Is a pay for delete letter legal?

Can you pay for a deletion

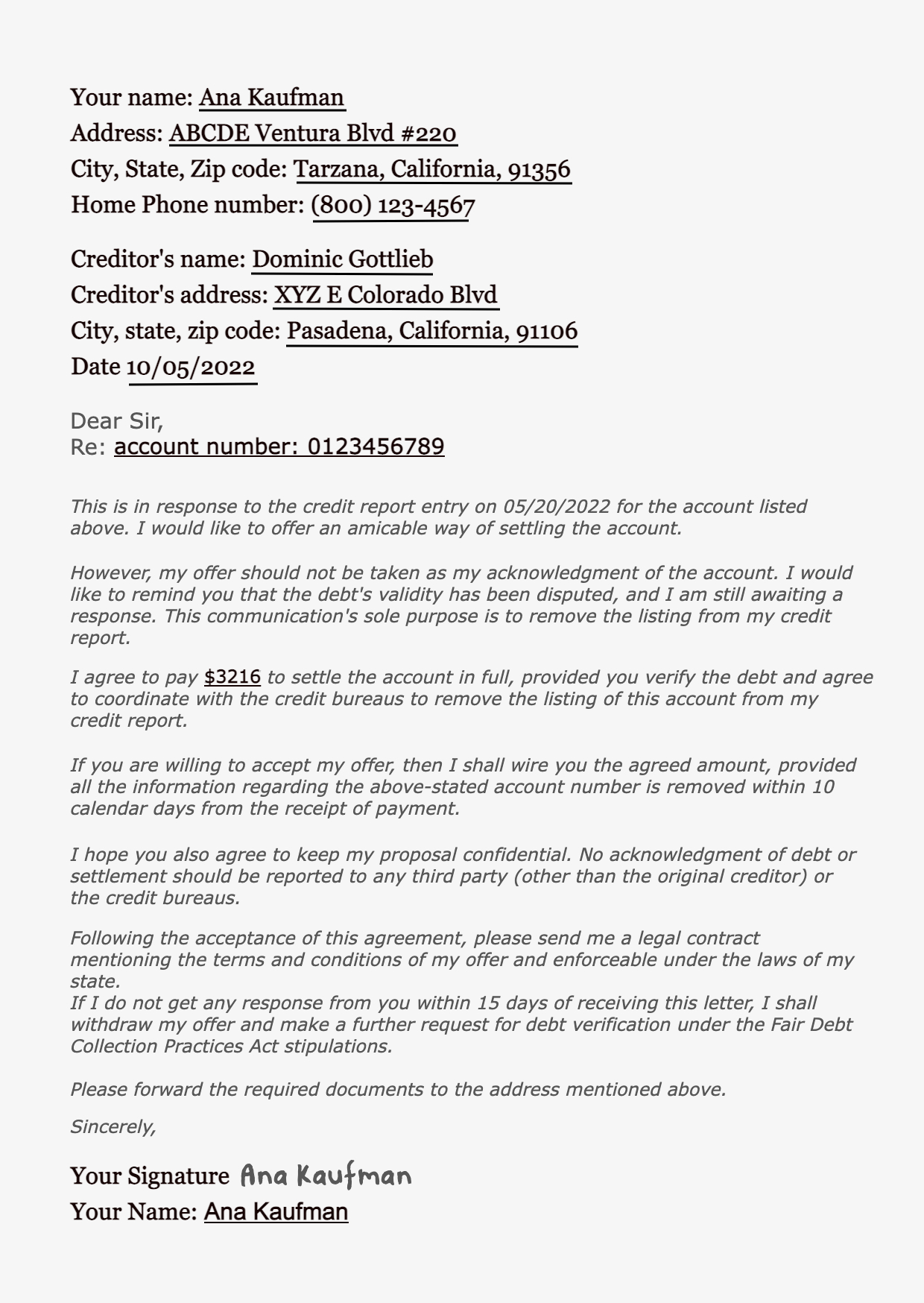

Pay for delete refers to the process of getting a debt collector to remove collection account removed from your credit report. It's a point you can use during a debt settlement negotiation, as you settle a debt for less than you owe. You agree to pay a certain amount of money in your settlement.

Cached

What is a pay to delete letter with payment

A pay for delete letter is sent to debt collectors to negotiate the removal of negative information from their credit report. The letter proposes a single payment (commonly 50%+ of the owed balance) in exchange for clearing the debt from the major credit reporting bureaus.

