How much can you borrow on a 203k loan?

What is the maximum loan-to-value for 203k

Note: The maximum loan-to-value (LTV) factor is 96.5% for a purchase case and 97.75% for a refinance case.

What are the cons of a 203k loan

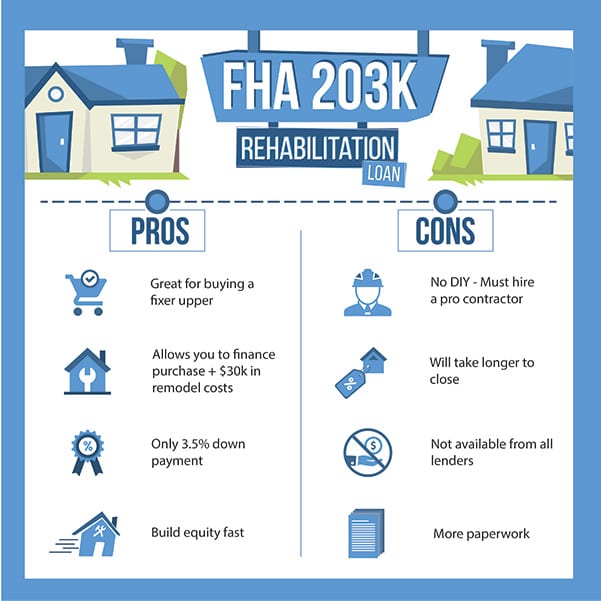

ConsOnly eligible for primary residences.Mortgage Insurance Premium (MIP) required (can be rolled into loan)Do it yourself work not allowed*More paperwork involved as compared to other loan options.

Are 203k rates higher

When financing either a FHA 203k renovation purchase or refinance transaction borrowers must keep in mind that the interest rate on the FHA 203k renovation loan is typically a . 5% higher than the standard FHA 203b loan.

Can you finish a basement with a 203k loan

FHA 203k program is flexible and allows a lot of leeway when it comes to the property you can buy and the repairs, renovations and upgrades you can complete as part of the loan. You can finance everything from second story additions, to finished basements, new kitchens or that large master suite you always wanted.

What is the debt-to-income ratio for a 203k loan

First, the Mortgage Payment Expense to Effective Income ratio (or front-end DTI) should not exceed 31 percent. Second, the Total Fixed Payment to Effective Income ratio (or back-end DTI) should not exceed 43 percent.

What is the debt-to-income ratio for FHA 203k

The max debt-to-income ratio for an FHA loan is 43%. In other words, your total monthly debts (including future monthly mortgage payments) shouldn't exceed 43% of your pre-tax monthly income if you want to qualify for an FHA loan.

Can you add a bathroom with a 203k loan

You can add bedrooms or bathrooms, expand a kitchen or dining room or even add a second story to the home. The FHA 203(k) covers home improvement projects from simple repairs to structural upgrades.

What is the minimum credit score for 203k

FHA 203(k) Loan Qualifications

Lenders require applicants to possess a credit score of at least 500. An FHA 203(k) loan requires a minimum down payment of 3.5% for those who possess a credit score of 580 or above, and 10% for those with a lower score.

What is the major advantage of a 203k loan through FHA

Here are some of the reasons an FHA 203(k) loan may be appealing to you: A low, 3.5 percent down payment is required. You make one payment every month (a combination of the mortgage and the improvements). The interest on your loan is tax-deductible like other mortgages.

How long does it take to close on a 203k mortgage

How long does it take for a 203k loan to close It will likely take 60 days or more to close a 203k loan, whereas a typical FHA loan might take 30-45 days. There is more paperwork involved with a 203k, plus a lot of back and forth with your contractor to get the final bids.

Can I get a mortgage with 55% DTI

There's not a single set of requirements for conventional loans, so the DTI requirement will depend on your personal situation and the exact loan you're applying for. However, you'll generally need a DTI of 50% or less to qualify for a conventional loan.

What is the max FHA debt-to-income ratio

Your DTI ratio measures the percentage of pre-tax income spent on monthly debt payments. FHA guidelines for DTI ratios vary depending on credit score and other financial considerations, such as cash on hand. The highest DTI allowed is 50 percent if the borrower has a credit score of 580 or higher.

What is the highest debt-to-income ratio for FHA

The maximum DTI for FHA loans is 57%. However, each lender is free to set its own requirements. This means some lenders may stick to the maximum DTI of 57% while others may set the limit closer to 40%. Do your research and speak with each lender you're considering working with.

How are 203k funds disbursed

A portion of the loan proceeds is used to pay the seller, or, if a refinance, to pay off the existing mortgage, and the remaining funds are placed in an escrow account and released as rehabilitation is completed.

What is the debt to income ratio for a 203k loan

First, the Mortgage Payment Expense to Effective Income ratio (or front-end DTI) should not exceed 31 percent. Second, the Total Fixed Payment to Effective Income ratio (or back-end DTI) should not exceed 43 percent.

What credit score is needed for a $350 000 house

Some mortgage lenders are happy with a credit score of 580, but many prefer 620-660 or higher.

What is the difference between a 203 B FHA loan and a 203 K FHA loan

FHA 203(b) Vs. FHA 203(k) An FHA 203(k) loan is used to assist home buyers who are purchasing a home in need of significant repairs or modifications. An FHA 203(b) loan, on the other hand, is primarily used for move-in ready homes.

What DTI is too high for mortgage

Lenders look at DTI when deciding whether or not to extend credit to a potential borrower, and at what rates. A good DTI is considered to be below 36%, and anything above 43% may preclude you from getting a loan.

What is the max DTI to qualify for a mortgage

As a general guideline, 43% is the highest DTI ratio a borrower can have and still get qualified for a mortgage. Ideally, lenders prefer a debt-to-income ratio lower than 36%, with no more than 28% of that debt going towards servicing a mortgage or rent payment.

Can I get a mortgage with 46 debt-to-income ratio

43% to 50%: Ratios falling in this range often show lenders that you have a lot of debt and may not be ready to take on a mortgage loan. 36% to 41%: Ratios in this range show lenders that you have reasonable amounts of debt and still have enough income to cover the cost of a mortgage should you get one.