Does paying off a loan lower your credit score?

Why did my credit score go down after paying off a loan

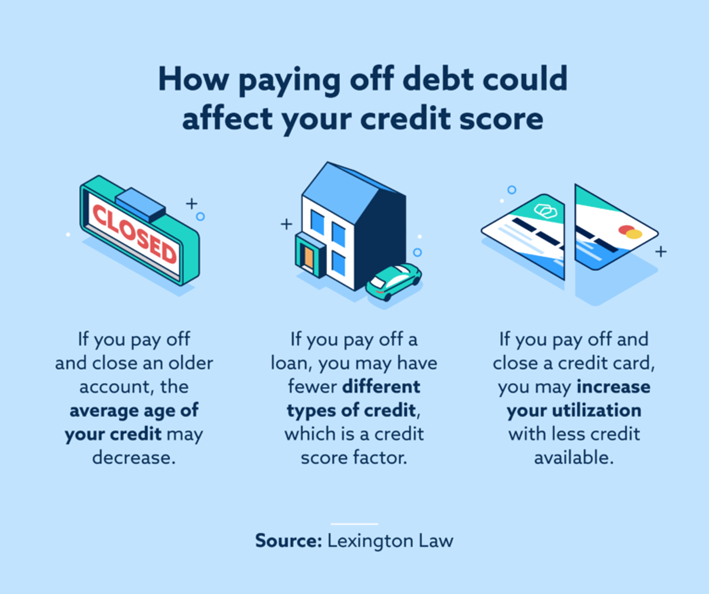

It's possible that you could see your credit scores drop after fulfilling your payment obligations on a loan or credit card debt. Paying off debt might lower your credit scores if removing the debt affects certain factors like your credit mix, the length of your credit history or your credit utilization ratio.

Cached

Does it hurt your credit score to pay off a loan

In short, yes—paying off a personal loan early could temporarily have a negative impact on your credit scores. You might be thinking, “Isn't paying off debt a good thing” And generally, it is. But credit reporting agencies look at several factors when determining your scores.

Cached

How many points does credit go up after paying off a loan

Your credit score could increase by 10 to 50 points after paying off your credit cards. Exactly how much your score will increase depends on factors such as the amounts of the balances you paid off and how you handle other credit accounts. Everyone's credit profile is different.

Is it bad to pay off a personal loan early

Paying off the loan early can put you in a situation where you must pay a prepayment penalty, potentially undoing any money you'd save on interest, and it can also impact your credit history.

Why would my credit score drop 40 points in one month

Your credit score may have dropped by 40 points because a late payment was listed on your credit report or you became further delinquent on past-due bills. It's also possible that your credit score fell because your credit card balances increased, causing your credit utilization to rise.

Why did my credit score drop 60 points after paying off my car

Lenders like to see a mix of both installment loans and revolving credit on your credit portfolio. So if you pay off a car loan and don't have any other installment loans, you might actually see that your credit score dropped because you now have only revolving debt.

Why did my credit score drop 40 points after paying off debt

Paying off debt can lower your credit score when: It changes your credit utilization ratio. It lowers average credit account age. You have fewer kinds of credit accounts.

How to raise credit score 100 points in 30 days

Quick checklist: how to raise your credit score in 30 daysMake sure your credit report is accurate.Sign up for Credit Karma.Pay bills on time.Use credit cards responsibly.Pay down a credit card or loan.Increase your credit limit on current cards.Make payments two times a month.Consolidate your debt.

How can a credit score drop 100 points in a month

New credit applications

In the FICOscoring model, each hard inquiry — when a creditor checks your credit report before approving or denying credit — can cost you up to five points on your credit score. So, if you apply for more than 20 credit cards in one month, you could see a 100-point credit score drop.

Does paying a car loan off early hurt your credit

Paying off your car loan early can hurt your credit score. Any time you close a credit account, your score will fall by a few points. So, while it's normal, if you are on the edge between two categories, waiting to pay off your car loan may be a good idea if you need to maintain your score for other big purchases.

Is it better to prepay personal loan

When you prepay your loan, then the overall EMI gets lowered allowing you to pay a lower interest on your outstanding amount. Your credit score also improves and you also get to save money.

Why did my credit score drop 700 points

Reasons why your credit score could have dropped include a missing or late payment, a recent application for new credit, running up a large credit card balance or closing a credit card.

How did my credit score drop 60 points in a month

Your credit score may have dropped by 60 points because negative information, like late payments, a collection account, a foreclosure or a repossession, was added to your credit report. Credit scores are based on the contents of your credit report and are adversely impacted by derogatory marks.

Why did my credit score drop 40 points in one day

Your credit score may have dropped by 40 points because a late payment was listed on your credit report or you became further delinquent on past-due bills. It's also possible that your credit score fell because your credit card balances increased, causing your credit utilization to rise.

Why did my credit score drop 100 points in one month

Credit scores can drop due to a variety of reasons, including late or missed payments, changes to your credit utilization rate, a change in your credit mix, closing older accounts (which may shorten your length of credit history overall), or applying for new credit accounts.

Why did my credit score drop 100 points in a day

Credit scores can drop due to a variety of reasons, including late or missed payments, changes to your credit utilization rate, a change in your credit mix, closing older accounts (which may shorten your length of credit history overall), or applying for new credit accounts.

How fast can I add 100 points to my credit score

For most people, increasing a credit score by 100 points in a month isn't going to happen. But if you pay your bills on time, eliminate your consumer debt, don't run large balances on your cards and maintain a mix of both consumer and secured borrowing, an increase in your credit could happen within months.

How to get a 900 credit score in 45 days

Here are 10 ways to increase your credit score by 100 points – most often this can be done within 45 days.Check your credit report.Pay your bills on time.Pay off any collections.Get caught up on past-due bills.Keep balances low on your credit cards.Pay off debt rather than continually transferring it.

How to get a 750 credit score in 6 months

How to Increase Your Credit Score in 6 MonthsPay on time (35% of your score) The most critical part of a good credit score is your payment history.Reduce your debt (30% of your score)Keep cards open over time (15% of your score)Avoid credit applications (10% of your score)Keep a smart mix of credit types open (10%)

Is A 650 A Good credit score

A FICO® Score of 650 places you within a population of consumers whose credit may be seen as Fair. Your 650 FICO® Score is lower than the average U.S. credit score. Statistically speaking, 28% of consumers with credit scores in the Fair range are likely to become seriously delinquent in the future.