How much down payment do you need for an ARM?

Do you have to put 20% down for an ARM

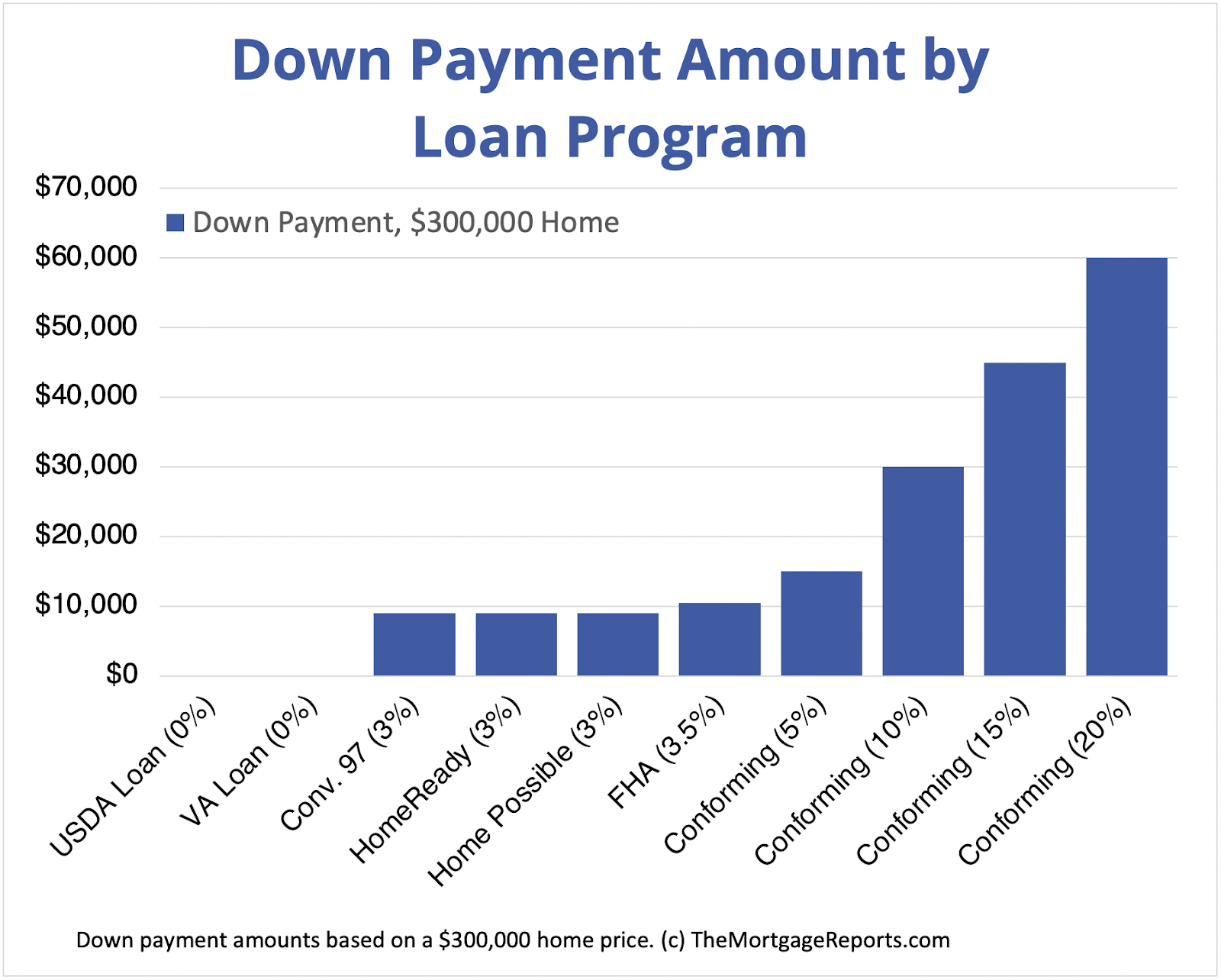

Conventional Adjustable-Rate Mortgage (ARM)

The down payment for an ARM is typically between 3 and 20% and will require PMI for buyers who put down less than 20%. With an ARM, the initial rate is often lower than a fixed-rate loan. However, the interest rate may go up over time.

Cached

Is it hard to qualify for an ARM loan

ARMs are easier to qualify for than fixed-rate loans, but you can get 30-year loan terms for both. An ARM might be better for you if you plan on staying in your home for a short period of time, interest rates are high or you want to use the savings in interest rate to pay down the principal on your loan.

