Is paying off a loan a good idea?

Is it worth paying off a loan

Paying off your debt

If you are paying more for your borrowing than you're getting on your savings, then it makes sense to pay off your loans – so long as you can access funds in an emergency (see more on this below) and you'll not be charged high penalties for repaying your loan.

Is it good to pay off a loan early

Paying off your loan early can save you hundreds — if not thousands — of dollars worth of interest over the life of the loan. Some lenders may charge a prepayment penalty of up to 2% of the loan's outstanding balance if you decide to pay off your loan ahead of schedule.

What is the smartest way to pay off a loan

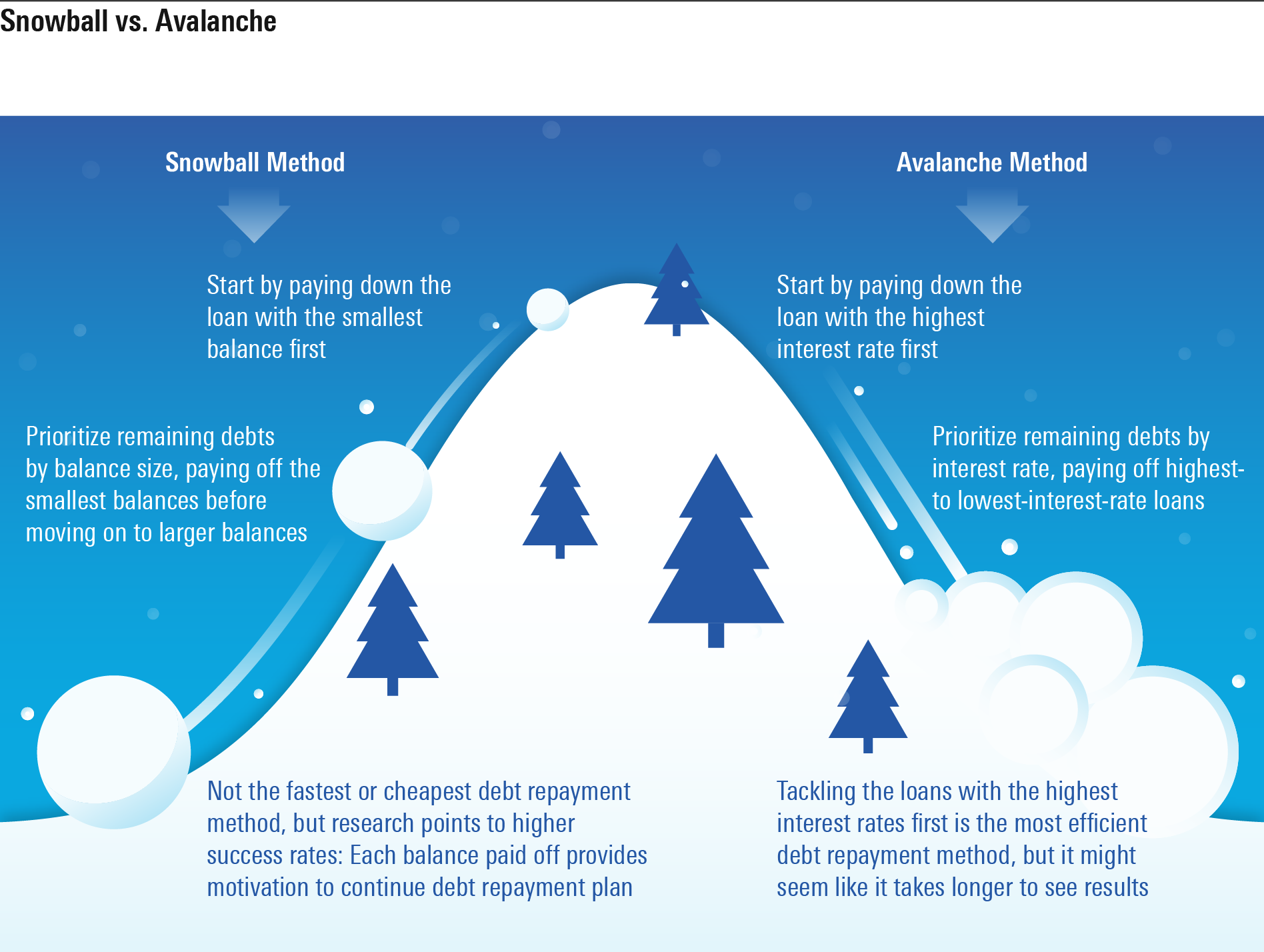

Pay off your most expensive loan first.

