Does cosigner affect your credit score?

Does having a cosigner hurt your credit score

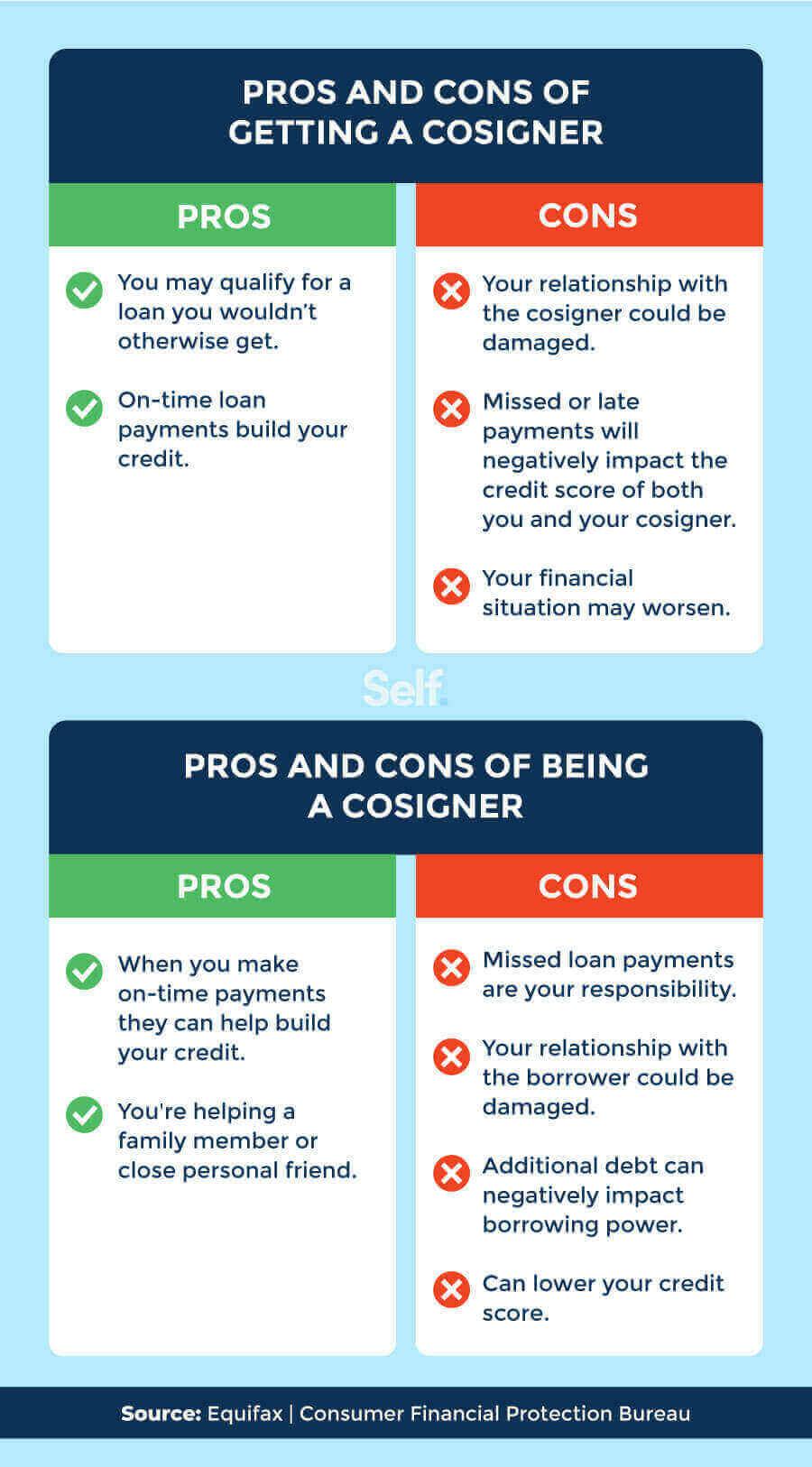

How does being a co-signer affect my credit score Being a co-signer itself does not affect your credit score. Your score may, however, be negatively affected if the main account holder misses payments.

Cached

Who gets the credit on a cosigned loan

The cosigner is responsible for paying back loan if the primary signer stops paying or is unable to pay. The loan becomes part of the co-signer's credit history. It's hard to get removed from the loan.

