Do VA loans have income limits?

Does income matter when using VA loan

The debt-to-income ratio determines if you can qualify for VA loans. The acceptable debt-to-income ratio for a VA loan is 41%. Generally, debt-to-income ratio refers to the percentage of your gross monthly income that goes towards debts. In fact, it is the ratio of your monthly debt obligations to gross monthly income.

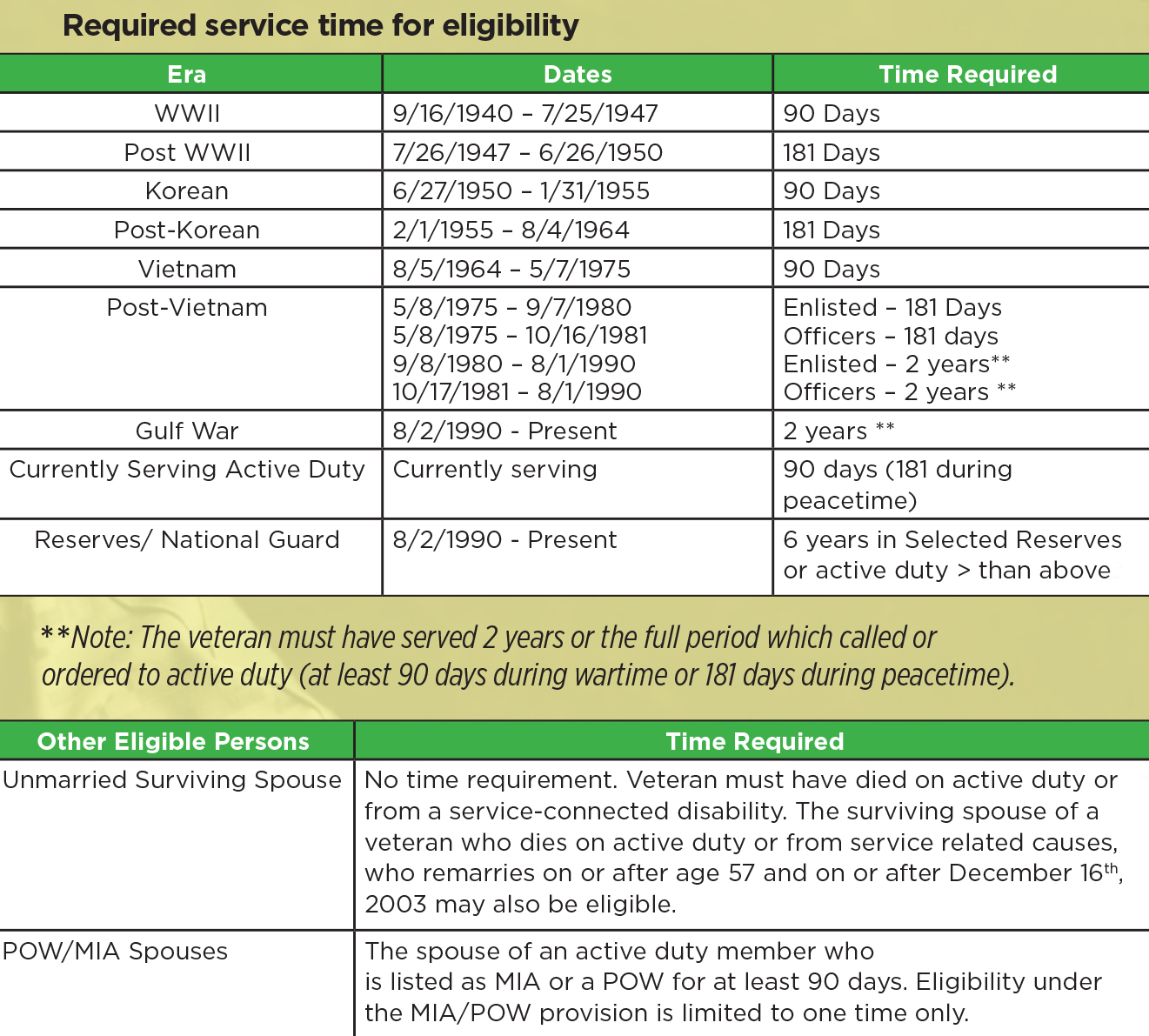

How many years of income do you need for a VA loan

two years

The VA requires that you must be able to show two years of consistent income, preferably documented through W-2s. If there are any gaps in employment in this two-year period, they must be substantiated.

