Does your credit drop if you’re a cosigner?

Who gets the credit on a cosigned loan

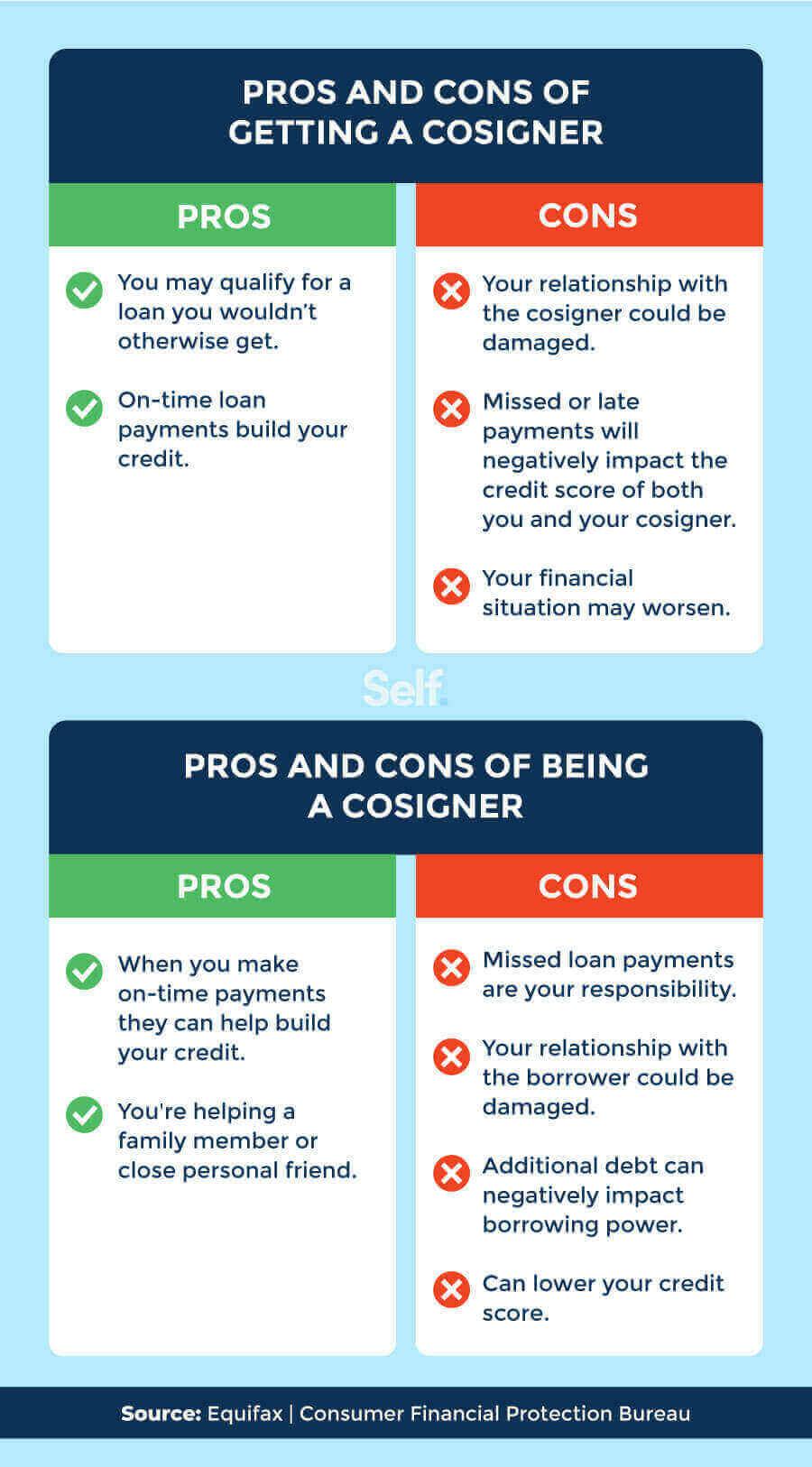

Both the primary borrower and the cosigner on a loan will get credit if the primary borrower makes the payments on time. On the other hand, if the primary borrower does not keep up with the monthly payments, both their credit score and the cosigner's credit score will drop.

