How do I waive late charges on my credit card?

Can credit card late fees be waived

If you want to have your late fee removed, you can ask your credit card issuer to get it waived. Whether they accept your request is completely up to their discretion, but if your payment history is good and your payments have been on-time, they are likely to accept.

Cached

How do I ask for a late payment fee waived

Contact your credit card issuer

Apologize for the late fee, and explain why it happened. Make sure to highlight your history as a good customer and ask if they'll be willing to waive the fee.

Cached

How do I get my credit card company to remove late payments

To get an incorrect late payment removed from your credit report, you need to file a dispute with the credit bureau that issued the report containing the error. Setting up automatic payments and regularly monitoring your credit can help you avoid late payments and spot any that were inaccurately reported.

Will a 2 day late payment affect credit score

Even a single late or missed payment may impact credit reports and credit scores. But the short answer is: late payments generally won't end up on your credit reports for at least 30 days after the date you miss the payment, although you may still incur late fees.

How bad is one late fee on credit card

Late payment fee: In most cases, you'll be hit with a late payment fee. This fee is often up to $41. Penalty APR: A late payment can cause your interest rate to spike significantly higher than your regular purchase APR.

Do unpaid late fees affect credit score

A late payment can drop your credit score by as much as 180 points and may stay on your credit reports for up to seven years. However, lenders typically report late payments to the credit bureaus once you're 30 days past due, meaning your credit score won't be damaged if you pay within those 30 days.

How do you professionally ask for a fee to be waived

When negotiating a fee waiver, it's important to be specific and straightforward. Call the bank, mention the fee you incurred and say you would like to have it waived by the bank. If the bank isn't immediately open to helping you, try to show you're a valuable customer.

