How many loans do underwriters do in a day?

Can underwriting be done in a day

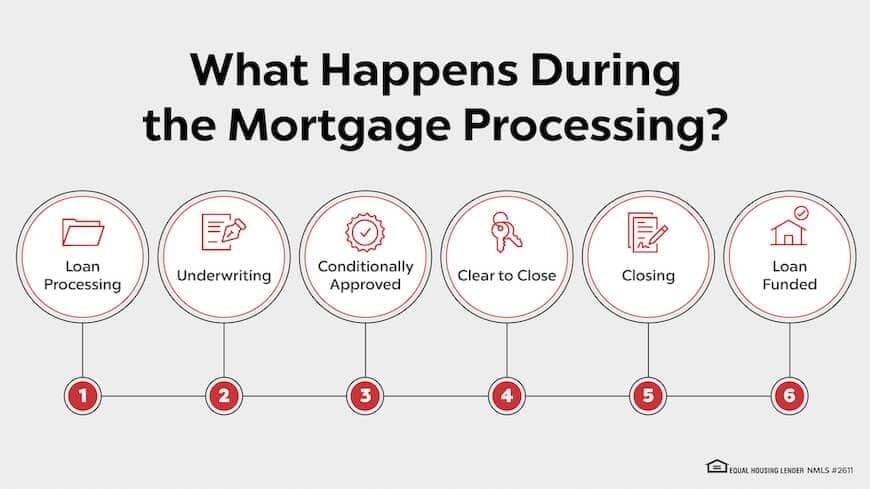

Underwriting—the process by which mortgage lenders verify your assets, check your credit scores, and review your tax returns before they can approve a home loan—can take as little as two to three days. Typically, though, it takes over a week for a loan officer or lender to complete the process.

Cached

How many loans fall through in underwriting

An underwriter denies a loan about 10% of the time. An application may be rejected because of high debt, irregular employment, or a low appraisal value. The entire underwriting process takes approximately 52 days to complete. Getting preapproved for a loan doesn't guarantee your loan application will be accepted.

How long should an underwriter take

between three to six weeks

How long does underwriting take The underwriting process typically takes between three to six weeks. In many cases, a closing date for your loan and home purchase will be set based on how long the lender expects the mortgage underwriting process to take.

Cached

How many hours a week does an underwriter work

Underwriting is typically a desk job with a standard 40-hour workweek, although overtime may be required as determined by each underwriting project. Evening and weekend hours are not uncommon. Working with computers and technology is a vital part of underwriting.

How often do underwriters deny loans

about 1 in 10

How often does an underwriter deny a loan A mortgage underwriter typically denies about 1 in 10 mortgage loan applications. A mortgage loan application can be denied for many reasons, including a borrower's low credit score, recent employment change or high debt-to-income ratio.

How many times does underwriter pull credit

Number of times mortgage companies check your credit. Guild may check your credit up to three times during the loan process. Your credit is checked first during pre-approval. Once you give your loan officer consent, credit is pulled at the beginning of the transaction to get pre-qualified for a specific type of loan.

How often do loans get denied in underwriting

You may be wondering how often underwriters denies loans According to the mortgage data firm HSH.com, about 8% of mortgage applications are denied, though denial rates vary by location and loan type. For example, FHA loans have different requirements that may make getting the loan easier than other loan types.

How likely is a loan to be denied in underwriting

About 8% of mortgage loans are denied in the underwriting process, so you've got about a 1 in 12 chance of having your mortgage denied after it once looked good enough to be approved.

Do underwriters work on weekends

Underwriters normally work regular business hours. They may occasionally need to work nights or weekends when they need to meet deadlines. An underwriter's salary may depend on their experience and certifications. The size, type and location of the business in which they work could also affect their salary.

Is underwriting a stressful job

Hardest part of being an Underwriter

Being an Underwriter is a stressful job, and telling people that the company can't cover them will never get any easier.

Is being a loan underwriter stressful

Yes, mortgage underwriting is a stressful job.

A mortgage underwriter considers layers of risk.

What not to do during underwriting

Tip #1: Don't Apply For Any New Credit Lines During Underwriting. Any major financial changes and spending can cause problems during the underwriting process. New lines of credit or loans could interrupt this process. Also, avoid making any purchases that could decrease your assets.

What can fail in underwriting

Your credit history or score is unacceptable.

This is typically only an issue in underwriting if your credit report expires before closing, and your scores have dropped. It can also become a problem if there's an error on your credit report regarding the date you completed a bankruptcy or foreclosure.

Do they pull your credit the day of closing

The answer is yes. Lenders pull borrowers' credit at the beginning of the approval process, and then again just prior to closing.

How worried should I be about underwriting

You shouldn't worry about underwriting if you meet the requirements for your loan type. Getting an initial approval helps because it gives you an idea of what you can afford – a lender uses your credit report, income, assets and debts to make a preliminary assessment of your qualifications.

What will make underwriter deny loan

An underwriter can deny a home loan for a multitude of reasons, including a low credit score, a change in employment status or a high debt-to-income (DTI) ratio. If they deny your loan application, legally, they have to provide you with a disclosure letter that explains why.

Is underwriting the final approval

Once the underwriter has determined that your loan is fit for approval, you'll be cleared to close.

Is underwriting a lot of math

A good underwriter is also detail-oriented and has excellent skills in math, communication, problem-solving, and decision-making. Although a university degree isn't a requirement across the board, some employers may hire you if you have relevant work experience and computer proficiency.

Do underwriters work a lot

Most underwriters work full time. Underwriters work in an office setting during regular business hours. They spend much of their time alone at a computer, most often working on applications but sometimes handling customer inquiries. Some property and casualty underwriters travel to assess properties in person.

Is underwriting a stable job

Job Outlook

Employment of insurance underwriters is projected to decline 4 percent from 2023 to 2031. Despite declining employment, about 8,400 openings for insurance underwriters are projected each year, on average, over the decade.