Then, continue paying down debts with the next highest interest rates to save on your overall cost. This is sometimes referred to as the “avalanche method” of paying down debt.

CachedSimilar

Is it better to pay off loans fast or slow

In most cases, paying off a loan early can save money, but check first to make sure prepayment penalties, precomputed interest or tax issues don't neutralize this advantage. Paying off credit cards and high-interest personal loans should come first. This will save money and will almost always improve your credit score.

CachedSimilar

Does paying off a loan hurt your credit

In short, yes—paying off a personal loan early could temporarily have a negative impact on your credit scores. You might be thinking, “Isn't paying off debt a good thing” And generally, it is. But credit reporting agencies look at several factors when determining your scores.

Does paying off a loan hurt your score

It's possible that you could see your credit scores drop after fulfilling your payment obligations on a loan or credit card debt. Paying off debt might lower your credit scores if removing the debt affects certain factors like your credit mix, the length of your credit history or your credit utilization ratio.

Does paying a loan build credit

Payment history: Getting a loan and making all of your monthly payments on time establishes a track record of responsibility. This is a primary factor in building a positive credit profile. Credit usage: How much debt you have — and what kind — is a reflection of how well you manage credit.

When you pay off a loan does your credit score go down

It's possible that you could see your credit scores drop after fulfilling your payment obligations on a loan or credit card debt. Paying off debt might lower your credit scores if removing the debt affects certain factors like your credit mix, the length of your credit history or your credit utilization ratio.

Is $20,000 debt a lot

“That's because the best balance transfer and personal loan terms are reserved for people with strong credit scores. $20,000 is a lot of credit card debt and it sounds like you're having trouble making progress,” says Rossman.

How to pay off $50,000 in debt in 1 year

What it takes to pay off $50,000 in debt in one year in 5 stepsThe benefits of paying off all your debt in a year.Tips to pay off $50,000 of debt in a year.Create a budget and track all expenses.Be mindful of debt fatigue.Prioritize paying high-interest debt first.Get a higher-paying new job.Freelance on the side.

Why did my credit score drop 40 points after paying off debt

It's possible that you could see your credit scores drop after fulfilling your payment obligations on a loan or credit card debt. Paying off debt might lower your credit scores if removing the debt affects certain factors like your credit mix, the length of your credit history or your credit utilization ratio.

How can I pay off $50000 in debt in one year

What it takes to pay off $50,000 in debt in one year in 5 stepsThe benefits of paying off all your debt in a year.Tips to pay off $50,000 of debt in a year.Create a budget and track all expenses.Be mindful of debt fatigue.Prioritize paying high-interest debt first.Get a higher-paying new job.Freelance on the side.

Why does credit score drop when a loan is paid off

This is because your total available credit is lowered when you close a line of credit, which could result in a higher credit utilization ratio. Additionally, if the account you closed was your oldest line of credit, it could negatively impact the length of your credit history and cause a drop in your scores.

Why did my credit drop after paying off loan

Lenders like to see a mix of both installment loans and revolving credit on your credit portfolio. So if you pay off a car loan and don't have any other installment loans, you might actually see that your credit score dropped because you now have only revolving debt.

Why does credit score go down after paying off loan

It's possible that you could see your credit scores drop after fulfilling your payment obligations on a loan or credit card debt. Paying off debt might lower your credit scores if removing the debt affects certain factors like your credit mix, the length of your credit history or your credit utilization ratio.

How long should I keep a loan to build credit

“If you have money to pay off the loan but want to build your credit, holding it for 12 to 24 months is ideal. By doing so, you won't accrue much interest but you will still build credit. That doesn't mean you have to get a 12- or 24-month loan, however.

What are the disadvantages of paying off debt

ConsPrepayment penalties.Impact on your credit score.Miss out on an opportunity to pay off debt.

Does paying a car loan off early hurt your credit

Paying off your car loan early can hurt your credit score. Any time you close a credit account, your score will fall by a few points. So, while it's normal, if you are on the edge between two categories, waiting to pay off your car loan may be a good idea if you need to maintain your score for other big purchases.

How much debt is unhealthy

Debt-to-income ratio targets

Generally speaking, a good debt-to-income ratio is anything less than or equal to 36%. Meanwhile, any ratio above 43% is considered too high.

How much is the average 25 year old in debt

Here's the average debt balances by age group: Gen Z (ages 18 to 23): $9,593. Millennials (ages 24 to 39): $78,396. Gen X (ages 40 to 55): $135,841.