Cached

Will my credit go up if I have a co-signer on a car

A co-signer can also help you improve your credit score if it is low due to past financial missteps. Payment history accounts for 35 percent of your credit score, so keeping current on the auto loan payments over the loan term could help boost your score — assuming you manage all other debts responsibly.

Cached

What are the risks of cosigning

Precautions to Take Before You Cosign

Be sure you can afford to pay the loan. If you are asked to pay and cannot, you could be sued or your credit rating could be damaged. Consider that, even if you are not asked to repay the debt, your liability for this loan may keep you from getting other credit you may want.

What is the disadvantage of being a cosigner

Risks of Cosigning. Credit is at stake for both cosigners. If one person fails to pay, the other signer is pressured to pay the other person's part to protect both of their credit scores. Relationships can be tarnished if one of the cosigners aren't responsible with their payments.

Do I need good credit if I have a cosigner

If you're planning to ask a friend or family member to co-sign on your loan or credit card application, they must have a good credit score with a positive credit history. Lenders and card issuers typically require your co-signer to have a credit score of 700 or above.

Can I be removed as a cosigner

To get a co-signer release you will first need to contact your lender. After contacting them you can request the release — if the lender offers it. This is just paperwork that removes the co-signer from the loan and places you, the primary borrower, as the sole borrower on the loan.

Does Cosigning add to your debt

Cosigning can affect your ability to get financing.

In addition to the impact on your credit scores, lenders may include the payments you cosigned for when calculating your debt-to-income (DTI) ratio. A high DTI can make getting a loan or line of credit more difficult.

Can you remove yourself as a cosigner

Fortunately, you can have your name removed, but you will have to take the appropriate steps depending on the cosigned loan type. Basically, you have two options: You can enable the main borrower to assume total control of the debt or you can get rid of the debt entirely.

Is it ever a good idea to cosign

The bottom line is this: co-signing on a loan for anyone is never a good idea. If you feel compelled, lend them some money with a written agreement on how it is to be repaid. But never put your credit on the line by co-signing documents with a lender.

Why is it never a good idea to cosign a loan

Depending on how much debt you already have, the addition of the cosigned loan on your credit reports may make it look like you have more debt than you can handle. As a result, lenders may shy away from you as a borrower. It could lower your credit scores.

Can I cosign with a 650 credit score

Typically, a cosigner needs a credit score of 670 or better to be approved. This range is usually classified as very good to excellent credit.

What is the minimum credit score for a cosigner

a 670 credit score

While each lender has its own credit requirements, most expect a cosigner to have good credit with at least a 670 credit score.

How do I remove a cosigner without refinancing

A loan assumption or modification could release a co-borrower from your mortgage without refinancing into a new loan. However, lenders aren't required to grant assumptions or modifications, so be willing to negotiate.

How do I protect myself as a cosigner

5 ways to protect yourself as a co-signerServe as a co-signer only for close friends or relatives. A big risk that comes with acting as a loan co-signer is potential damage to your credit score.Make sure your name is on the vehicle title.Create a contract.Track monthly payments.Ensure you can afford payments.

Is cosigning ever a good idea

The benefits of cosigning a loan

It can be a great way, for example, to help your child build credit. When a young adult is just starting out, it can be hard to get a loan or credit card with a decent interest rate because they lack the credit history that lenders use to determine if a prospective borrower is reliable.

How hard is it to remove a cosigner

To get a co-signer release you will first need to contact your lender. After contacting them you can request the release — if the lender offers it. This is just paperwork that removes the co-signer from the loan and places you, the primary borrower, as the sole borrower on the loan.

What happens to cosigner if I don’t pay

If the borrower does not repay the loan, you may be forced to repay the whole amount of the loan, plus interest and any late fees that have accrued. With most cosigned loans, the lender is not required to pursue the main borrower first, but can request payment from the cosigner any time there is a missed payment.

Is it smart to cosign

The bottom line. The decision to sign on as a co-signer comes down to the trust you have in the primary borrower. If you believe they will meet their payments and are willing to risk your own finances, then helping a friend or family member may be the right thing to do. Otherwise, it is best to say no to this agreement …

Can I remove myself from being a cosigner

Fortunately, you can have your name removed, but you will have to take the appropriate steps depending on the cosigned loan type. Basically, you have two options: You can enable the main borrower to assume total control of the debt or you can get rid of the debt entirely.