What are the risks of cosigning

Precautions to Take Before You Cosign

Be sure you can afford to pay the loan. If you are asked to pay and cannot, you could be sued or your credit rating could be damaged. Consider that, even if you are not asked to repay the debt, your liability for this loan may keep you from getting other credit you may want.

Will cosigning affect me buying a car

Cosigning an auto loan doesn't disqualify you from obtaining financing of your own — you can still get approved for an auto loan if you have a solid credit history and can afford your car payments.

Is it better to have a cosigner even if they have bad credit

If your credit history is less than stellar, you might want to consider using a cosigner. Making regular, manageable payments is the key to rebuilding credit and a cosigner can help you secure lower interest rates that could save you hundreds (if not thousands) of dollars over the lifetime of your loan.

How high does a co-signer’s credit have to be

670 or better

Although lender requirements vary, a cosigner generally needs a credit score that is at least considered "very good," which usually means at least 670 or better.

How much of a difference does a co-signer make

A co-signer may increase your chance of approval, give you access to better loan terms and — over time — help you improve your credit score as you pay back your auto loan. Improve your chance of approval. A co-signer adds to your application if you don't have an extensive credit history or have a poor credit score.

Why is it never a good idea to cosign a loan

Depending on how much debt you already have, the addition of the cosigned loan on your credit reports may make it look like you have more debt than you can handle. As a result, lenders may shy away from you as a borrower. It could lower your credit scores.

Is it ever a good idea to cosign

The bottom line is this: co-signing on a loan for anyone is never a good idea. If you feel compelled, lend them some money with a written agreement on how it is to be repaid. But never put your credit on the line by co-signing documents with a lender.

Is it smart to cosign for a car

Serving as a co-signer is a good idea if your relationship is strong and can survive financial pressure, you can track monthly payments, can afford to pay off the loan if necessary and can handle a long-term financial commitment.

What credit score do you need to cosign for a car

700 or above

Generally, lenders will require a potential cosigner to have a credit rating score of 700 or above. People with this range of credit score, and higher, are generally very financially responsible and pay their bills and obligations on time. If you have bad credit, your cosigner and needs to have excellent credit.

Can a cosigner have a 600 credit score

If you're planning to ask a friend or family member to co-sign on your loan or credit card application, they must have a good credit score with a positive credit history. Lenders and card issuers typically require your co-signer to have a credit score of 700 or above.

Does having a cosigner look bad

Depending on how much debt you already have, the addition of the cosigned loan on your credit reports may make it look like you have more debt than you can handle. As a result, lenders may shy away from you as a borrower.

Can you cosign with a 700 credit score

Cosigners are usually required to have: Excellent credit—often with a credit score above 700. A good debt-to-income ratio. A steady income.

Can I cosign with a 650 credit score

Typically, a cosigner needs a credit score of 670 or better to be approved. This range is usually classified as very good to excellent credit.

What is the disadvantage of being a cosigner

You'll be tied to this person, and any possible financial upheavals, for the term of the loan, whether that's six months or 10 years. You'll be responsible for repayment if the borrower has financial difficulties or if something else goes wrong, and your relationship could suffer.

Can a cosigner have worse credit

Cosigning a loan can affect the co-signer's credit score—for better or for worse. The loan will be added to the co-signer's credit history and impact their credit score. Any late or missed payments on the loan will also have an impact on credit score.

Is it smart to cosign

The bottom line. The decision to sign on as a co-signer comes down to the trust you have in the primary borrower. If you believe they will meet their payments and are willing to risk your own finances, then helping a friend or family member may be the right thing to do. Otherwise, it is best to say no to this agreement …

Can I get a car with a 550 credit score and a cosigner

The pledge and guarantee to pay must be in writing. In order for your cosigner to be accepted by the bank or lender, the cosigner is usually required to have a good or excellent personal credit rating. Generally, lenders will require a potential cosigner to have a credit rating score of 700 or above.

Do you build credit faster with a cosigner

A co-signer can also help you improve your credit score if it is low due to past financial missteps. Payment history accounts for 35 percent of your credit score, so keeping current on the auto loan payments over the loan term could help boost your score — assuming you manage all other debts responsibly.

Can a cosigner have worse credit than you

Cosigning a loan can affect the co-signer's credit score—for better or for worse. The loan will be added to the co-signer's credit history and impact their credit score.