How much will my credit score drop if I cosign for a car?

Does your credit score go down if you cosign for a car

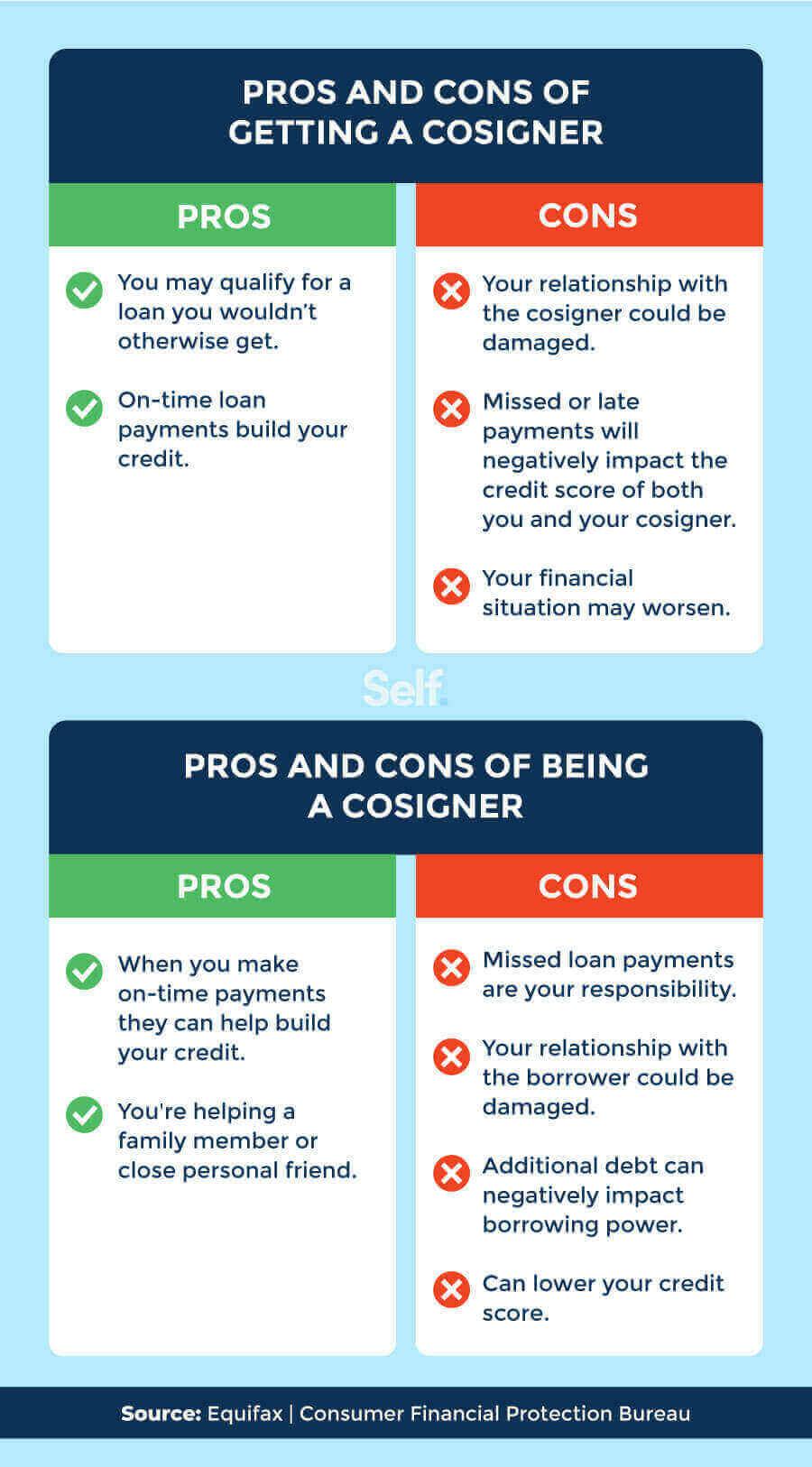

Being a co-signer itself does not affect your credit score. Your score may, however, be negatively affected if the main account holder misses payments.

Cached

How risky is it to cosign a car

Risks of cosigning

Credit risk: The auto loan will appear on both you and your cosigner's credit reports. If you miss a car payment or if the car is repossessed, you could do major damage to your cosigner's credit scores and cause them to be denied for loans and credit cards in the future.

