Does paying statement balance build credit?

Is it better to pay statement or full balance to build credit

Carrying a balance does not help your credit score, so it's always best to pay your balance in full each month. The impact of not paying in full each month depends on how large of a balance you're carrying compared to your credit limit.

Does paying your statement balance affect your credit score

Both your statement balance and current balance affect your credit score.

Cached

Is paying statement balance early good

Paying early also cuts interest

Not only does that help ensure that you're spending within your means, but it also saves you on interest. If you always pay your full statement balance by the due date, you will maintain a credit card grace period and you will never be charged interest.

Cached

Should I pay statement balance or minimum balance

Experts recommend you pay the statement balance in full every month, but there are times when that may not be possible. In those cases, it's important to make at least the minimum payment so your account stays current and you don't incur any late fees or penalty APRs.

Should I pay off my entire statement balance

Pay your statement balance in full to avoid interest charges

But in order to avoid interest charges, you'll need to pay your statement balance in full. If you pay less than the statement balance, your account will still be in good standing, but you will incur interest charges.

How fast can I add 100 points to my credit score

For most people, increasing a credit score by 100 points in a month isn't going to happen. But if you pay your bills on time, eliminate your consumer debt, don't run large balances on your cards and maintain a mix of both consumer and secured borrowing, an increase in your credit could happen within months.

What happens if I pay my statement balance

Paying your statement balance helps you avoid interest rates, which can add up quickly and make it more challenging to pay off your credit card debt.

How to pay off credit card to increase credit score

Just pay off your credit card bill in full and on time each month, and the card issuer will report your payments to the credit bureaus. By paying in full, you also won't have to pay interest. Your payment history makes up 35% of your FICO credit score, so this is one of the best things you can do to build your credit.

What happens if you just pay your statement balance

Pay your statement balance in full to avoid interest charges

But in order to avoid interest charges, you'll need to pay your statement balance in full. If you pay less than the statement balance, your account will still be in good standing, but you will incur interest charges.

What is the 15 3 rule

The 15/3 credit card payment rule is a strategy that involves making two payments each month to your credit card company. You make one payment 15 days before your statement is due and another payment three days before the due date.

Which is the best strategy for paying your credit card bill

The best way to pay your credit card bill is by paying the statement balance on your credit bill by the due date each month. Doing so will allow you to avoid incurring any interest or fees. In case you weren't aware, you do not automatically pay interest simply by having a credit card.

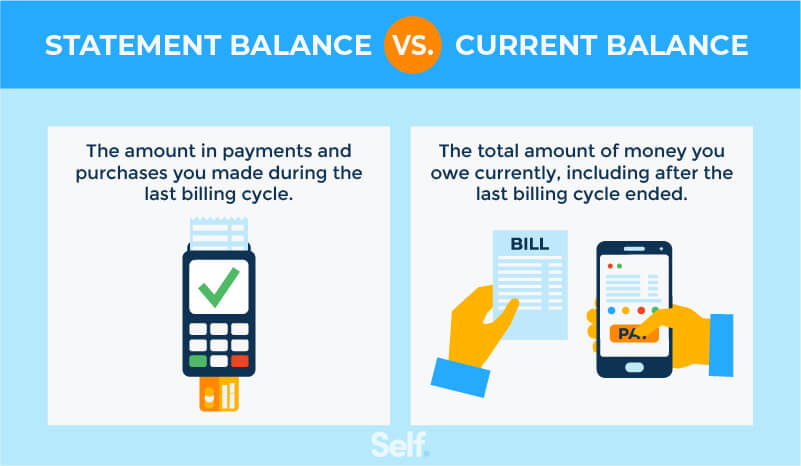

Is a statement balance how much you owe

Your statement balance typically shows what you owe on your credit card at the end of your last billing cycle. Your current balance, however, will typically reflect the total amount that you owe at any given moment.

How to get a 700 credit score in 30 days

Best Credit Cards for Bad Credit.Check Your Credit Reports and Credit Scores. The first step is to know what is being reported about you.Correct Mistakes in Your Credit Reports. Once you have your credit reports, read them carefully.Avoid Late Payments.Pay Down Debt.Add Positive Credit History.Keep Great Credit Habits.

How to get 800 credit score in 45 days

Here are 10 ways to increase your credit score by 100 points – most often this can be done within 45 days.Check your credit report.Pay your bills on time.Pay off any collections.Get caught up on past-due bills.Keep balances low on your credit cards.Pay off debt rather than continually transferring it.

What does statement balance mean when paying credit card

Your statement balance typically shows what you owe on your credit card at the end of your last billing cycle. Your current balance, however, will typically reflect the total amount that you owe at any given moment. Billing cycle times frames may vary if an issuer allows cardmembers to change their billing cycle.

Is it bad to pay more than statement balance

There's nothing wrong with paying your current balance in full, even if it's higher than your statement balance, if you want to do so. But you should understand that paying your current balance won't save you any extra money in interest, unless you've previously lost your card's grace period.

How to raise credit score 100 points in 30 days

Quick checklist: how to raise your credit score in 30 daysMake sure your credit report is accurate.Sign up for Credit Karma.Pay bills on time.Use credit cards responsibly.Pay down a credit card or loan.Increase your credit limit on current cards.Make payments two times a month.Consolidate your debt.

How can I raise my credit score 40 points fast

Here are six ways to quickly raise your credit score by 40 points:Check for errors on your credit report.Remove a late payment.Reduce your credit card debt.Become an authorized user on someone else's account.Pay twice a month.Build credit with a credit card.

Why does the 15 3 credit hack work

The 15/3 hack can help struggling cardholders improve their credit because paying down part of a monthly balance—in a smaller increment—before the statement date reduces the reported amount owed. This means that credit utilization rate will be lower which can help boost the cardholder's credit score.

What is the 30 percent credit rule

Your credit utilization ratio should be 30% or less, and the lower you can get it, the better it is for your credit score. Your credit utilization ratio is one of the most important factors of your credit score—and keeping it low is key to top scores. Here's how to do it.