Is it worth paying off all your debt?

Is it bad to pay off all debt at once

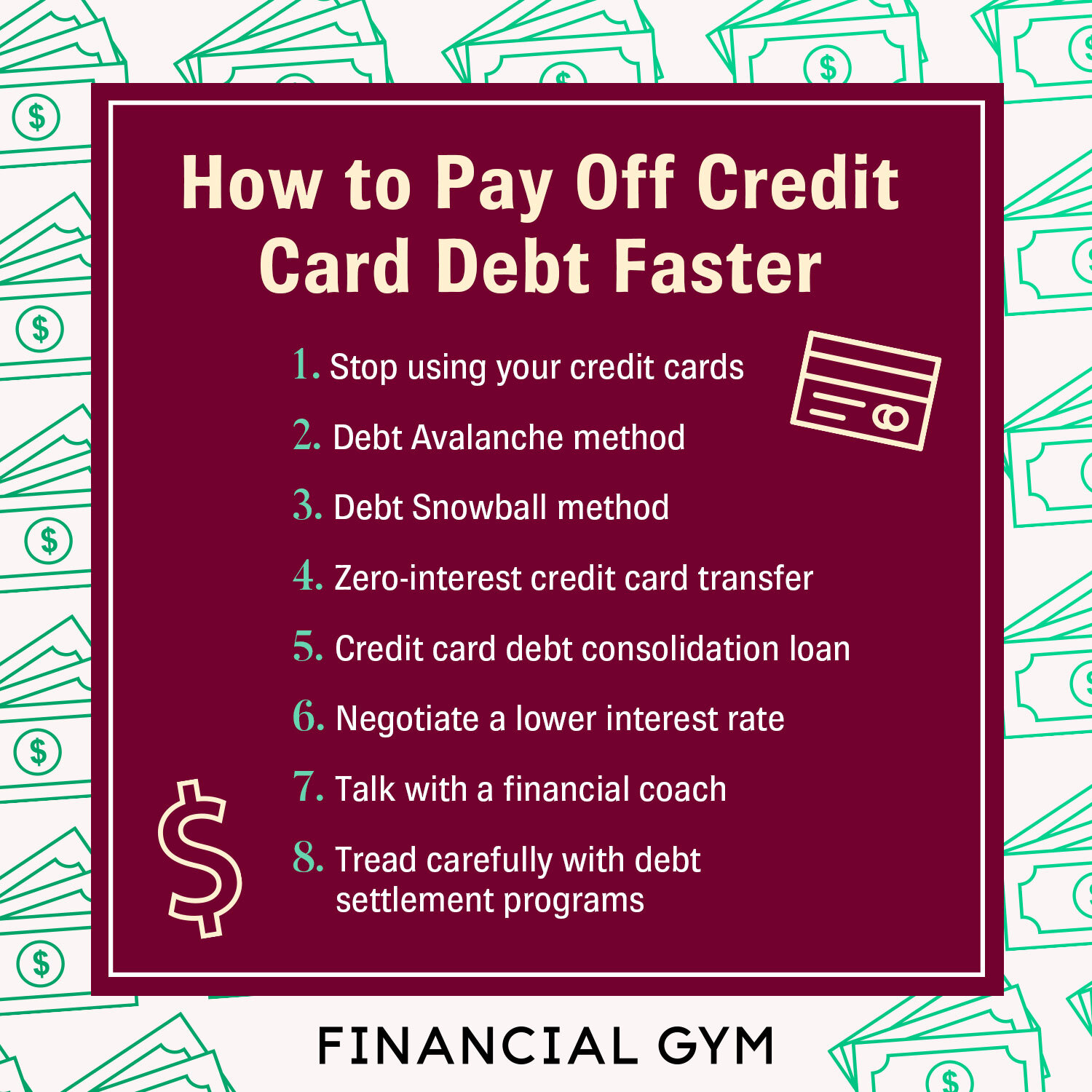

You may have heard carrying a balance is beneficial to your credit score, so wouldn't it be better to pay off your debt slowly The answer in almost all cases is no. Paying off credit card debt as quickly as possible will save you money in interest but also help keep your credit in good shape.

