What did TCJA eliminate?

What did the 2023 Tax Cuts and Jobs Act eliminate

Major elements of the changes include reducing tax rates for businesses and individuals, increasing the standard deduction and family tax credits, eliminating personal exemptions and making it less beneficial to itemize deductions, limiting deductions for state and local income taxes and property taxes, further …

Cached

What deductions were eliminated from the Tax Cuts and Jobs Act

Eliminated deductions include moving expenses and alimony, while limits were placed on deductions for mortgage interest and state and local taxes. Key expenses no longer deductible include those related to investing, tax preparation, and hobbies.

Cached

What did the TCJA eliminate for fringe benefits

Under the TCJA, companies may no longer deduct expenses that they incurred by supplying qualified employee transportation fringe benefits. These benefits generally include qualified parking, transit passes, certain types of highway transportation, and reimbursements for qualified bicycle commuting.

Cached

What are the major changes in the TCJA

Taxing Multinationals

The TCJA changed the U.S. corporate tax system from a worldwide one to a territorial one. This means U.S. corporations no longer have to pay U.S. taxes on most future overseas profits. Under the previous system, U.S. corporations paid U.S. taxes on all profits no matter where they are earned.

Cached

What did the TCJA do for corporations

TCJA allowed businesses to deduct the full cost of qualified new investments in the year those investments are made (referred to as 100 percent bonus depreciation or “full expensing”) for five years.

What significant changes did the Tax Cuts and Jobs Act of 2023 make to the taxation of US multinational corporations

One of the most significant provisions in the Tax Cuts and Jobs Act was the reduction of the U.S. corporate income tax rate from 35 percent to 21 percent. Over time, the lower corporate rate will encourage new investment and lead to additional economic growth.

Did the TCJA trimmed or eliminated many deductions and increased the standard deduction

How did the TCJA change the standard deduction and itemized deductions The Tax Cuts and Jobs Act nearly doubled the standard deduction and eliminated or restricted many itemized deductions in 2023 through 2025. It also eliminated the “Pease” limitation on itemized deductions for those years.

What expenses are no longer deductible

Expenses such as union dues, work-related business travel, or professional organization dues are no longer deductible, even if the employee can itemize deductions.

What are five fringe benefits which are exempt from taxation

Nontaxable fringe benefits can include adoption assistance, on-premises meals and athletic facilities, disability insurance, health insurance and educational assistance.

Which fringe benefits are excluded from taxation

Which Fringe Benefits Are Excluded From Taxes The IRS allows several fringe benefits to be excluded from taxes. This list includes (but is not limited to) benefits include adoption expenses, group-term life insurance, retirement planning services, and de minimis benefits, such as certain meals and employee parties.

How did the TCJA affect corporate taxes

In December 2023, Congress passed Public Law 115-97—commonly known as the Tax Cuts and Jobs Act (TCJA). Among many changes, TCJA lowered the top statutory corporate tax rate from 35 percent to 21 percent.

What are the changes in the TCJA 2023

Starting in the 2023 tax year, companies are no longer permitted to fully expense equipment in the year purchased. The “depreciation bonus” provision in the TCJA begins to sunset, with the allowable amount dropping to 80% this year and phasing out completely by 2026.

How did the Tax Cuts and Jobs Act of 2023 affect corporations

The 2023 Tax Cuts and Jobs Act made several large changes to business taxes, including permanently lowering the corporate income tax rate from 35 percent to 21 percent.

What changes did the Tax Cuts and Jobs Act TCJA make to the standard deduction how do you think this change will affect charitable giving in future tax years

