Is a 5’6 ARM a good idea?

Is a 5-year ARM a good idea in 2023

Is an ARM a good idea in 2023 ARMs are generally only a good idea if rates are likely to drop by the time your rate would adjust, or if you're confident you'll be able to sell or refinance before it does. Most major forecasts expect mortgage rates to trend down over the next couple of years.

Cached

Is a 5-year ARM worth it

A 5/1 adjustable-rate mortgage (ARM) loan may be worth considering if you're looking for a low monthly payment and don't plan to stay in your home long. Rates on 5/1 ARMs are typically lower than 30-year fixed-rate mortgages for those first five years.

Cached

Is a 5-year ARM risky

The biggest disadvantage of an ARM is the risk of interest rate hikes. For example, it's possible a 5/1 ARM with a 4.5% start rate could (worst case) increase as follows: Beginning of year six: 6.5% Starting year seven: 8.5%

Cached

What may be a concern if you have an adjustable-rate mortgage ARM

An adjustable-rate mortgage (ARM) is a loan with an interest rate that changes. ARMs may start with lower monthly payments than fixed-rate mortgages, but keep in mind the following: Your monthly payments could change. They could go up — sometimes by a lot—even if interest rates don't go up.

Cached

What are the disadvantages of ARM

The big disadvantage of an ARM is the likelihood of your rate going up. If rates have risen since you took out the loan, your repayments will increase. Often, there's a cap on the annual/total rate increase, but it can still sting.

What happens after 5 years in a 5-year ARM

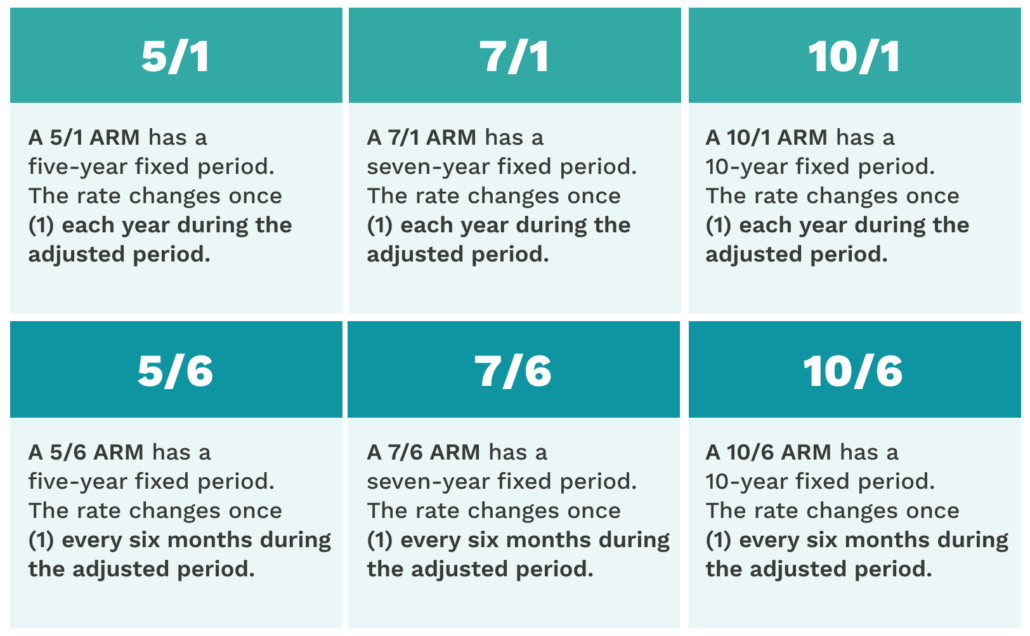

With a 5/1 ARM, the first five years come with a fixed interest rate. Once this initial five-year period is over, the interest rate switches to an adjustable rate for the remainder of the term.

What is the downside to getting an ARM

The big disadvantage of an ARM is the likelihood of your rate going up. If rates have risen since you took out the loan, your repayments will increase. Often, there's a cap on the annual/total rate increase, but it can still sting.

Can you pay off a 5 1 ARM early

Can you pay off a 5/1 ARM early Yes, you can pay off the loan early, either by selling the property or refinancing the original loan. Many 5/1 ARMs come with prepayment penalties.

Is a 5 6 ARM bad

The biggest danger associated with a 5/6 hybrid ARM is interest rate risk. Because the interest rate can increase every six months after the first five years, the monthly mortgage payments could rise significantly and even become unaffordable if the borrower keeps the mortgage for that long.

What is the downfall of an ARM mortgage

The big disadvantage of an ARM is the likelihood of your rate going up. If rates have risen since you took out the loan, your repayments will increase. Often, there's a cap on the annual/total rate increase, but it can still sting.

What is the downside of an adjustable interest rate

Cons of an adjustable-rate mortgage

Rates and payments can rise significantly over the life of the loan. Some annual caps don't apply to the initial loan adjustment. ARMs are more complex than their fixed-rate counterparts, including features like margins, caps and adjustment indexes.

Who would benefit from an ARM mortgage

ARMs are easier to qualify for than fixed-rate loans, but you can get 30-year loan terms for both. An ARM might be better for you if you plan on staying in your home for a short period of time, interest rates are high or you want to use the savings in interest rate to pay down the principal on your loan.

Why would someone want an ARM mortgage

Many homeowners choose an ARM to take advantage of the lower mortgage rates during the initial period. You may consider an adjustable-rate mortgage if: You plan on moving or selling your home within five years, or before the adjustment period of the loan. Interest rates are high when you buy your home.

What are the benefits of a 5-year ARM mortgage

A 5-year ARM offers these benefits:It has a lower initial interest rate and, therefore, a lower monthly mortgage payment in the early term than a fixed-rate mortgage.It allows you to save money that can be invested or put it towards financial goals like saving for retirement or paying off credit card debt.

Can you pay off 5 year ARM early

Can you pay off a 5/1 ARM early Yes, you can pay off the loan early, either by selling the property or refinancing the original loan. Many 5/1 ARMs come with prepayment penalties.

Is it hard to live with one ARM

If you only have the use of one hand or arm, doing your day-to-day activities can be hard. If you have lost your dominant hand you will need to use your other hand for most tasks like feeding or writing, at least in the beginning.

Will mortgage interest rates go down in 2023

“[W]ith the rate of inflation decelerating rates should gently decline over the course of 2023.” Fannie Mae. 30-year fixed rate mortgage will average 6.4% for Q2 2023, according to the May Housing Forecast. National Association of Realtors (NAR).

Is it harder to refinance an ARM

Can You Refinance An ARM Loan You can refinance an adjustable-rate mortgage, and it's just as easy as refinancing any other loan. By refinancing, the borrower is replacing their existing loan with a new, updated loan – usually a fixed-rate mortgage.

Are ARM loans a bad idea

Using an ARM may also make sense if you're looking for a starter home and may not be able to afford a fixed-rate mortgage. Historically, says McCauley, most first- and second-time homebuyers only stay in a home an average of five years, so ARMs are often a safe bet.

Do ARM loans make sense

There are many good reasons to consider applying for an ARM, including: Lower initial interest rates. An ARM generally comes with a lower initial interest rate than that of a comparable fixed-rate mortgage, giving you lower monthly payments — at least for the fixed period of the loan. Afford a more expensive home.