Does transform credit report to credit bureaus?

Is transform credit loans legit

Is Transform Credit legit Yes. Transform Credit is licensed to offer loans in nine states. It's headquartered in Chicago, Illinois, and it has a customer service phone number.

Cached

Can a private lender report to credit bureau

However, since private lenders do not report to the credit bureau, a private mortgage alone will not improve your credit score. But if used correctly, a private mortgage can buy you enough time to repair your credit yourself.

What gets reported to credit bureaus

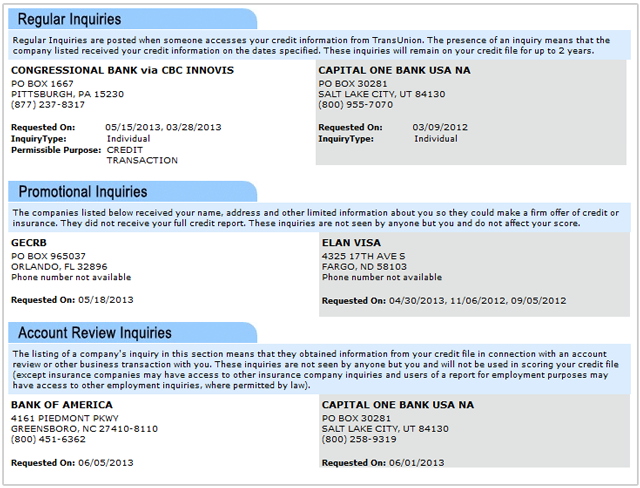

Your credit report is primarily a record of your payment history on your various credit accounts. These accounts include credit cards, car loans, mortgages, student loans and similar debts. Credit reports also include reports on things like bankruptcies and tax liens, and can even include rent or bill payments.

Do you need a cosigner for transform credit

Transform Credit is a cosigner loan provider; all of our customers must have a cosigner for us to lend to them. A cosigner is a great sign to us that someone trusts you and that we should too, no matter what your credit history! A cosigner's responsibility is to make the loan repayments if the borrower does not.

How fast does transform credit pay

We aim to pay out every loan within 24 hours of the cosigner being accepted. If you and your cosigner complete the application online and all checks are completed without issue, we could get the money to you sooner.

Why is transform credit charging me $5 dollars

If you have been charged $5 this will be for your monthly payment to Transform Credit Builder. When you created your Transform Credit Builder account, you agreed to make a payment of $5 per month. It is these repayments that we report back to the credit bureaus each month to help grow and build your credit score.

Can you request a credit card company to report to credit bureau

Credit reporting is a voluntary process. There's nothing you can do to force a creditor to report an account to the credit bureaus. And you can't make a creditor update your account outside of its normal credit reporting cycle.

Why do some lenders not report to credit bureaus

The primary reason some banks choose not to report customers' account activity to the credit bureaus is that doing so is costly and complicated. Reporting borrowers' information requires the lender to go through the complex steps of setting up an account with each credit bureau.

What is not reported to credit bureaus

Most of Your Everyday Bills Are Not Reported

While your credit card accounts and lines of credit are pulled into your credit report, your day-to-day bills, such as your rent and utility payments like Internet, water, and electricity aren't roped in.

Is 600 a good credit score to buy a house

A 600 credit score is high enough to get a home loan. In fact, there are several mortgage programs designed specifically to help people with lower credit scores. However, you'll need to meet other lending requirements too.

What is the minimum credit score for a cosigner

670 or better

Although there might not be a required credit score, a cosigner typically will need credit in the very good or exceptional range—670 or better. A credit score in that range generally qualifies someone to be a cosigner, but each lender will have its own requirement.

Does my credit score go up if I have a cosigner

How does being a co-signer affect my credit score Being a co-signer itself does not affect your credit score. Your score may, however, be negatively affected if the main account holder misses payments.

How long does it take to build credit from 500 to 750

Average Recovery Time

For instance, going from a poor credit score of around 500 to a fair credit score (in the 580-669 range) takes around 12 to 18 months of responsible credit use. Once you've made it to the good credit zone (670-739), don't expect your credit to continue rising as steadily.

How does transform credit works

Transform Credit Builder is a loan product that provides a simple and easy way to build your credit score. As part of your Transform Credit Builder agreement we report to the credit bureaus each of your payments. Each positive payment that is recorded on your credit file could help build and improve your credit score.

Why is there a $75 charge on my credit one credit card

Annual fee: The Credit One Visa for Rebuilding Credit card does have an annual fee, as do most unsecured credit building cards. The fee is $75 the first year and $99 after that and is charged against your credit line.

How do I stop my company from charging my credit card

Stopping an automatic, recurring payment on a credit card is different. Start by putting in your request with the vendor. But if the vendor continues to charge your credit card, contact your card issuer. You'll have 60 days to dispute the charge, starting when the card issuer sends you the statement with the charges.

Why is my credit card company not reporting to credit bureaus

Credit cards don't pop up on your credit reports the moment you're approved. It can take anywhere from 30 – 60 days for your account's credit activity to be reported to the credit bureaus. It'll usually happen after the first billing cycle comes to a close.

How do I ask my creditor to update my credit report

Instead, get in touch with your creditors and ask them to update your records with your new address, name or employer. When your creditors send their monthly updates to the credit bureaus, they'll include your new information and your credit reports will be updated.

How long do lenders have to report to credit bureaus

When are credit reports updated Your credit reports are updated when lenders provide new information to the nationwide credit reporting agencies (Equifax, Experian, TransUnion) for your accounts. This usually happens once a month, or at least every 45 days. However, some lenders may update more frequently than this.

Why did my credit score go from 524 to 0

Credit scores can drop due to a variety of reasons, including late or missed payments, changes to your credit utilization rate, a change in your credit mix, closing older accounts (which may shorten your length of credit history overall), or applying for new credit accounts.