Is a pre approval a hard inquiry?

Is pre-approval a hard or soft pull

hard inquiry

A pre-approved offer will be sent out after a soft inquiry indicates that you're a good prospect for additional credit. If you apply based on the offer, the lender may make a hard inquiry before issuing the credit. A soft inquiry has no impact on your credit rating.

Cached

How many pre approvals can I get without hurting my credit

While many home buyers will only need one mortgage preapproval letter, there really is no limit to the number of times you can get preapproved. In fact, you can — and should — get preapproved with multiple lenders. Many experts recommend getting at least three preapproval letters from three different lenders.

Cached

What credit score is needed for pre-approval

620 or higher

It's recommended you have a credit score of 620 or higher when you apply for a conventional loan. If your score is below 620, lenders either won't be able to approve your loan or may be required to offer you a higher interest rate, which can result in higher monthly payments.

Will pre approval hurt credit score

A mortgage preapproval can have a hard inquiry on your credit score if you end up applying for the credit. Although a preapproval may affect your credit score, it plays an important step in the home buying process and is recommended to have. The good news is that this ding on your credit score is only temporary.

How hard does a pre approval affect credit score

Does getting a prescreened pre-approved offer hurt your credit The short answer is: No. That's because a prescreened pre-approval involves a soft inquiry, which doesn't affect your credit scores. The prescreen soft inquiry is simply a way for lenders to determine if you may qualify for their credit card offer.

Can I get denied if I’m pre-approved

Getting pre-approved for a loan only means that you meet the lender's basic requirements at a specific moment in time. Circumstances can change, and it is possible to be denied for a mortgage after pre-approval.

Do they run your credit for a pre-approval

A mortgage preapproval can have a hard inquiry on your credit score if you end up applying for the credit. Although a preapproval may affect your credit score, it plays an important step in the home buying process and is recommended to have. The good news is that this ding on your credit score is only temporary.

Does pre-approval line of credit hurt your credit

Here's the good news: Preapproved credit card offers do not impact your credit score in any way. That's because creditors only place a “soft pull” on your credit report to determine your eligibility. You'll only see an impact if you move forward with the application.

Is it bad to get pre-approved too early

As a home buyer, pre-approvals are for your benefit, so it's never too early to get one. Getting pre-approved early is an advantage because one-third of mortgage applications contain an error. These errors can negatively affect your interest rate and ability to buy a home.

Why did my credit score drop after pre-approval

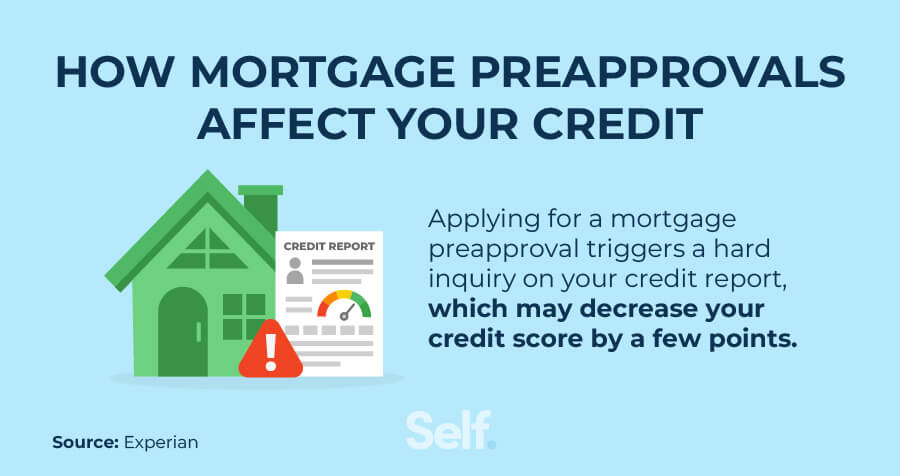

This occurs when a lender is considering extending a line of credit to you. Hard inquiries show up on your credit report and can affect your credit scores. For example, if you apply for a pre-approval offer, it will trigger a hard inquiry, and you could see a dip in your credit scores.

Do they run your credit again after pre-approval

An initial credit inquiry during the pre-approval process. A second pull is less likely, but may occasionally occur while the loan is being processed. A mid-process pull if any discrepancies are found in the report. A final monitoring report may be pulled from the credit bureaus in case new debt has been incurred.

Does applying for a pre-approval hurt your credit

Fortunately, in most cases, a preapproval has no direct impact on your credit since the process typically involves a soft inquiry of your credit. If you respond to a preapproved offer from a credit card issuer and submit an application, the card issuer will do a more thorough review of your credit.

How hard does a pre-approval affect credit score

Does getting a prescreened pre-approved offer hurt your credit The short answer is: No. That's because a prescreened pre-approval involves a soft inquiry, which doesn't affect your credit scores. The prescreen soft inquiry is simply a way for lenders to determine if you may qualify for their credit card offer.

How guaranteed is a pre approval

A prequalification or preapproval letter is a document from a lender stating that the lender is tentatively willing to lend to you, up to a certain loan amount. This document is based on certain assumptions and it is not a guaranteed loan offer.

How many points is a hard inquiry

five points

How does a hard inquiry affect credit While a hard inquiry does impact your credit scores, it typically only causes them to drop by about five points, according to credit-scoring company FICO®. And if you have a good credit history, the impact may be even less.

How soon is too soon to get preapproved for a mortgage

The best time to get pre-approved for a mortgage is at least one year before you decide to purchase. As a home buyer, pre-approvals are for your benefit, so it's never too early to get one. Getting pre-approved early is an advantage because one-third of mortgage applications contain an error.

Is your credit ran again after pre-approval

An initial credit inquiry during the pre-approval process. A second pull is less likely, but may occasionally occur while the loan is being processed. A mid-process pull if any discrepancies are found in the report. A final monitoring report may be pulled from the credit bureaus in case new debt has been incurred.

Why did my credit score drop 40 points after paying off debt

It's possible that you could see your credit scores drop after fulfilling your payment obligations on a loan or credit card debt. Paying off debt might lower your credit scores if removing the debt affects certain factors like your credit mix, the length of your credit history or your credit utilization ratio.

What can go wrong after pre-approval

Many situations in which a prospective homebuyer is denied for mortgage after pre-approval result from changes in the homebuyer's finances or other new information.Debt Increase.Credit Report Information.Change in Income.Change in Job.Unusual Financial Activity.Change in Lender or Loan Requirements.Ask Your Lender Why.

Why would you get denied after pre-approval

Buyers are denied after pre-approval because they increase their debt levels beyond the lender's debt-to-income ratio parameters. The debt-to-income ratio is a percentage of your income that goes towards debt. When you take on new debt without an increase in your income, you increase your debt-to-income ratio.