Is it hard to get conventional loan?

What can stop you from getting a conventional loan

Your credit score might be the most important conventional mortgage requirement. If your score is not at least 620, you can't get approved. Your credit score also affects the mortgage rates lenders will offer you. The higher the score, the lower your rate.

Cached

What credit score is needed for a conventional loan

620

Credit score: In most cases, you'll need a credit score of at least 620 to qualify for a conventional loan. When you apply, your lender will check your credit history to determine if you have good credit. If you don't, you might not get approved for the loan.

Cached

Is it harder to get a conventional loan or FHA

FHA loans and conventional loans are two of the most common mortgages. FHA loans are backed by the Federal Housing Administration (FHA) and offered by FHA-approved lenders. These loans are generally easier to qualify for than conventional loans and have smaller down payment requirements.

Cached

How long does it take to get a conventional loan

Approval normally takes a few weeks to process, while closing takes an additional few weeks. This is what makes the process last for roughly 50 days. Calculate your monthly mortgage payments with Total Mortgage's Purchase Calculator and get a feel for what you can afford.

Is it easier to qualify for a conventional loan

It's easier to qualify for a conventional loan than many first-time home buyers expect. You'll need a minimum credit score of 620 as well as two consecutive years of stable income and employment.

How often do conventional loans get denied

An underwriter denies a loan about 10% of the time. An application may be rejected because of high debt, irregular employment, or a low appraisal value. The entire underwriting process takes approximately 52 days to complete. Getting preapproved for a loan doesn't guarantee your loan application will be accepted.

How much down payment do you need for a conventional loan

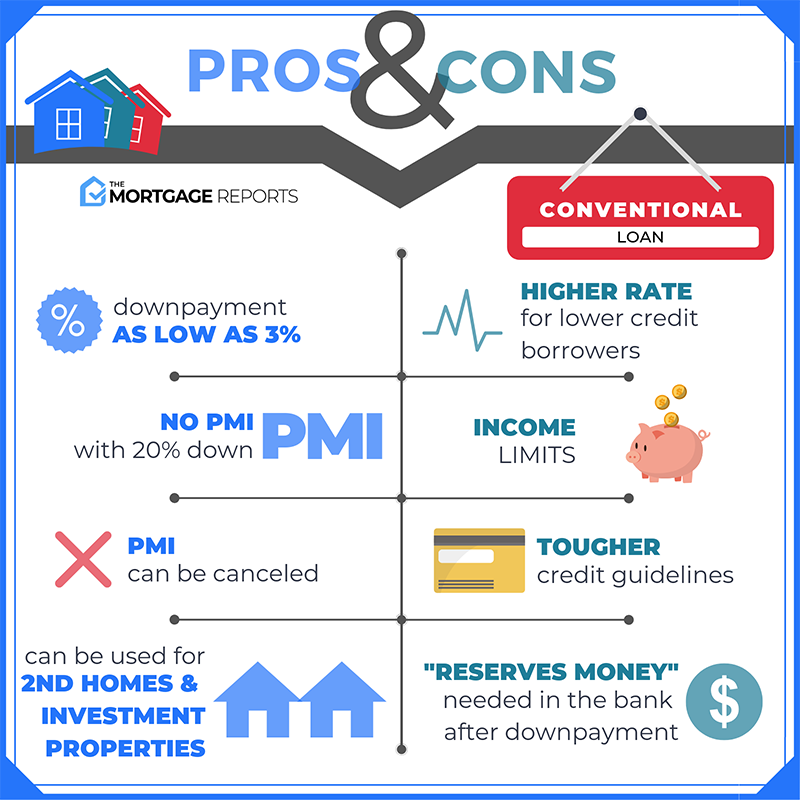

Most lenders offer conventional loans with PMI for down payments ranging from 5 percent to 15 percent. Some lenders may offer conventional loans with 3 percent down payments. A Federal Housing Administration (FHA) loan. FHA loans are available with a down payment of 3.5 percent or higher.

Why do realtors prefer conventional over FHA

Sellers often prefer conventional buyers because of their own financial views. Because a conventional loan typically requires higher credit and more money down, sellers often deem these reasons as a lower risk to default and traits of a trustworthy buyer.

How fast can you close on a conventional loan

It takes approximately 47 days to close on a conventional mortgage loan in accordance with Fannie Mae's qualified lending standards. Conventional refinances are faster and take around 35 days to close on average. Conventional mortgage loans follow the most traditional path from application through closing and funding.

Is it easier to qualify for FHA or conventional

FHA loans are usually easier to qualify for, requiring a minimum credit score of 580 to be eligible to make a 3.5% down payment. If your credit score is 500 to 579, you may qualify for an FHA loan with a 10% down payment.

What are red flags in the loan process

It's prudent to look for warning signs like: inconsistencies in the type or location of comparables. the house number in photos doesn't match the appraisal. the owner is someone other than the seller shown on the sales contract.

Is $25,000 enough for a down payment on a house

But for the most part, the minimum investment comes to 3% of the purchase price. Applying that percentage to the current median home price in California ($833,910) would equal a down payment of around $25,000.

Is a conventional loan good

In general, a conventional mortgage is ideal for borrowers with good credit that can provide a larger down payment. Conventional loans are more affordable in the long run and can be a smart investment for your future. There are two types of conventional mortgages: fixed rate and adjustable rate.

Why would a house only go conventional

Sellers often prefer conventional buyers because of their own financial views. Because a conventional loan typically requires higher credit and more money down, sellers often deem these reasons as a lower risk to default and traits of a trustworthy buyer.

Are conventional loans easier to close

Conventional Loans now Easier to Close

This is why these loans are often called conforming loans. But conventional loans are not quite a straightforward as one might think. Lenders typically don't approve conventional loan applications strictly by the set of rules published by Fannie and Freddie.

What is the 3 7 3 rule in mortgage

Timing Requirements – The “3/7/3 Rule”

The initial Truth in Lending Statement must be delivered to the consumer within 3 business days of the receipt of the loan application by the lender. The TILA statement is presumed to be delivered to the consumer 3 business days after it is mailed.

How much is a downpayment on a conventional loan

Home buyers can make a conventional down payment anywhere between 3% and 20% (or more) depending on the lender, the loan program, and the price and location of the home. Keep in mind that when you put down less than 20% on a conventional loan, you are required to pay private mortgage insurance (PMI).

What is the biggest red flag to potential money or credit lenders

You max out credit cards and only pay the bare minimum.

Behaviors like running up a lot of debt and paying off only the minimum monthly amount tells them that you lack discipline and may be on your way to getting in over your head financially.

What is considered a large deposit to an underwriter

A large deposit is defined as a single deposit that exceeds 50% of the total monthly qualifying income for the loan. When bank statements (typically covering the most recent two months) are used, the lender must evaluate large deposits.

Can I afford a 300K house on a $70 K salary

Home buying with a $70K salary

If you're an aspiring homeowner, you may be asking yourself, “I make $70,000 a year: how much house can I afford” If you make $70K a year, you can likely afford a home between $290,000 and $360,000*.