Can you pay payoff loans off early?

What happens if you pay off a loan early

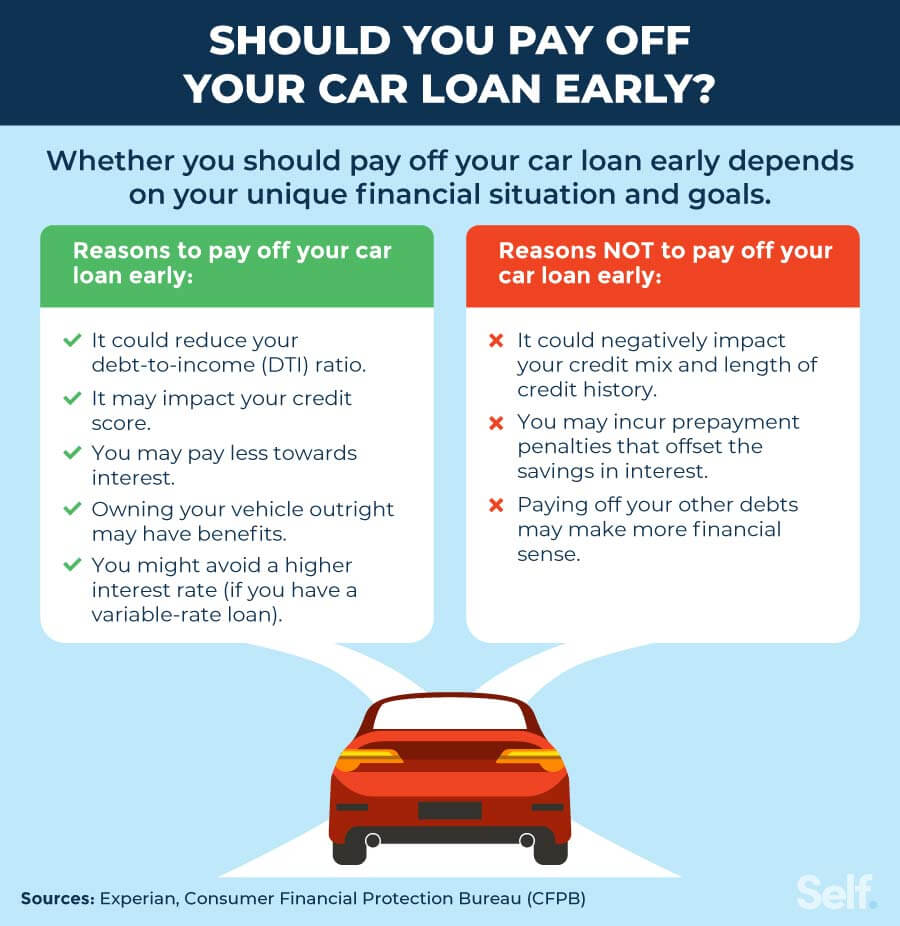

Paying off the loan early can put you in a situation where you must pay a prepayment penalty, potentially undoing any money you'd save on interest, and it can also impact your credit history.

Does payoff hurt your credit

Paying off your only line of installment credit reduces your credit mix and may ultimately decrease your credit scores. Similarly, if you pay off a credit card debt and close the account entirely, your scores could drop.

What are the disadvantages of paying off a car loan early

The lender makes money from the interest you pay on your loan each month. Repaying a loan early usually means you won't pay any more interest, but there could be an early prepayment fee. The cost of those fees may be more than the interest you'll pay over the rest of the loan.

Cached

Is payoff a good idea

Payoff is legit and may be worthwhile

In some cases, it can be helpful, but only if the loan's APR, which can range from 5.99% to 24.99%, is lower than the credit cards you intend to pay off. Also, it's only beneficial if you can afford the monthly payment.

Why do you get penalized for paying off a loan early

A mortgage prepayment penalty is a fee that some lenders charge when you pay all or part of your mortgage loan off early. The penalty fee is an incentive for borrowers to pay back their principal slowly over a longer term, allowing mortgage lenders to collect interest.

What is the fastest way to pay off a loan

Pay off your most expensive loan first.

Then, continue paying down debts with the next highest interest rates to save on your overall cost. This is sometimes referred to as the “avalanche method” of paying down debt.

Is it better to pay off bad debt or settle it

It's better to pay off a debt in full (if you can) than settle. Summary: Ultimately, it's better to pay off a debt in full than settle. This will look better on your credit report and help you avoid a lawsuit. If you can't afford to pay off your debt fully, debt settlement is still a good option.

Why is loan payoff higher than balance

Your current balance might not reflect how much you actually have to pay to completely satisfy the loan. Your payoff amount also includes the payment of any interest you owe through the day you intend to pay off your loan. The payoff amount may also include other fees you have incurred and have not yet paid.

What happens if I pay an extra $100 a month on my car loan

Your car payment won't go down if you pay extra, but you'll pay the loan off faster. Paying extra can also save you money on interest depending on how soon you pay the loan off and how high your interest rate is.

Is it smarter to pay off a car loan early

The bottom line

Paying off a car loan early can save you money — provided the lender doesn't assess too large a prepayment penalty and you don't have other high-interest debt. Even a few extra payments can go a long way to reducing your costs.

Does payoff charge a fee

Payoff doesn't charge any application, prepayment, late payment, or annual fees, but you will have to pay a loan origination fee if your application is accepted and you receive a loan. There are other lenders that do not charge origination fees, but they tend to focus on good credit borrowers.

How long does a payoff take to hit your credit

How long does it take for my credit score to update after paying off debt It can often take as long as one to two months for debt payment information to be reflected on your credit score. This has to do with both the timing of credit card and loan billing cycles and the monthly reporting process followed by lenders.

How much is a early payoff penalty

The penalty can be 2 percent of your loan balance within the loan's first two years and 1 percent of your loan balance in year three. For example, say you want to sell your home only one year after you took out a non-conforming mortgage loan to purchase it.

Can you pay off a 72 month car loan early

Some lenders make it difficult to pay off car loans early because they'll receive less payment in interest. If your lender does allow early payoff, ask whether there's a prepayment penalty, since a penalty could reduce any interest savings you'd gain.

How to pay off a $30,000 loan fast

5 Ways To Pay Off A Loan EarlyMake bi-weekly payments. Instead of making monthly payments toward your loan, submit half-payments every two weeks.Round up your monthly payments.Make one extra payment each year.Refinance.Boost your income and put all extra money toward the loan.

What is the smartest way to pay off a loan

Pay off your most expensive loan first.

Then, continue paying down debts with the next highest interest rates to save on your overall cost. This is sometimes referred to as the “avalanche method” of paying down debt.

Is it bad to pay off debt in full

It's a good idea to pay off your credit card balance in full whenever you're able. Carrying a monthly credit card balance can cost you in interest and increase your credit utilization rate, which is one factor used to calculate your credit scores.

What’s the most reliable way to pay off debt

Pay off your debt and save on interest by paying more than the minimum every month. The key is to make extra payments consistently so you can pay off your loan more quickly. Some lenders allow you to make an extra payment each month specifying that each extra payment goes toward the principal.

Is it better to pay off loans faster or slower

Saving Money on Interest

The longer you pay, the more it costs. So, the quicker you pay off your loan, the less you ultimately spend on your purchase. This is especially the case with credit cards or other high-interest debt. It's a terrible idea to make only the minimum monthly payment.

Is it better to pay off a loan all at once or over time

The faster you can pay off a loan, the less it will cost you in interest. If you can pay off a personal loan early, it can lower your total cost of borrowing, potentially saving you a considerable amount of money.