Can you negotiate late payments

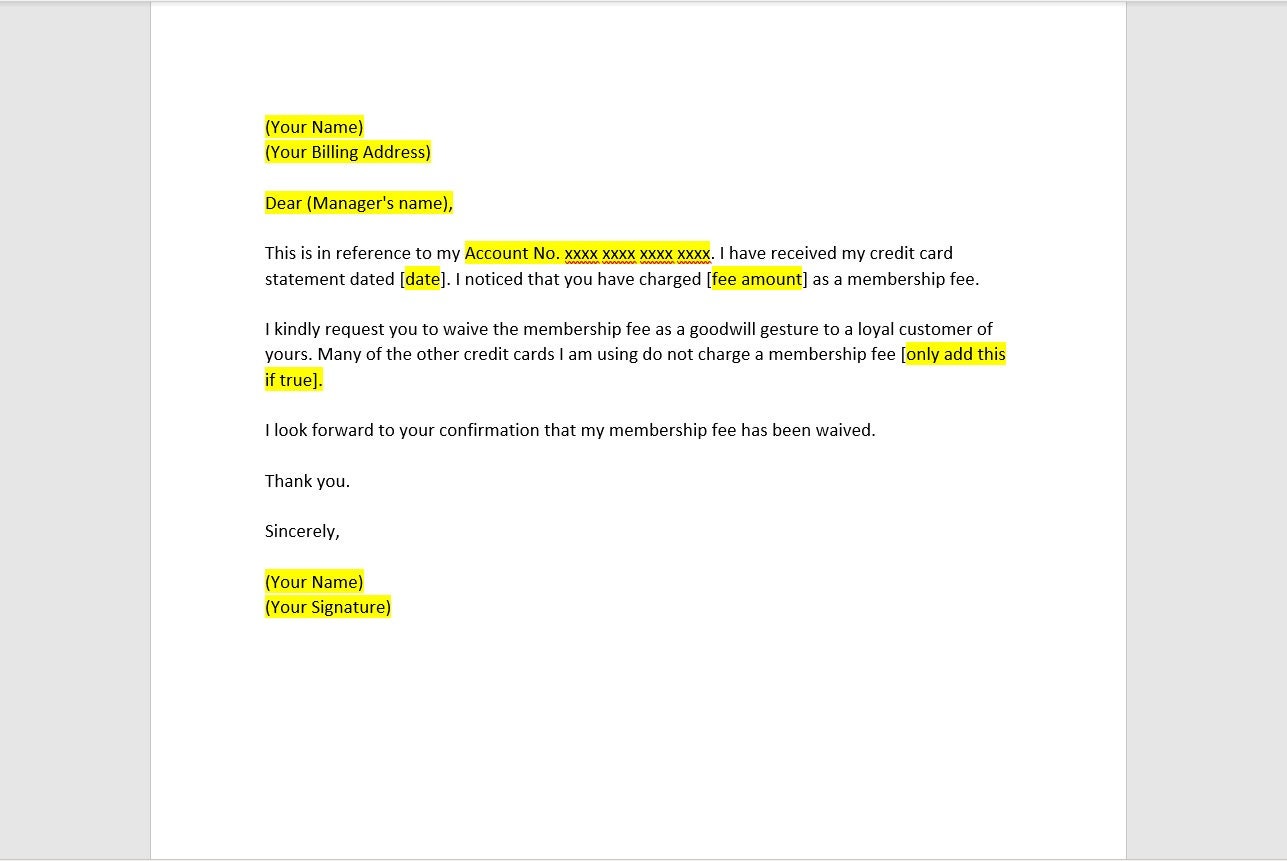

In some cases, creditors are willing to make a goodwill adjustment if your payment history has been good or if you have a good relationship with them. The process is easy: simply write a letter to your creditor explaining why you paid late. Ask them to forgive the late payment and assure them it won't happen again.

Can I get a late payment removed

Can you remove late payments from your credit reports If you act quickly by paying within 30 days of the original due date, a late payment will generally not be recorded on your credit reports. After 30 days, you can only remove falsely reported late payments.

Do goodwill letters work for late payments

One possible solution: You may be able to remove late payments on your credit reports and start to improve your credit with a “goodwill letter.” A goodwill letter won't always work, but some consumers have reported success. It's worth trying because these derogatory marks on your credit can last seven years.

How long does 1 late payment affect credit score

seven years

A late payment will stay on your credit reports for up to seven years from the date of the delinquency, even if you catch up on payments after falling behind. If you leave the bill unpaid, it will still fall off your credit history in seven years, but you'll suffer hefty penalties in the meantime.

How bad is one late payment on credit score

Your credit score can drop by as much as 100+ points if one late payment appears on your credit report, but the impact will vary depending on the scoring model and your overall financial profile.

What happens if I pay my credit card bill 1 day late

You will have to pay a late fee if you pay your bill after the due date. The late fee would be charged by the bank in your next credit card bill. In a recent move, the Reserve Bank of India (RBI) has directed banks to charge late fee only if the payment has been due for more than three days after the due date.

How much does 1 missed payment affect credit score

Your credit score can drop by as much as 100+ points if one late payment appears on your credit report, but the impact will vary depending on the scoring model and your overall financial profile.

How much does 1 late payment affect credit score

Your credit score can drop by as much as 100+ points if one late payment appears on your credit report, but the impact will vary depending on the scoring model and your overall financial profile.

How much does your credit score drop for a late payment

A late payment can drop your credit score by as much as 180 points and may stay on your credit reports for up to seven years. However, lenders typically report late payments to the credit bureaus once you're 30 days past due, meaning your credit score won't be damaged if you pay within those 30 days.

What do you say to get a fee waived

When negotiating a fee waiver, it's important to be specific and straightforward. Call the bank, mention the fee you incurred and say you would like to have it waived by the bank. If the bank isn't immediately open to helping you, try to show you're a valuable customer.

How do I get a fee waiver

1. Get an SAT or ACT WaiverEnrollment in a free or reduced-cost lunch program.Income eligibility for the USDA's Food and Nutrition Service.Receipt of public assistance or another low-income program from the local, state, or federal government.Homelessness.Status as an orphan or ward of the state.

How many late payments is considered bad

Anything more than 30 days will likely cause a dip in your credit score that can be as much as 180 points. Here are more details on what to expect based on how late your payment is: Payments less than 30 days late: If you miss your due date but make a payment before it's 30 days past due, you're in luck.

What is a 609 letter to remove late payments

A 609 letter is a credit repair method that requests credit bureaus to remove erroneous negative entries from your credit report. It's named after section 609 of the Fair Credit Reporting Act (FCRA), a federal law that protects consumers from unfair credit and collection practices.