Cached

Is a pay for delete binding

Pay for delete isn't legally binding

If you do get a pay for delete arrangement settled with a creditor, they may not actually follow through after you make your payment—and you probably won't have any legal recourse. Creditors may even temporarily delete your debt and later report it again.

Cached

How do you negotiate a pay for delete letter

Here are a few easy things you can say right away once you're on the phone with your creditor:Ask for a “pay for delete.”Offer lower payment to your creditor.Negotiate with them and agree on a figure to settle on.If you can afford to pay your creditor in full, do so.

Cached

How much should you pay for a pay to delete

Basically, you will agree to pay the entire amount owed and they agree to remove the collection from your credit report. Even if you are strapped for cash, most people can afford to pay $500 to a collection agency. If it's over $500, I still think this is an excellent technique.

Should I ask for pay for delete

Generally speaking, consumers should not use pay for delete to address a collection account on their credit reports. Here's why you shouldn't rely on pay for delete when trying to improve your credit score: The process is discouraged.

Why is pay for delete bad

If you pay off an account in collections, it will still appear on your credit reports as a paid collection. And pay for delete won't remove the negative information reported by the original creditor, such as late payments.

Should I request a pay for delete or just pay off debt

Pay the bill, even without a pay-for-delete offer.

If you are able to get a pay-for-delete from a collection agency, it may help your credit. But the delinquent account with the original creditor will still remain on your credit report. A collection account paid in full reflects better on your credit report.

How can I get a collection removed without paying

You can ask the creditor — either the original creditor or a debt collector — for what's called a “goodwill deletion.” Write the collector a letter explaining your circumstances and why you would like the debt removed, such as if you're about to apply for a mortgage.

How much should I offer pay for delete

With this in mind, you should always start your offer at 25 percent or less. Let's understand the math here. If your debt is $1,000, let's say at the most, the collection agencies have paid or will collect 7 cents on the dollar, or $70. If you offer them $250 (25 percent), they are still making a profit of $180.

How do you negotiate collections pay for delete

Start by offering cents on every dollar you owe, say around 20 to 25 cents, then 50 cents on every dollar, then 75. The debt collector may still demand to collect the full amount that you owe, but in some cases they may also be willing to take a slightly lower amount that you propose.

What is the 11 word credit loophole

In case you are wondering what the 11 word phrase to stop debt collectors is supposed to be its “Please cease and desist all calls and contact with me immediately.”

Does pay for delete increase credit score

Typically, your debt history will stay on your credit report for seven years even after you pay it, but pay for delete is a process meant to remove the account sooner. This may seem like an effective way to improve your credit score, but the strategy is discouraged under the Fair Credit Reporting Act.

What does the 15 3 credit hack do

The 15/3 hack can help struggling cardholders improve their credit because paying down part of a monthly balance—in a smaller increment—before the statement date reduces the reported amount owed. This means that credit utilization rate will be lower which can help boost the cardholder's credit score.

Can a 10 year old debt still be collected

Debt collectors may not be able to sue you to collect on old (time-barred) debts, but they may still try to collect on those debts. In California, there is generally a four-year limit for filing a lawsuit to collect a debt based on a written agreement.

How many points will my credit score increase if a collection is deleted

One of the ways to delete a collection account is to call the collection agency and try to negotiate with them. Ask them to delete the collection in exchange for paying off your debt. Also, get the agreement in writing. If they accept it, your credit could increase by as much as 100 points.

What is the credit secret loophole

A 609 Dispute Letter is often billed as a credit repair secret or legal loophole that forces the credit reporting agencies to remove certain negative information from your credit reports.

How to raise 420 credit score

Steps to Improve Your Credit ScoresBuild Your Credit File.Don't Miss Payments.Catch Up On Past-Due Accounts.Pay Down Revolving Account Balances.Limit How Often You Apply for New Accounts.

How long before a debt becomes uncollectible

four years

The statute of limitations on debt in California is four years, as stated in the state's Code of Civil Procedure § 337, with the clock starting to tick as soon as you miss a payment.

Why did my credit score drop when I paid off collections

This is because your total available credit is lowered when you close a line of credit, which could result in a higher credit utilization ratio. Additionally, if the account you closed was your oldest line of credit, it could negatively impact the length of your credit history and cause a drop in your scores.