Cached

Why did my credit score drop 50 points after paying off a car

Lenders like to see a mix of both installment loans and revolving credit on your credit portfolio. So if you pay off a car loan and don't have any other installment loans, you might actually see that your credit score dropped because you now have only revolving debt.

Does a cosigned car loan build credit

Having a co-signer on the loan will help the primary borrower build their credit score (as long as they continue to make on-time payments). It could also help the co-signer build their credit score and credit history, if the primary borrower makes on-time payments throughout the course of the loan.

Cached

Whose credit score is used when co-signing for a car

Whose credit is used for a co-signed auto loan In a co-signed auto loan, the lender will consider the credit scores of both the primary borrower and the co-signer.

Can I cosign for a car with a 500 credit score

So, if someone has a bad credit score, there is still a chance that they can be a cosigner. If the credit score is in the 500s, then it is relatively easier to get a loan, but that will come at a high-interest rate, but getting the loan will still be possible.

Why is it never a good idea to cosign a loan

Depending on how much debt you already have, the addition of the cosigned loan on your credit reports may make it look like you have more debt than you can handle. As a result, lenders may shy away from you as a borrower. It could lower your credit scores.

Is it ever a good idea to cosign

The bottom line is this: co-signing on a loan for anyone is never a good idea. If you feel compelled, lend them some money with a written agreement on how it is to be repaid. But never put your credit on the line by co-signing documents with a lender.

Can your credit score drop 100 points in a month

In the FICOscoring model, each hard inquiry — when a creditor checks your credit report before approving or denying credit — can cost you up to five points on your credit score. So, if you apply for more than 20 credit cards in one month, you could see a 100-point credit score drop.

How did my credit score drop 60 points in a month

Your credit score may have dropped by 60 points because negative information, like late payments, a collection account, a foreclosure or a repossession, was added to your credit report. Credit scores are based on the contents of your credit report and are adversely impacted by derogatory marks.

Who gets the credit on a cosigned car loan

Both the primary borrower and the cosigner on a loan will get credit if the primary borrower makes the payments on time. On the other hand, if the primary borrower does not keep up with the monthly payments, both their credit score and the cosigner's credit score will drop.

Is it smart to cosign for a car

Having a co-signer to help you with an auto loan application can make the approval process easier. You will often land more favorable loan terms and more affordable monthly payments. A co-signer can be particularly helpful if you're just beginning to build a credit profile or if your credit score needs improvement.

Can I cosign with a 650 credit score

Who Qualifies as a Cosigner To be a cosigner, your friend or family member must meet certain requirements. Although there might not be a required credit score, a cosigner typically will need credit in the very good or exceptional range—670 or better.

Will I need a cosigner with a 650 credit score

If you're planning to ask a friend or family member to co-sign on your loan or credit card application, they must have a good credit score with a positive credit history. Lenders and card issuers typically require your co-signer to have a credit score of 700 or above.

Whose credit score is used when buying a car with a cosigner

Whose credit score is used when buying a car with a co-signer Lenders can consider the credit scores of both borrowers when co-signing an auto loan. If you have a lower credit score, having a co-signer with a higher score could work in your favor.

Who gets the credit on a cosigned loan

Both the primary borrower and the cosigner on a loan will get credit if the primary borrower makes the payments on time. On the other hand, if the primary borrower does not keep up with the monthly payments, both their credit score and the cosigner's credit score will drop.

Whose credit score is used with a co-signer

Whose credit score is used when buying a car with a co-signer Lenders can consider the credit scores of both borrowers when co-signing an auto loan. If you have a lower credit score, having a co-signer with a higher score could work in your favor.

How did my credit score drop 40 points

Your credit score may have dropped by 40 points because a late payment was listed on your credit report or you became further delinquent on past-due bills. It's also possible that your credit score fell because your credit card balances increased, causing your credit utilization to rise.

Why did my credit score drop 40 points after paying off debt

It's possible that you could see your credit scores drop after fulfilling your payment obligations on a loan or credit card debt. Paying off debt might lower your credit scores if removing the debt affects certain factors like your credit mix, the length of your credit history or your credit utilization ratio.

How can my credit score drop 80 points in a month

Your credit score may have dropped by 80 points because negative information, like late payments, a collection account, a foreclosure or a repossession, was added to your credit report. Credit scores are based on the contents of your credit report and are adversely impacted by derogatory marks.