How long does it take for mortgage Hard inquiries to fall off?

How do I get rid of hard inquiries on my mortgage

If you find an unauthorized or inaccurate hard inquiry, you can file a dispute letter and request that the bureau remove it from your report. The consumer credit bureaus must investigate dispute requests unless they determine your dispute is frivolous.

Cached

How many points does credit score drop with hard inquiry for mortgage

five points

How does a hard inquiry affect credit While a hard inquiry does impact your credit scores, it typically only causes them to drop by about five points, according to credit-scoring company FICO®.

Cached

How many hard inquiries is too many when buying a house

Each lender typically has a limit of how many inquiries are acceptable. After that, they will not approve you, no matter what your credit score is. For many lenders, six inquiries are too many to be approved for a loan or bank card.

Can a lender remove a hard inquiry

Disputing hard inquiries on your credit report involves working with the credit reporting agencies and possibly the creditor that made the inquiry. Hard inquiries can't be removed, however, unless they're the result of identity theft. Otherwise, they'll have to fall off naturally, which happens after two years.

Cached

Do hard inquiries affect buying a house

Here's why comparing rates can lower your credit score: Each time you apply for a home loan, a mortgage lender does an in-depth review of your credit report. This action is referred to as a hard inquiry, and it can impact your score. Read: Best FHA Loans.

How do I clear all loan inquiries

You can raise a dispute online with the credit agency on their website. Visit the 'dispute resolution' section and fill in the form with accurate details. Since the credit bureaus cannot make such changes on their own, they will verify the dispute with the financial institution.

How long is a credit pull good for mortgage

for 120 days

This initial credit inquiry is standard for all mortgage applications. Occasionally, the lender will need to pull your credit report again while the loan is processed. Credit reports are only valid for 120 days, so your lender will need a new copy if closing falls outside that window.

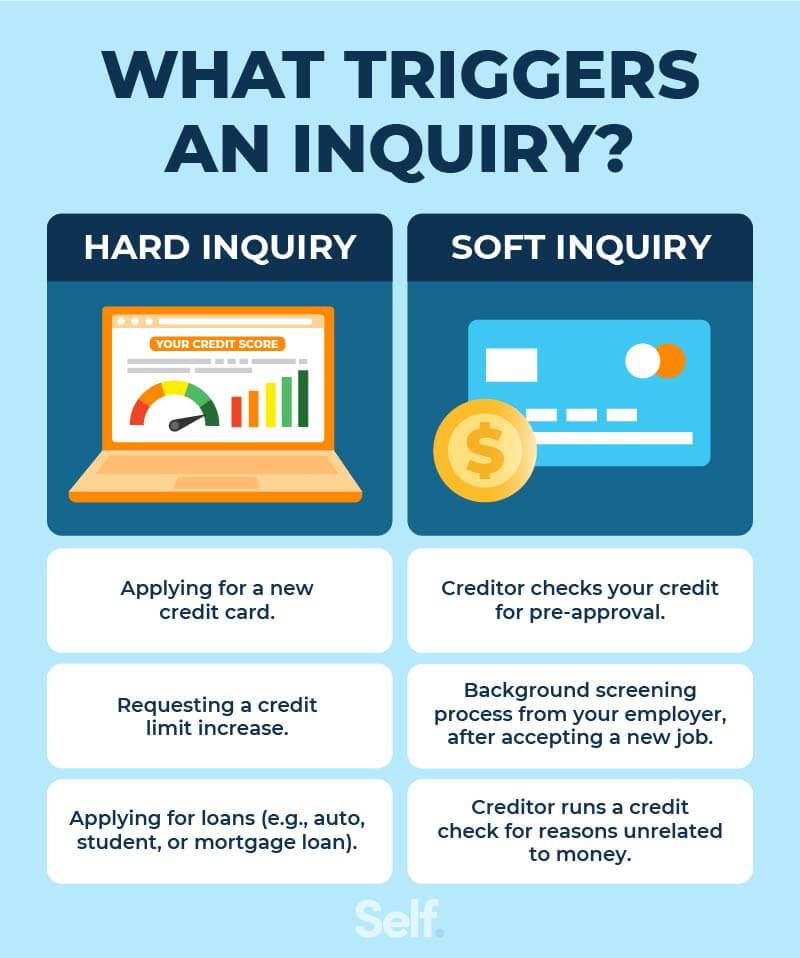

What do lenders see on a hard inquiry

A hard inquiry requests your full credit history and credit score from a credit bureau. The lender or creditor making the request has the option to choose the bureau and credit report style that best fit its needs. Most lenders will rely on one or more of the top three credit bureaus: Experian, TransUnion, and Equifax.

How far back do mortgage Lenders look at credit inquiries

The typical timeframe is the last six years. Your credit history is one of the many factors that can affect your ability to get approved for a mortgage and a lender can pull up one of your credit reports to see financial information about you, within minutes.

How many times can credit be pulled for mortgage

Number of times mortgage companies check your credit. Guild may check your credit up to three times during the loan process. Your credit is checked first during pre-approval. Once you give your loan officer consent, credit is pulled at the beginning of the transaction to get pre-qualified for a specific type of loan.

What is the easiest way to remove hard inquiries

If you find an inquiry on your credit report that you don't recognize, contact the creditor or the credit bureau to request its removal. You'll need to provide proof that the inquiry was unauthorized or fraudulent.

How many inquiries is too many for a loan

A hard inquiry occurs when a lender or creditor pulls your credit report to make a lending decision. Too many hard inquiries on your credit report can lower your credit score and suggest that you're a high-risk borrower. Generally, having more than six hard inquiries within a six-month period is considered too many.

How many times do mortgage companies pull credit

Number of times mortgage companies check your credit. Guild may check your credit up to three times during the loan process. Your credit is checked first during pre-approval. Once you give your loan officer consent, credit is pulled at the beginning of the transaction to get pre-qualified for a specific type of loan.

Can I buy a house with 661 credit score

Can I get a mortgage with an 661 credit score Yes, your 661 credit score can qualify you for a mortgage. And you have a couple of main options. With a credit score of 580 or higher, you can qualify for an FHA loan to buy a home with a down payment of just 3.5%.

Can too many inquiries stop you from buying a house

Multiple inquiries from auto loan, mortgage or student loan lenders typically don't affect most credit scores. Second, you may also want to check your credit before getting quotes to understand what information is reported in your credit report.

How bad is 3 hard inquiries

There's no such thing as “too many” hard credit inquiries, but multiple applications for new credit accounts within a short time frame could point to a risky borrower. Rate shopping for a particular loan, however, may be treated as a single inquiry and have minimal impact on your creditworthiness.

How many times can you get your credit pulled for a mortgage

Many borrowers wonder how many times their credit will be pulled when applying for a home loan. While the number of credit checks for a mortgage can vary depending on the situation, most lenders will check your credit up to three times during the application process.

How long do I have to shop for a mortgage without hurting your credit

When it comes to mortgages, however, lenders expect you to shop around and you can do so as much as you need to within 45 days of getting your first hard inquiry without harming your credit score further.

What credit score is needed to buy a 300k house

620-660

Additionally, you'll need to maintain an “acceptable” credit history. Some mortgage lenders are happy with a credit score of 580, but many prefer 620-660 or higher.

Is 642 a good credit score to buy a house

Your score falls within the range of scores, from 580 to 669, considered Fair. A 642 FICO® Score is below the average credit score. Some lenders see consumers with scores in the Fair range as having unfavorable credit, and may decline their credit applications.