Does it hurt your credit score to get pre-approved?

How much does pre-approval affect credit score

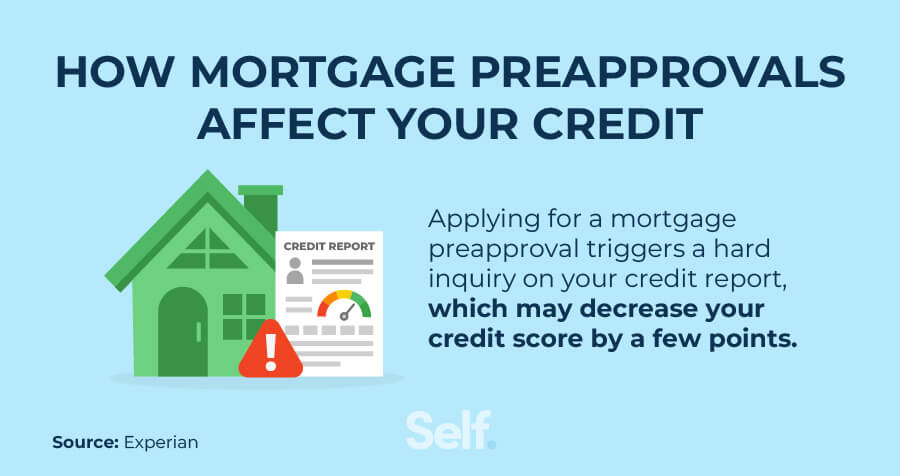

A mortgage pre-approval affects a home buyer's credit score. The pre-approval typically requires a hard credit inquiry, which decreases a buyer's credit score by five points or less. A pre-approval is the first big step towards purchasing your first home.

Cached

How do I get pre-approved without affecting my credit score

Get prequalified for a mortgage

To prequalify you for a loan, lenders check your credit report, but conduct a “soft” inquiry, or soft pull, in which they prescreen your report without it affecting your score.

Will getting prequalified hurt my credit

Just like other loans or credit cards, mortgage prequalification doesn't hurt your scores since it's also based on a soft inquiry. Having your credit report evaluated is a necessary part of the mortgage process.

Cached

Is it bad to get pre-approved too early

As a home buyer, pre-approvals are for your benefit, so it's never too early to get one. Getting pre-approved early is an advantage because one-third of mortgage applications contain an error. These errors can negatively affect your interest rate and ability to buy a home.

Is it better to get pre-approved

Getting preapproved is a smart step to take when you are ready to put in an offer on a home. It shows sellers that you're a serious homebuyer and that you can secure a mortgage – which makes it more likely that you'll complete your purchase of the home.

Why did my credit score drop after pre-approval

This occurs when a lender is considering extending a line of credit to you. Hard inquiries show up on your credit report and can affect your credit scores. For example, if you apply for a pre-approval offer, it will trigger a hard inquiry, and you could see a dip in your credit scores.

How many credit cards is too many to have open

It's generally recommended that you have two to three credit card accounts at a time, in addition to other types of credit. Remember that your total available credit and your debt to credit ratio can impact your credit scores. If you have more than three credit cards, it may be hard to keep track of monthly payments.

How many points does your credit score go down for an inquiry

about five points

While a hard inquiry does impact your credit scores, it typically only causes them to drop by about five points, according to credit-scoring company FICO®. And if you have a good credit history, the impact may be even less.

What is better prequalified or preapproved

This means a preapproval is a stronger sign of what you can afford and adds more credibility to your offer than a prequalification. This will also allow you to show sellers a preapproval letter to demonstrate that your financial information has been verified and you can afford a mortgage.

Which is better prequalified and pre-approved

The biggest difference between the two is that getting pre-qualified is typically a faster and less detailed process, while pre-approvals are more comprehensive and take longer. Getting a pre-qualification or pre-approval letter is generally not a guarantee that you will secure a loan from the lender.

What happens if I get pre-approved

Preapproval is as close as you can get to confirming your creditworthiness without having a purchase contract in place. You will complete a mortgage application and the lender will verify the information you provide. They'll also perform a credit check.

Is pre-approved a good thing

Getting a pre-qualification or pre-approval letter is generally not a guarantee that you will secure a loan from the lender. However, it may help you prove to a seller that you are able to receive financing for your purchase.

What is the point of a pre-approval

It establishes your credibility as a homebuyer.

A mortgage pre-approval shows home sellers that you have your finances in check, that you're serious about buying a house, and that you won't be denied a mortgage if they decide to sell you their home.

Why did my credit score drop 50 points after opening a credit card

You applied for a new credit card

Card issuers pull your credit report when you apply for a new credit card because they want to see how much of a risk you pose before lending you a line of credit. This credit check is called a hard inquiry, or “hard pull,” and temporarily lowers your credit score a few points.

Why is my credit score going down if I pay everything on time

Similarly, if you pay off a credit card debt and close the account entirely, your scores could drop. This is because your total available credit is lowered when you close a line of credit, which could result in a higher credit utilization ratio.

Is it bad to have a lot of credit cards with zero balance

It is not bad to have a lot of credit cards with zero balance because positive information will appear on your credit reports each month since all of the accounts are current. Having credit cards with zero balance also results in a low credit utilization ratio, which is good for your credit score, too.

What is the no 1 way to raise your credit score

One of the best things you can do to improve your credit score is to pay your debts on time and in full whenever possible. Payment history makes up a significant chunk of your credit score, so it's important to avoid late payments.

How to get 800 credit score in 45 days

Here are 10 ways to increase your credit score by 100 points – most often this can be done within 45 days.Check your credit report.Pay your bills on time.Pay off any collections.Get caught up on past-due bills.Keep balances low on your credit cards.Pay off debt rather than continually transferring it.

How many credit pulls is too many

In general, six or more hard inquiries are often seen as too many. Based on the data, this number corresponds to being eight times more likely than average to declare bankruptcy. This heightened credit risk can damage a person's credit options and lower one's credit score.

Why would you get denied after pre approval

Buyers are denied after pre-approval because they increase their debt levels beyond the lender's debt-to-income ratio parameters. The debt-to-income ratio is a percentage of your income that goes towards debt. When you take on new debt without an increase in your income, you increase your debt-to-income ratio.