Cached

Is it better to pay off debt in full or settle

It's better to pay off a debt in full (if you can) than settle. Summary: Ultimately, it's better to pay off a debt in full than settle. This will look better on your credit report and help you avoid a lawsuit. If you can't afford to pay off your debt fully, debt settlement is still a good option.

Is it better to be in debt or debt-free

Financial experts agree that you should generally invest your extra cash rather than accelerate paying off low-interest debt, but still some people place immeasurable value on being debt-free or owning a debt-free home.

How much debt is too high

Generally speaking, a good debt-to-income ratio is anything less than or equal to 36%. Meanwhile, any ratio above 43% is considered too high.

What happens when all debt is paid off

Without any debts to worry about, your monthly expenses will drop, freeing up your personal cash flow and allowing you to focus on savings and daily living expenses. Few people understand just how free you can feel when you're no longer beholden to a slew of banks and lenders.

What are the disadvantages of paying off debt

ConsPrepayment penalties.Impact on your credit score.Miss out on an opportunity to pay off debt.

Does paid in full increase credit score

Paying off your credit card balance every month may not improve your credit score alone, but it's one factor that can help you improve your score. There are several factors that companies use to calculate your credit score, including comparing how much credit you're using to how much credit you have available.

At what age should you be debt free

The Standard Route. The Standard Route is what credit companies and lenders recommend. If this is the graduate's choice, he or she will be debt free around the age of 58.

How much debt is ok

A common rule-of-thumb to calculate a reasonable debt load is the 28/36 rule. According to this rule, households should spend no more than 28% of their gross income on home-related expenses, including mortgage payments, homeowners insurance, and property taxes.

Is $30,000 in debt a lot

Many people would likely say $30,000 is a considerable amount of money. Paying off that much debt may feel overwhelming, but it is possible. With careful planning and calculated actions, you can slowly work toward paying off your debt. Follow these steps to get started on your debt-payoff journey.

Is $20,000 a lot of debt

“That's because the best balance transfer and personal loan terms are reserved for people with strong credit scores. $20,000 is a lot of credit card debt and it sounds like you're having trouble making progress,” says Rossman.

Why debt-free is bad

Cons of Living Debt-Free

Without open accounts, there may not be enough credit activity for credit bureaus to calculate your score, which could harm your credit. Of course, that's not a problem if you don't want to play the credit game and have enough cash to take care of your financial needs.

What it feels like to be debt-free

Without any debts to worry about, your monthly expenses will drop, freeing up your personal cash flow and allowing you to focus on savings and daily living expenses. Few people understand just how free you can feel when you're no longer beholden to a slew of banks and lenders.

What is worse than being in debt

Worse than being in debt is losing your peace.

It's called being human. For some people that adversity takes the form of being in debt. The main thing is to keep your peace, to know that God is taking care of each of us, and to remember to trust Him to provide.

Why did my credit score drop 40 points after paying off debt

It's possible that you could see your credit scores drop after fulfilling your payment obligations on a loan or credit card debt. Paying off debt might lower your credit scores if removing the debt affects certain factors like your credit mix, the length of your credit history or your credit utilization ratio.

How to raise credit score 100 points in 30 days

Quick checklist: how to raise your credit score in 30 daysMake sure your credit report is accurate.Sign up for Credit Karma.Pay bills on time.Use credit cards responsibly.Pay down a credit card or loan.Increase your credit limit on current cards.Make payments two times a month.Consolidate your debt.

How much debt is normal

The average American holds a debt balance of $96,371, according to 2023 Experian data, the latest data available.

How much debt is the average 30 year old in

The average credit card debt for 30 year olds is roughly $4,200, according to the Experian data report. Compared to people in their 50s, this debt is not so high. According to Experian, the people in their 50s have the highest average credit card debt, at around $8,360.

How much debt is unhealthy

Debt-to-income ratio targets

Generally speaking, a good debt-to-income ratio is anything less than or equal to 36%. Meanwhile, any ratio above 43% is considered too high.

What is an OK amount of debt

A common rule-of-thumb to calculate a reasonable debt load is the 28/36 rule. According to this rule, households should spend no more than 28% of their gross income on home-related expenses, including mortgage payments, homeowners insurance, and property taxes.