What disqualifies me from the VA loan

Dishonorable Discharge

Veteran status requires that service members are discharged or released from the military under conditions other than dishonorable. A veteran with a dishonorable discharge will not be eligible to participate in the VA Loan Guaranty program.

How much do I need to make to buy a $300 K house with VA loan

To purchase a $300K house, you may need to make between $50,000 and $74,500 a year. This is a rule of thumb, and the specific salary will vary depending on your credit score, debt-to-income ratio, type of home loan, loan term, and mortgage rate.

What income is too high for VA benefits

VA Income Limits 2023

In 2023, the VA National Income Thresholds were as follows: $34,616 or less if you have no dependents. $41,539 or less if you have one dependent. $43,921 or less if you have two dependents.

Can you get VA benefits with too much income

No, you can not make too much money to get VA benefits.

The VA has no restrictions on the earning or income status of veterans that want to receive VA benefits. VA benefits are available to any veteran who the VA has determined to have a service-related condition that negatively impacts their health.

How many months of income do you need for a VA home loan

The VA requires that you show two years of consistent income, although they do not need to be from one job or position. Breaks between employment must be substantiated. Lenders often need to document at least a two-year work history as well.

What are the disadvantages of a VA loan

What are the Cons of a VA LoanRequired VA funding fee. One disadvantage of a VA loan is the additional cost of the VA Funding Fee.Tighter occupancy requirements.Stricter appraisal requirements.Less equity without a down payment.For homeownership only.

Can you be turned down for a VA loan

VA loan denial isn't uncommon. According to HMDA data, 12% of VA loan applications received a denial in Q2 of 2023, compared to 17% of FHA loans. While not uncommon, many scenarios may be preventable.

Why would a VA loan not be approved

In the overwhelming majority of cases, inexperienced loan officers or strict overlays are the reason for being denied for a VA loan. If your lender is not approved to do manual underwriting on VA home loans, you may be told you're not approved without further explanation or options.

Can I afford a 300k house on a $70 K salary

Home buying with a $70K salary

If you're an aspiring homeowner, you may be asking yourself, “I make $70,000 a year: how much house can I afford” If you make $70K a year, you can likely afford a home between $290,000 and $360,000*.

How much do you have to make a year to afford a $400000 house

$105,864 each year

Assuming a 30-year fixed conventional mortgage and a 20 percent down payment of $80,000, with a high 6.88 percent interest rate, borrowers must earn a minimum of $105,864 each year to afford a home priced at $400,000. Based on these numbers, your monthly mortgage payment would be around $2,470.

Does the VA have a salary cap

This legislation comes less than a year after the passage of the RAISE Act, which boosted the salary cap for VA nurses to $203,000. According to VA, this led to almost immediate pay increases for nearly 10,000 nurses. The CAREERS Act includes other ways to make the VA more appealing to potential recruits.

Does VA allow you to gross up income

The VA allows lenders to “gross up” a borrower's income, effectively adjusting non-taxable income upward. This pre-tax, or gross, figure can be used to qualify Veterans who receive tax-exempt income for a higher loan amount.

What is countable income for VA benefits

Your countable income is how much you earn, including your salary, investment and retirement payments, and any income you may have from your dependents. Some expenses, like non-reimbursable medical expenses (paid medical expenses not covered by your insurance provider), may reduce your countable income.

What does the VA considered countable income

Your countable income is how much you earn, including your Social Security benefits, investment and retirement payments, and any income your dependents receive. Some expenses, like non-reimbursable medical expenses (medical expenses not covered by your insurance provider), may reduce your countable income.

How is income calculated for VA loan

If you're the only one applying for the VA loan, only include your monthly income. If you're applying with someone else, such as a spouse, you can include their income as well. Once you determine your gross monthly income, you can divide your total recurring debt payments by your gross monthly income.

Why do home sellers not like VA loans

VA Closing Costs

Some home sellers won't accept VA offers because they mistakenly believe they'll have to pay all of the buyer's closing costs. The VA does limit what closing costs Veterans can pay, which is a huge benefit for those who've served our country.

Why are VA loans so strict

The VA has strict requirements for properties it will finance, both to ensure the homeowner's safety and the property's value in the long run.

Is it harder to buy a house with a VA loan

The short answer is “no.” It's true VA loans were once harder to close — but that's ancient history. Today, you're likely to have roughly the same issues with a buyer who has this sort of mortgage as any other. And VA's flexible guidelines may be the only reason your buyer can purchase your home.