Does Cosigning build credit?

Can being a cosigner increase your credit score

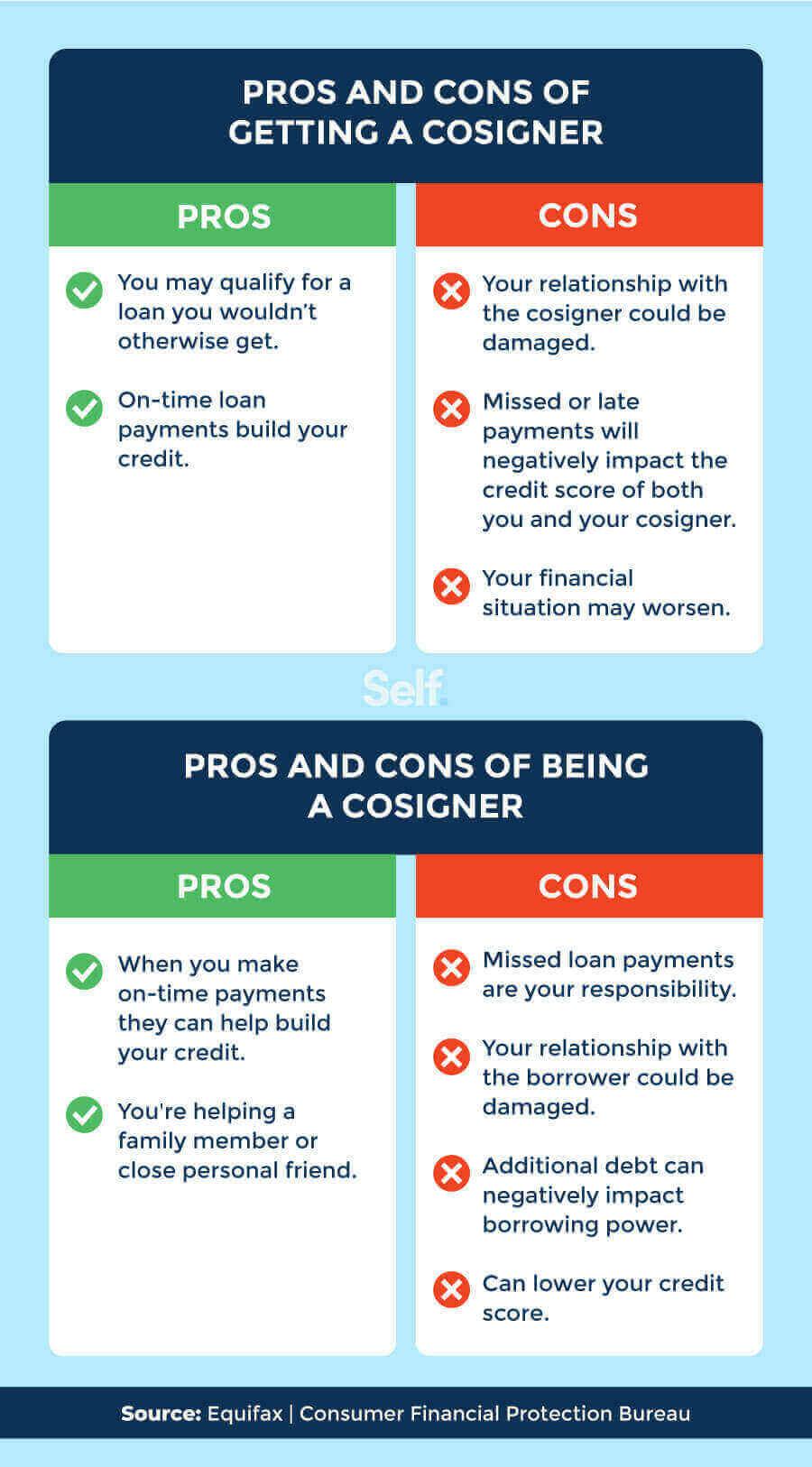

A co-signer can also help you improve your credit score if it is low due to past financial missteps. Payment history accounts for 35 percent of your credit score, so keeping current on the auto loan payments over the loan term could help boost your score — assuming you manage all other debts responsibly.

