Do they check your credit on closing day?

How many days before closing do they pull your credit

Lenders will typically pull your credit within seven days before closing. However, most lenders will only check with a “soft credit inquiry,” so your credit score won't be affected.

Cached

Why do lenders pull credit day of closing

Before closing, the lender will pull a final monitoring report from the credit bureaus to determine whether you incurred any new debt. Any new accounts must be added to your debt-to-income ratio, potentially impacting the original loan terms or even causing the loan to be denied.

Do lenders check your bank account the day of closing

Yes, they do. One of the final and most important steps toward closing on your new home mortgage is to produce bank statements showing enough money in your account to cover your down payment, closing costs, and reserves if required.

Cached

What happens if your credit score goes up before closing

The mortgage lender may need to send your application back to an underwriter for a second review. If there are major concerns raised by a change in your credit score, this can cause you to lose the loan. It's crucial not to mess with your credit during the application process.

Cached

Can you get clear to close the day of closing

Most buyers won't have to wait very long to meet at the closing table once they're clear to close. With that in mind, you should expect at least a 3-day buffer between the time you receive your Closing Disclosure and the day you close.

What happens 3 days before closing

Your lender is required to send you a Closing Disclosure that you must receive at least three business days before your closing. It's important that you carefully review the Closing Disclosure to make sure that the terms of your loan are what you are expecting.

Can a loan be denied on closing day

Can a mortgage be denied after the closing disclosure is issued Yes. Many lenders use third-party “loan audit” companies to validate your income, debt and assets again before you sign closing papers. If they discover major changes to your credit, income or cash to close, your loan could be denied.

Should I pay credit before closing date

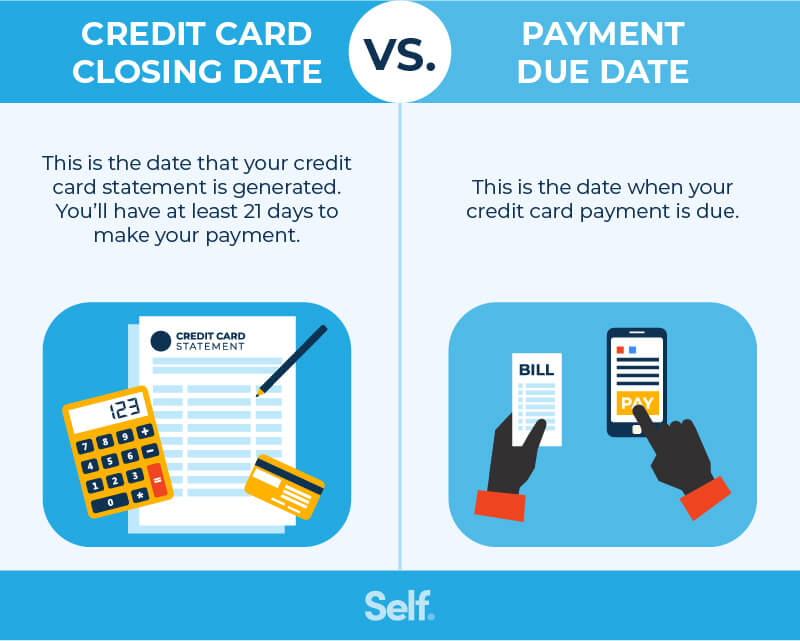

To avoid paying interest and late fees, you'll need to pay your bill by the due date. But if you want to improve your credit score, the best time to make a payment is probably before your statement closing date, whenever your debt-to-credit ratio begins to climb too high.

What do lenders look at right before closing

First, your lender will want to see verification of your income and assets, such as pay stubs and recent bank statements. Then you'll need to present your current debt and monthly expenses, which can help your lender determine your debt-to-income ratio.

Can your loan be denied after closing

Can a mortgage be denied after the closing disclosure is issued Yes. Many lenders use third-party “loan audit” companies to validate your income, debt and assets again before you sign closing papers. If they discover major changes to your credit, income or cash to close, your loan could be denied.

Do lenders do a soft pull before closing

Final credit check before closing

Also, if there are any new credit inquiries, we'll need verify what new debt, if any, resulted from the inquiry. This can affect your debt-to-income ratio, which can also affect your loan eligibility. This is known as a soft pull.

Can a loan be denied after clear to close

Clear-to-close buyers aren't usually denied after their loan is approved and they've signed the Closing Disclosure. But there are circumstances where a lender may decline an applicant at this stage. These rejections are usually caused by drastic changes to your financial situation.

What is the 7 day closing rule

Under the TRID rule, the creditor must deliver or place in the mail the initial Loan Estimate at least seven business days before consummation, and the consumer must receive the initial Closing Disclosure at least three business days before consummation.

What happens 24 hours before closing

Final walkthrough: Not to be confused with a home inspection, the final walkthrough—which your real estate agent will schedule—typically happens 24 hours before closing. At this point, all the seller's belongings should be completely cleared out, except for anything you agreed to keep.

What can cause a closing to fall through

What Can Cause A Mortgage Loan To Fall ThroughFunding Denied Because You Financed A Big Purchase.Funding Denied Because You Applied For More Credit.Job Change or Loss of Employment.Home Appraisal Came Back Lower Than Purchase Price.Home Inspection Revealed Major Problems.Seller Delayed Closing Date Due To Title Issues.

Can lender cancel after closing

In general, a lender cannot cancel a loan after closing unless there are specific circumstances outlined in the loan agreement or if fraud or misrepresentation is discovered. Once the loan has been closed and funded, the lender has typically committed the funds and established the mortgage lien on the property.

What happens if I don t pay my credit card before the closing date

Depending on your issuer and your account terms, the lender may apply a penalty annual percentage rate (APR) to your account if it's been 60 days without a payment. In general, card issuers report late payments every 30 days. Late payments are only one of several factors that impact credit scores.

How does closing date affect first payment

Since mortgages are paid in arrears and on the first of the month, your first mortgage payment typically comes at the start of the new month after you've lived in your new home for 30 days. This means that if you close on your house on May 25, your first payment is due July 1.

Will lender pull credit before closing

The answer is yes. Lenders pull borrowers' credit at the beginning of the approval process, and then again just prior to closing.

Do lenders run your credit again before closing

A question many buyers have is whether a lender pulls your credit more than once during the purchase process. The answer is yes. Lenders pull borrowers' credit at the beginning of the approval process, and then again just prior to closing.