How hard does a mortgage application hit your credit?

Does submitting a mortgage application affect credit score

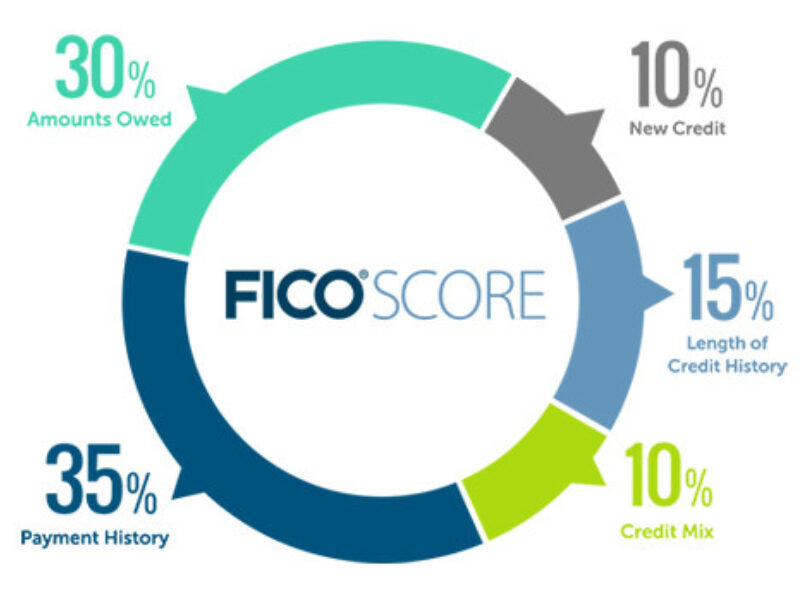

Your credit score might take an initial hit when you apply for a mortgage because the lender will have to open up a hard inquiry into your credit report. A hard inquiry (a.k.a., a “hard pull”) is when a lender pulls your credit report from one of the three main credit bureaus (Experian, Equifax or TransUnion).

How much does your credit score drop when applying for a mortgage

A New Mortgage May Temporarily Lower Your Credit Score

When a lender pulls your credit score and report as part of a loan application, the inquiry can cause a minor drop in your credit score (usually less than five points).

Cached

How long does it take for a mortgage to hit your credit report

30 to 90 days

One of the most common reasons you don't yet see your mortgage on your credit report is because there's been a simple reporting delay. For most people, it can take anywhere from 30 to 90 days for a new or refinanced loan to appear.

Cached

How many times does your credit get pulled when buying a house

While the number of credit checks for a mortgage can vary depending on the situation, most lenders will check your credit up to three times during the application process.

Cached

What should you not say when applying for a mortgage

1) Anything untruthful

Lying to a mortgage lender can ruin your chances of approval. On top of that, providing misleading info on a loan application is considered mortgage fraud. Some try to hide certain info, but lenders are required to perform verifications of key financial documents.

How many inquiries is too many for a mortgage

There's no such thing as “too many” hard credit inquiries, but multiple applications for new credit accounts within a short time frame could point to a risky borrower. Rate shopping for a particular loan, however, may be treated as a single inquiry and have minimal impact on your creditworthiness.

Do mortgage pre approvals affect credit score

A mortgage pre-approval affects a home buyer's credit score. The pre-approval typically requires a hard credit inquiry, which decreases a buyer's credit score by five points or less. A pre-approval is the first big step towards purchasing your first home.

Do all lenders pull credit day of closing

The answer is yes. Lenders pull borrowers' credit at the beginning of the approval process, and then again just prior to closing.

Do they check credit right before closing

The answer is yes. Lenders pull borrowers' credit at the beginning of the approval process, and then again just prior to closing.

What do mortgage lenders not want to see

The two most common are insufficient credit and a high debt-to-income ratio. As far as bank statements are concerned, an underwriter might deny a loan if the sources of funds can't be verified or aren't “acceptable.” This could leave the borrower with too little verifiable cash to qualify.

What is the red flag rule in mortgage

Under the Red Flags Rules, financial institutions and creditors must develop a written program that identifies and detects the relevant warning signs – or “red flags” – of identity theft.

Can too many inquiries stop you from buying a house

Multiple inquiries from auto loan, mortgage or student loan lenders typically don't affect most credit scores. Second, you may also want to check your credit before getting quotes to understand what information is reported in your credit report.

Is it common to be denied a mortgage after pre-approval

Though it isn't common, lenders can deny your mortgage application after pre-approval. There are a few reasons this can happen, but all of them can be prevented with a little preparation and foresight.

Can I get denied after preapproval

Getting pre-approved for a loan only means that you meet the lender's basic requirements at a specific moment in time. Circumstances can change, and it is possible to be denied for a mortgage after pre-approval.

Can a loan be denied on closing day

Can a mortgage be denied after the closing disclosure is issued Yes. Many lenders use third-party “loan audit” companies to validate your income, debt and assets again before you sign closing papers. If they discover major changes to your credit, income or cash to close, your loan could be denied.

How many days before closing do they pull your credit

Lenders will typically pull your credit within seven days before closing. However, most lenders will only check with a “soft credit inquiry,” so your credit score won't be affected.

Do they check your credit during underwriting

Underwriters look at your credit score and pull your credit report. They look at your overall credit score and search for things like late payments, bankruptcies, overuse of credit and more.

What is red flag in mortgage

High-level Red Flags. Social Security number discrepancies within the loan file. Address discrepancies within the loan file. Verifications addressed to a specific party's attention. Verifications completed on the same day they were ordered.

Do mortgage lenders look at spending habits

They will look at things like how much you spend on credit cards, how much you spend on groceries, and how much you spend on entertainment. Mortgage lenders want to see that you are living within your means and that you are not spending more than you can afford.

What is the golden rule on a mortgage

The 28/36 rule states that your total housing costs should not exceed 28% of your gross monthly income and your total debt payments should not exceed 36%. Following this rule aims to keep borrowers from overextending themselves for housing and other costs.