Do credit screenings affect credit score?

Do credit checks hurt your credit score

Good news: Credit scores aren't impacted by checking your own credit reports or credit scores. In fact, regularly checking your credit reports and credit scores is an important way to ensure your personal and account information is correct, and may help detect signs of potential identity theft.

What does a credit screening do

Credit screening is the process of gathering information from credit agencies and public records in order to verify submitted information and look for red flags so that you can properly evaluate the financial stability and reliability of potential tenants.

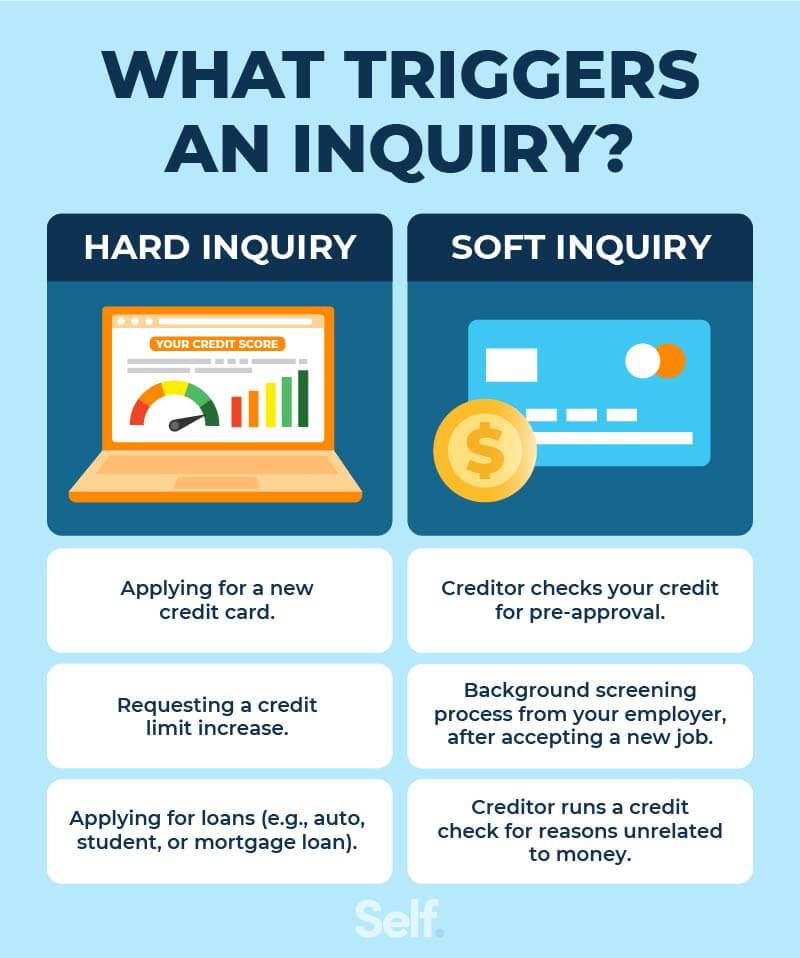

What credit check won t affect my score

A current creditor checks your credit.

Because this is not a new lender peeking into your financial history, it won't hurt your score.

How many credit checks hurt your credit score

Often no points are subtracted. However, multiple hard inquiries can deplete your score by as much as 10 points each time they happen. People with six or more recent hard inquiries are eight times as likely to file for bankruptcy than those with none.

What hurts credit score the most

1. Payment History: 35% Your payment history carries the most weight in factors that affect your credit score, because it reveals whether you have a history of repaying funds that are loaned to you.

What are 3 things that hurt your credit score

5 Things That May Hurt Your Credit ScoresHighlights:Making a late payment.Having a high debt to credit utilization ratio.Applying for a lot of credit at once.Closing a credit card account.Stopping your credit-related activities for an extended period.

What does it mean when a credit screening is rejected

The term credit denial refers to the rejection of a credit application by a prospective lender. Financial companies issue denials to applicants who aren't creditworthy. The majority of denials are the result of previous blemishes on a borrower's credit history.

What factor most greatly affects your credit score

Payment history

1. Payment history. Payment history is the most important factor influencing your credit score – accounting for 35% of the total score.

How many times can you check your credit score without hurting your credit

How Often Can You Check Your Credit Score You can check your credit score as often as you want without hurting your credit, and it's a good idea to do so regularly. At the very minimum, it's a good idea to check before applying for credit, whether it's a home loan, auto loan, credit card or something else.

Is 700 a good credit score

For a score with a range between 300 and 850, a credit score of 700 or above is generally considered good. A score of 800 or above on the same range is considered to be excellent. Most consumers have credit scores that fall between 600 and 750. In 2023, the average FICO® Score☉ in the U.S. reached 714.

What is the #1 way to hurt your credit score

Making a late payment

Your payment history on loan and credit accounts can play a prominent role in calculating credit scores; depending on the scoring model used, even one late payment on a credit card account or loan can result in a decrease.

Why is 850 the highest credit score

Your 850 FICO® Score is nearly perfect and will be seen as a sign of near-flawless credit management. Your likelihood of defaulting on your bills will be considered extremely low, and you can expect lenders to offer you their best deals, including the lowest-available interest rates.

What 5 things are worst for your credit rating

Here are 10 things you may not have known could hurt your credit score:Just one late payment.Not paying ALL of your bills on time.Applying for more credit.Canceling your zero-balance credit cards.Transferring balances to a single card.Co-signing credit applications.Not having enough credit diversity.

How bad does getting denied credit hurt score

Being denied for a credit card doesn't hurt your credit score. But the hard inquiry from submitting an application can cause your score to decrease. Submitting a credit card application and receiving notice that you're denied is a disappointment, especially if your credit score drops after applying.

What are the 3 main reasons why credit applicants can be declined credit

Main reasons your credit card application can be deniedYour credit score is too low. Credit cards are often denied because the applicant's credit score is too low.Your income is too low.You have a negative credit history.You've applied for too much new credit.You picked a card that has application restrictions.

What can hurt credit score

Here are 10 things you may not have known could hurt your credit score:Just one late payment.Not paying ALL of your bills on time.Applying for more credit.Canceling your zero-balance credit cards.Transferring balances to a single card.Co-signing credit applications.Not having enough credit diversity.

What are the 3 C’s of credit

Students classify those characteristics based on the three C's of credit (capacity, character, and collateral), assess the riskiness of lending to that individual based on these characteristics, and then decide whether or not to approve or deny the loan request.

Do multiple hard inquiries count as one

If you're shopping for a new auto or mortgage loan or a new utility provider, the multiple inquiries are generally counted as one inquiry for a given period of time. The period of time may vary depending on the credit scoring model used, but it's typically from 14 to 45 days.

How often is too often to check your credit score

The CFPB recommends you review your credit reports at least once a year. However, reviewing your credit history and open credit accounts more frequently can give you a more accurate picture of your financial standing, so you may want to consider checking one of your free credit reports every four months.

How to get 800 credit score in 45 days

Here are 10 ways to increase your credit score by 100 points – most often this can be done within 45 days.Check your credit report.Pay your bills on time.Pay off any collections.Get caught up on past-due bills.Keep balances low on your credit cards.Pay off debt rather than continually transferring it.