Is it better to use USDA loan or conventional?

What are the disadvantages of a USDA loan

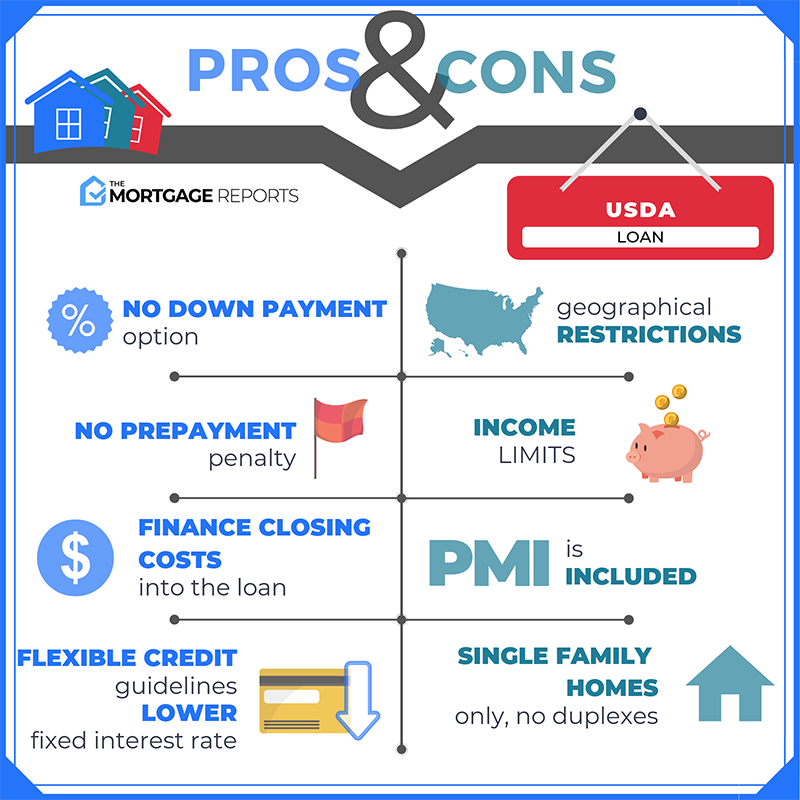

Strict geographical and income requirements.Income-producing activities may be prohibited.Mortgage insurance cannot be removed.Longer underwriting times.Second homes are not eligible.Duplexes are not eligible.No refinancing options for non-USDA borrowers.Cash-out refinancing is not available.

Are USDA rates higher than conventional

In many cases, interest rates for USDA loans are lower than rates for conventional loans. The government backing of USDA loans typically means that lenders can issue them with competitive interest rates.

Cached

For which buyer would a USDA loan be most appropriate

A USDA loan is a great option for buyers with moderate or low income. It lets you buy a house with no money down and low mortgage rates — two huge benefits that only one other loan program (the VA loan) offers.

What is the difference between a USDA loan and a conventional loan

To qualify for a USDA mortgage, the property must be located in an eligible rural area as defined by the USDA. Conventional loans don't have these restrictions on location, but you'll need to meet other eligibility requirements.

Cached

Does USDA annual fee ever go away

The applicable upfront guarantee fee and/or annual fee may differ for a purchase and refinance transaction. The annual fee will cease to be collected when 80% loan to value (LTV) is achieved. WAY TO GO! Thank you for supporting the USDA Single Family Housing Guaranteed Loan Program!

Is USDA more strict than FHA

USDA home loans have stricter income limits than FHA loans and also require you to live in an eligible rural area. Your home address and annual household income determine your borrower eligibility for USDA loans. FHA borrower requirements, on the other hand, are more lenient as you can have a lower credit score.

What is the advantage of a USDA loan

The main benefit to you is that you can get low mortgage interest rates, even without a down payment. Be aware, however, that if you put little or no money down you will have to pay a mortgage insurance premium. The loan term is a 30-year fixed-rate mortgage.

Is USDA stricter than FHA

USDA home loans have stricter income limits than FHA loans and also require you to live in an eligible rural area. Your home address and annual household income determine your borrower eligibility for USDA loans. FHA borrower requirements, on the other hand, are more lenient as you can have a lower credit score.

Is it easier to get approved for FHA or USDA

The process of getting a USDA loan may take longer than an FHA loan, largely because USDA loans are underwritten twice, first by the lender and then by the USDA. To have the loan automatically underwritten by the USDA, you'll need a credit score of 640 or higher.

Why do lenders prefer conventional loans

This type of loan uses lower interest rates and less strict credit score requirements. Conventional loans are not backed by a government agency and often use conforming loan limits.

What is the USDA upfront fee for 2023

1.0%

The USDA Loan fees for FY 2023 are an upfront guarantee fee of 1.0% of the loan amount and an annual fee of 0.35% of the loan amount. These fees apply to both home purchases and refinance transactions during the 2023 fiscal year, which runs October 1, 2023, through September 30, 2023.

Does PMI go away on USDA loans

Private mortgage insurance (PMI) is the term used for mortgage insurance on conventional (non-government-backed) loans. So no, USDA loans don't require PMI; only conventional loans have PMI, and only on those loans where the borrower has less than 20% equity in their home.

Which one is better a USDA loan or an FHA loan

A USDA home loan is often the best choice for borrowers who meet the U.S. Department of Agriculture's guidelines. With no down payment requirement and low mortgage insurance rates, USDA mortgages are often cheaper than FHA loans, both upfront and in the long run.

What is one advantage a USDA loan has over the FHA loan

An FHA loan requires you to make a down payment of 3.5% if your credit score is 580 or higher. For a credit score range of 500 – 579, you'll need a 10% down payment. USDA loans, on the other hand, do not require you to come up with a down payment at all. That's one of the most appealing factors of a USDA loan.

How often do underwriters deny USDA loans

An underwriter denies a loan about 10% of the time. An application may be rejected because of high debt, irregular employment, or a low appraisal value. The entire underwriting process takes approximately 52 days to complete. Getting preapproved for a loan doesn't guarantee your loan application will be accepted.

Are USDA loans more strict than FHA

USDA home loans have stricter income limits than FHA loans and also require you to live in an eligible rural area. Your home address and annual household income determine your borrower eligibility for USDA loans. FHA borrower requirements, on the other hand, are more lenient as you can have a lower credit score.

Why would an underwriter deny a USDA loan

Things like unverifiable income, undisclosed debt, or even just having too much household income for your area can cause a loan to be denied. Talk with a USDA loan specialist to get a clear sense of your income and debt situation and what might be possible.

What are the disadvantages of conventional finance

Conventional loan disadvantages

Even though the rate is great, the term won't allow you to operate your new location profitably because your monthly payments will be higher to meet the repayment schedule." "Conventional loans do not allow for projection-based financing."

Why would a house only go conventional

Sellers often prefer conventional buyers because of their own financial views. Because a conventional loan typically requires higher credit and more money down, sellers often deem these reasons as a lower risk to default and traits of a trustworthy buyer.

Can you get rid of USDA annual fee

USDA may assess a late fee to the lender if the annual fee is not paid when due. The applicable upfront guarantee fee and/or annual fee may differ for a purchase and refinance transaction. The annual fee will cease to be collected when 80% loan to value (LTV) is achieved.