the approval amount, loan program and interest rate might change as the lender gets more information.

How do I get pre-approved without affecting my credit score

Get prequalified for a mortgage

To prequalify you for a loan, lenders check your credit report, but conduct a “soft” inquiry, or soft pull, in which they prescreen your report without it affecting your score.

Cached

Will I get approved if I prequalify

When a credit card offer mentions that someone is pre-qualified or pre-approved, it typically means they've met the initial criteria required to become a cardholder. But they still need to apply and get approved. Think of these offers as invitations to start the actual application process.

How much does your credit drop when you get pre-approved

five points

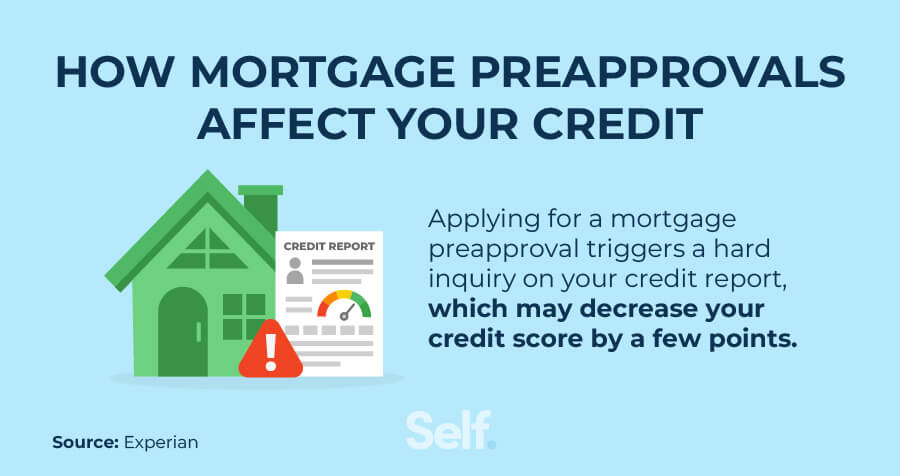

The pre-approval typically requires a hard credit inquiry, which decreases a buyer's credit score by five points or less.

What’s better pre qualified vs pre-approved

The biggest difference between the two is that getting pre-qualified is typically a faster and less detailed process, while pre-approvals are more comprehensive and take longer. Getting a pre-qualification or pre-approval letter is generally not a guarantee that you will secure a loan from the lender.

What is the difference between pre-approved and pre qualified

The biggest difference between the two is that getting pre-qualified is typically a faster and less detailed process, while pre-approvals are more comprehensive and take longer. Getting a pre-qualification or pre-approval letter is generally not a guarantee that you will secure a loan from the lender.

Is a pre qualification a hard inquiry

Prequalification is typically considered a soft inquiry, and it won't hurt your credit all on its own. In fact, it can be a helpful tool for lowering your risk of being rejected for a new credit card.

Why did my credit score drop after pre-approval

This occurs when a lender is considering extending a line of credit to you. Hard inquiries show up on your credit report and can affect your credit scores. For example, if you apply for a pre-approval offer, it will trigger a hard inquiry, and you could see a dip in your credit scores.

How many hard inquiries is too many

There's no such thing as “too many” hard credit inquiries, but multiple applications for new credit accounts within a short time frame could point to a risky borrower. Rate shopping for a particular loan, however, may be treated as a single inquiry and have minimal impact on your creditworthiness.

Which is stronger prequalification or preapproval

This means a preapproval is a stronger sign of what you can afford and adds more credibility to your offer than a prequalification. This will also allow you to show sellers a preapproval letter to demonstrate that your financial information has been verified and you can afford a mortgage.

What’s better prequalified or preapproved

The biggest difference between the two is that getting pre-qualified is typically a faster and less detailed process, while pre-approvals are more comprehensive and take longer. Getting a pre-qualification or pre-approval letter is generally not a guarantee that you will secure a loan from the lender.

What is the disadvantage of prequalification

Time-consuming process: Prequalification can be a time-consuming process, requiring the GC to collect and review a significant amount of information from potential partners. This can result in delays in the procurement process and potentially impact project timelines.

How long does prequalification last

– 90 days

Most mortgage preapproval letters last between 60 – 90 days. Your mortgage preapproval will list how much you're approved to borrow, your interest rate and other terms and conditions. Typically, borrowers should wait until they're ready to actively search for a home before they get preapproved.

Does pre qualified mean approved for a car loan

Worth noting, prequalification doesn't mean your loan has been approved — you'll still have to formally apply for it with your lender. It should, however, provide some clarity on what you may be approved for.

Why did my credit score drop 40 points after paying off debt

It's possible that you could see your credit scores drop after fulfilling your payment obligations on a loan or credit card debt. Paying off debt might lower your credit scores if removing the debt affects certain factors like your credit mix, the length of your credit history or your credit utilization ratio.

Why is my credit score going down if I pay everything on time

A short credit history gives less to base a judgment on about how you manage your credit, and can cause your credit score to be lower. A combination of these and other issues can add up to high credit risk and poor credit scores even when all of your payments have been on time.

How long should I wait between hard inquiries

Bottom line. Generally, it's a good idea to wait about six months between credit card applications. Since applying for a new credit card will result in a slight reduction to your credit score, multiple inquiries could lead to a significantly decrease.

Do hard inquiries go away if approved

Hard inquiries serve as a timeline of when you have applied for new credit and may stay on your credit report for two years, although they typically only affect your credit scores for one year. Depending on your unique credit history, hard inquiries could indicate different things to different lenders.

Can you be denied after prequalification

Yes, it's possible to have your loan application denied after getting preapproved for a mortgage. It doesn't seem fair, but the reason this is possible is because your loan has to go through the underwriting process before it's finalized.