Is insurance debit or credit in profit and loss account?

Where is insurance shown in profit and loss account

A related account is Insurance Expense, which appears on the income statement and shown on balance sheet as asset.

Is insurance a credit or debit

debit

The amount paid for insurance raises the company's asset total, hence it is recorded as a debit in the books of accounts.

Is insurance an item in profit and loss account

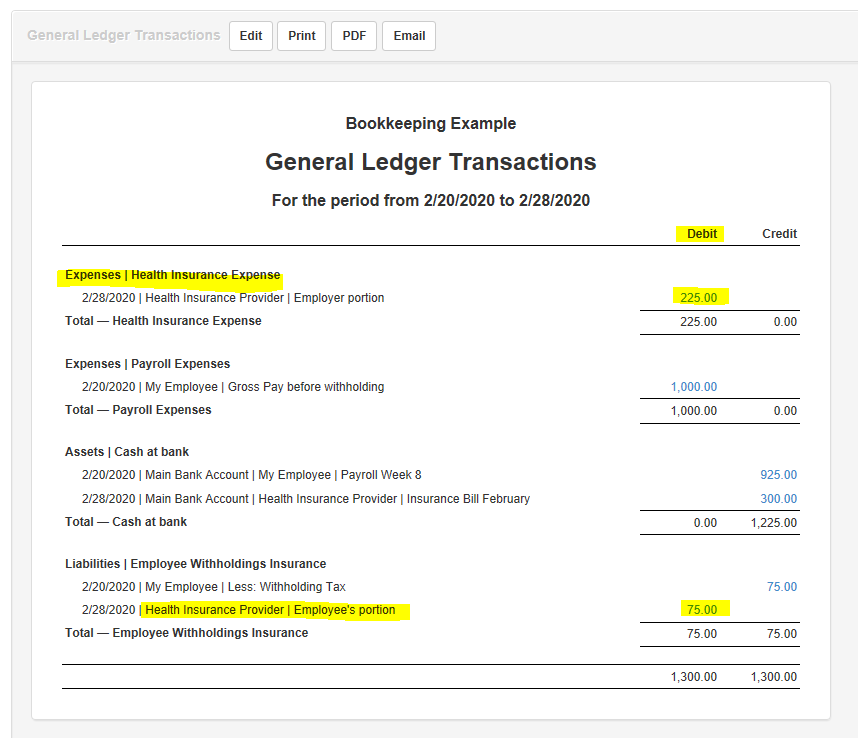

Insurance expense will be one of the categories that your income statement lists as an expenditure. Because the income statement reflects business activity over a period of time, this line on your income statement will aggregate any insurance payments your business made during the period that the statement covers.

Cached

Is insurance expense a debit

Is insurance expense debit or credit The insurance expense account will be debited, and the prepaid insurance account will be credited when the asset is charged to expenses. As a result, the amount assigned to an accounting period as an expense is merely the amount of the prepaid insurance asset.

Where do you put insurance in accounting

At the end of any accounting period, the amount of the insurance premiums that remain prepaid should be reported in the current asset account, Prepaid Insurance. The prepaid amount will be reported on the balance sheet after inventory and could part of an item described as prepaid expenses.

Where does insurance go in accounting

When the insurance coverage comes into effect, it is moved from an asset and charged to the expense side of the company's balance sheet. Insurance coverage, though, is often consumed over several periods. In this case, the company's balance sheet may show corresponding charges recorded as expenses.

Does insurance count as credit

The short answer is no. There is no direct affect between car insurance and your credit, paying your insurance bill late or not at all could lead to debt collection reports.

What items are on the debit side of profit and loss

Items included on the debit side are opening stock, purchases, and direct expenses and on the credit side are sales and closing stock. The resultant figure is either gross profit or gross loss.

How is insurance recorded in accounting

At the end of any accounting period, the amount of the insurance premiums that remain prepaid should be reported in the current asset account, Prepaid Insurance. The prepaid amount will be reported on the balance sheet after inventory and could part of an item described as prepaid expenses.

Which account is insurance debited

As the prepaid amount expires, the balance in Prepaid Insurance is reduced by a credit to Prepaid Insurance and a debit to Insurance expense. Was this answer helpful

Is insurance an expense or liability

This is because the insurance protects the business from liability, and the cost of the insurance is directly related to the risk of liability. This expense category is typically used for all types of insurance, such as property insurance, health insurance, and liability insurance.

How is insurance classified in accounting

Any insurance premium costs that have not expired as of the balance sheet date should be reported as a current asset such as Prepaid Insurance. The costs that have expired should be reported in income statement accounts such as Insurance Expense, Fringe Benefits Expense, etc.

Where is insurance recorded in income statement

Generally, the insurance premium is paid monthly or quarterly. The expense, unexpired and prepaid, is reported in the books of accounts under under current assets.

What expense category is insurance

Operating expenses are the costs associated with running a business on a day-to-day basis, including rent, utilities, and salaries. Insurance fits into this category because it's something businesses have to pay regularly in order to protect their assets and employees.

What is credit in insurance

Credit insurance is a type of insurance policy purchased by a borrower that pays off one or more existing debts in the event of a death, disability, or in rare cases, unemployment.

Why is insurance based on credit

The reason insurers check your credit is because studies have shown that credit rating tends to be a good indicator of how many claims a driver will file. That allows insurers to match more expensive rates with drivers who will likely use their insurance more.

Which items are not shown in profit and loss account

Withdrawal of capital is not shown in profit or loss appropriation account.

Which of the following expenses will be shown in the profit and loss account

Expenses included in the profit and loss account are Selling and distribution expenses, Freight & carriage on sales, Sales tax, Administrative Expenses, Financial Expenses, Maintenance, depreciation and Provisions and more.

Where does insurance fall in accounting

All policies come with premiums. If they expire, they must be recorded as an expense. Unexpired premiums should be listed as prepaid insurance, which is listed in an asset account.

What type of account is insurance in accounting

Account Types

| Account | Type | Debit |

|---|---|---|

| INSURANCE EXPENSE | Expense | Increase |

| INSURANCE PAYABLE | Liability | Decrease |

| INTEREST EXPENSE | Expense | Increase |

| INTEREST INCOME | Revenue | Decrease |