Cached

Is it ever a good idea to cosign

The bottom line is this: co-signing on a loan for anyone is never a good idea. If you feel compelled, lend them some money with a written agreement on how it is to be repaid. But never put your credit on the line by co-signing documents with a lender.

Do I need good credit if I have a cosigner

If you're planning to ask a friend or family member to co-sign on your loan or credit card application, they must have a good credit score with a positive credit history. Lenders and card issuers typically require your co-signer to have a credit score of 700 or above.

Cached

Will cosigning affect me buying a car

Cosigning an auto loan doesn't disqualify you from obtaining financing of your own — you can still get approved for an auto loan if you have a solid credit history and can afford your car payments.

Who builds credit on a cosigned loan

Having a co-signer on the loan will help the primary borrower build their credit score (as long as they continue to make on-time payments). It could also help the co-signer build their credit score and credit history, if the primary borrower makes on-time payments throughout the course of the loan.

Who gets the credit on a cosigned loan

Cosigning for someone means you're taking responsibility for the loan, lease or similar contract if the original borrower is unable to pay as agreed. Whatever you cosign will show up on your credit report as if the loan is yours, which, depending on your credit history, may impact your credit scores.

Why is it risky to be a co-signer

The lender can sue the cosigner for interest, late fees, and any attorney's fees involved in collection. If the primary borrower falls on hard times financially and cannot make payments, AND the cosigner fails to make the payments, the lender may also decide to pursue garnishment of the wages of the cosigner.

How much credit does a cosigner get

Being a co-signer itself does not affect your credit score. Your score may, however, be negatively affected if the main account holder misses payments.

Can I be removed as a cosigner

To get a co-signer release you will first need to contact your lender. After contacting them you can request the release — if the lender offers it. This is just paperwork that removes the co-signer from the loan and places you, the primary borrower, as the sole borrower on the loan.

How high does a co-signer’s credit have to be

670 or better

Although lender requirements vary, a cosigner generally needs a credit score that is at least considered "very good," which usually means at least 670 or better.

Why is it never a good idea to cosign a loan

Depending on how much debt you already have, the addition of the cosigned loan on your credit reports may make it look like you have more debt than you can handle. As a result, lenders may shy away from you as a borrower. It could lower your credit scores.

Is it smart to cosign

The bottom line. The decision to sign on as a co-signer comes down to the trust you have in the primary borrower. If you believe they will meet their payments and are willing to risk your own finances, then helping a friend or family member may be the right thing to do. Otherwise, it is best to say no to this agreement …

Can I cosign with a 650 credit score

Typically, a cosigner needs a credit score of 670 or better to be approved. This range is usually classified as very good to excellent credit.

Can you cosign with a 700 credit score

Cosigners are usually required to have: Excellent credit—often with a credit score above 700. A good debt-to-income ratio. A steady income.

Will removing myself as a cosigner hurt my credit

Being removed as a cosigner from a loan with a positive payment history could potentially hurt your credit. How much will depend on your current credit history.

Who gets the credit score if you have a cosigner

Co-signing a loan can help or hurt your credit scores. Having a co-signer on the loan will help the primary borrower build their credit score (as long as they continue to make on-time payments).

How to go from 650 to 750 credit score

Here are some of the best ways.Pay on Time, Every Time.Reduce Your Credit Card Balances.Avoid Taking Out New Debt Frequently.Be Mindful of the Types of Credit You Use.Dispute Inaccurate Credit Report Information.Don't Close Old Credit Cards.

Can I get a 50K loan with a 650 credit score

For a loan of 50K, lenders usually want the borrower to have a minimum credit score of 650 but will sometimes consider a credit score of 600 or a bit lower. For a loan of 50K or more, a poor credit score is anything below 600 and you might find it difficult to get an unsecured personal loan.

Can I get a loan with a 500 credit score with a cosigner

Apply with a cosigner

The cosigner's credit and income impact the lender's decision more than those of the primary applicant, so it can help people with a credit score of 500 get approved for loans they might not normally qualify for.

How hard is it to remove a cosigner

To get a co-signer release you will first need to contact your lender. After contacting them you can request the release — if the lender offers it. This is just paperwork that removes the co-signer from the loan and places you, the primary borrower, as the sole borrower on the loan.