What credit score do you need for an ARM

620 or above

Credit score: For a conventional ARM, you typically need a score of 620 or above to get approved, but Federal Housing Administration (FHA) ARMs can go as low as 580 or even 500 if you have a 10% down payment.

Cached

What are the payment options for an ARM

A payment-option ARM is a monthly adjusting adjustable-rate mortgage (ARM), which allows the borrower to choose between several monthly payment options, including the following: A 30 or 40-year fully amortizing payment. A 15-year fully amortizing payment. An interest-only payment.

What is the downside to getting an ARM

The big disadvantage of an ARM is the likelihood of your rate going up. If rates have risen since you took out the loan, your repayments will increase. Often, there's a cap on the annual/total rate increase, but it can still sting.

Is a 7 year ARM a bad idea

A 7/1 ARM is a good option if you intend to live in your new house for less than seven years or plan to refinance your home within the same timeframe. An ARM tends to have lower initial rates than a fixed-rate loan, so you can take advantage of the lower payment for the introductory period.

Is a 5 year ARM a good idea

A 5/1 adjustable-rate mortgage (ARM) loan may be worth considering if you're looking for a low monthly payment and don't plan to stay in your home long. Rates on 5/1 ARMs are typically lower than 30-year fixed-rate mortgages for those first five years.

What are bad things about ARM loans

Cons of an adjustable-rate mortgageRates and monthly payments may rise. The big disadvantage of an ARM is the likelihood of your rate going up.You could buy too much house. The lower initial payments could make it easier to qualify for a more expensive home.Difficulty with refinancing.

Is an ARM loan good 2023

The Pros of an Adjustable-Rate Mortgage

Here are some reasons for getting an ARM in 2023: ARMs often offer interest rates and entire point lower than the current 30-year fixed rate mortgages. And sometimes an ARM can even be lower than an entire point! This means big monthly savings for a buyer.

Can you do an ARM with an FHA loan

FHA offers a standard 1-year ARM and four "hybrid" ARM products. Hybrid ARMs offer an initial interest rate that is constant for the first 3-, 5-, 7-, or 10 years. After the initial period, the interest rate will adjust annually.

Can I pay off an ARM early

Some ARMs, including interest-only and payment-option ARMs, may require you to pay special fees or penalties if you refinance or pay off the ARM early (usually within the first 3 to 5 years of the loan).

Can you make pre payments on an ARM loan

A 5-year adjustable-rate mortgage (5/1 ARM) can be paid off early. However, there may be a prepayment penalty. A prepayment penalty requires additional interest owing on the mortgage.

Can you pay off an ARM early

Some ARMs, including interest-only and payment-option ARMs, may require you to pay special fees or penalties if you refinance or pay off the ARM early (usually within the first 3 to 5 years of the loan).

Why are ARM mortgages bad

ARMs require borrowers to plan for when the interest rate starts changing and monthly payments grow. Even with careful planning, though, you might be unable to sell or refinance when you want to. If you can't make the payments after the fixed-rate phase of the loan, you could lose the home.

Is a 7 year ARM locked for 7 years

With a 7/6 ARM, your introductory period is locked in for 7 years before any adjustments are made. This period gives you 7 years of predictable payments at a low interest rate. Flexibility: If you think your life may change in the next few years, an ARM loan can be a great idea and a way to save money.

What is the downfall of an ARM mortgage

The big disadvantage of an ARM is the likelihood of your rate going up. If rates have risen since you took out the loan, your repayments will increase. Often, there's a cap on the annual/total rate increase, but it can still sting.

Is a 7 year ARM worth it

If you're confident that you can make your monthly payments even if the interest rate reaches the maximum amount, then a 7/6 ARM is worth considering. A 7/6 ARM loan might also be worth the risk if you think you're only going to be in your home for a short period of time before you sell again.

Is it smart to do a 5 year ARM

A 5/1 adjustable-rate mortgage (ARM) loan may be worth considering if you're looking for a low monthly payment and don't plan to stay in your home long. Rates on 5/1 ARMs are typically lower than 30-year fixed-rate mortgages for those first five years.

What is the disadvantage of ARM mortgage

The big disadvantage of an ARM is the likelihood of your rate going up. If rates have risen since you took out the loan, your repayments will increase. Often, there's a cap on the annual/total rate increase, but it can still sting.

Is a 7 year ARM a good idea

If you're confident that you can make your monthly payments even if the interest rate reaches the maximum amount, then a 7/6 ARM is worth considering. A 7/6 ARM loan might also be worth the risk if you think you're only going to be in your home for a short period of time before you sell again.