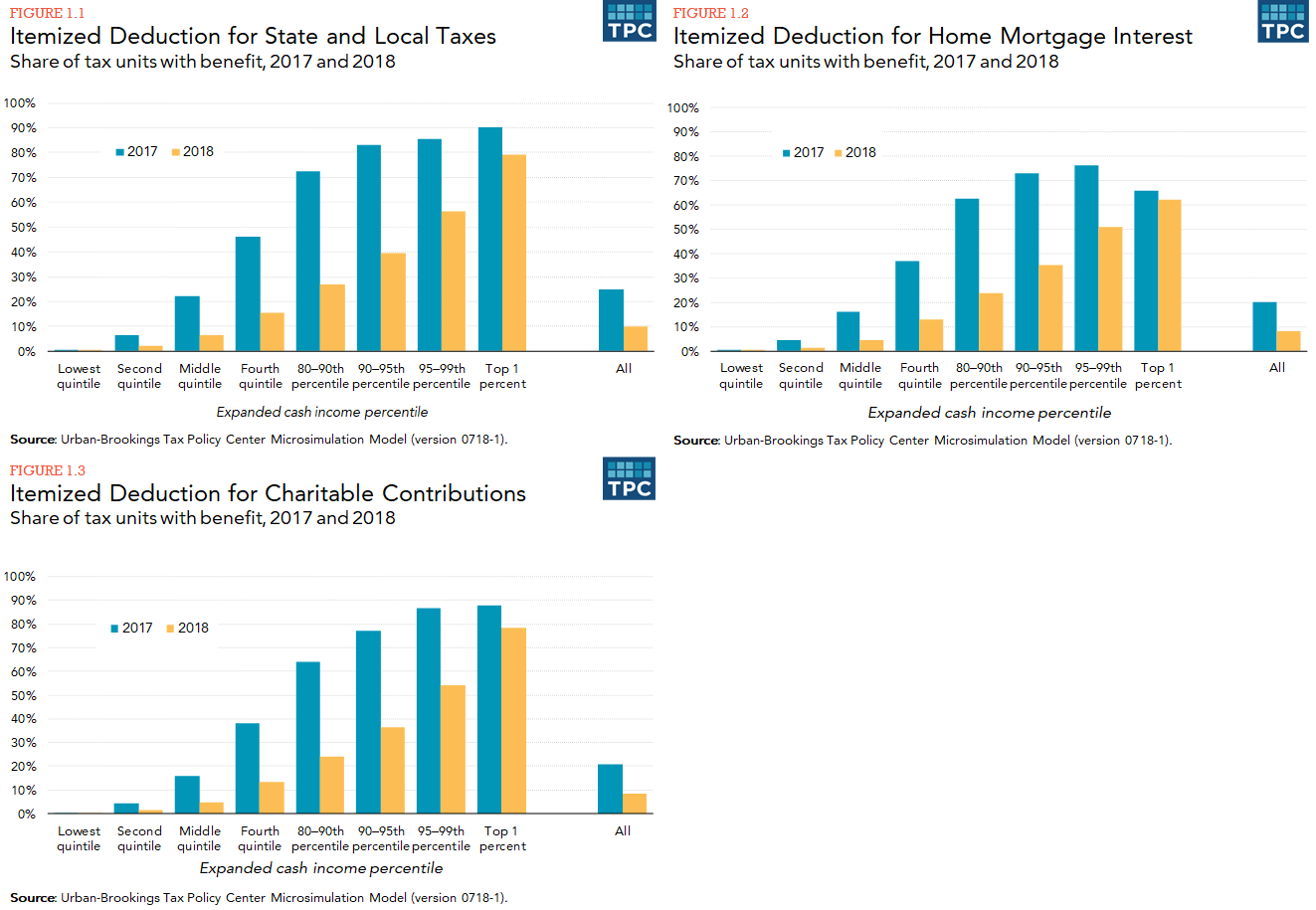

It increased the standard deduction to $12,000 for singles and $24,000 for couples, capped the state and local tax deduction at $10,000, and eliminated other itemized deductions—steps that significantly reduced the number of itemizers and hence the number of taxpayers taking a deduction for charitable contributions.

Did the 2023 Tax Cuts and Jobs Act eliminated the ability to recharacterize any conversions

In the past, you could change your mind and recharacterize that Roth conversion back to a traditional IRA. However, the Tax Cuts and Jobs Act (TCJA) of 2023 banned recharacterizing the account balance of a Roth conversion back to a traditional IRA. 5 Roth IRA conversions are now irrevocable.

What are the standard deduction amounts based on the TCJA tax law changes

Under the Tax Cuts and Jobs Act for the tax years beginning after December 31, 2023 and before January 1, 2026, the standard deduction has been increased for each filing status: $24,000 for married individuals filing a joint return, $18,000 for head-of-household filers, and $12,000 for all other taxpayers.

What itemized deductions are allowed in 2023

For 2023, as in 2023, 2023, 2023, 2023 and 2023, there is no limitation on itemized deductions, as that limitation was eliminated by the Tax Cuts and Jobs Act.

What expenses are 100% deductible

Here are some common examples of 100% deductible meals and entertainment expenses:A company-wide holiday party.Food and drinks provided free of charge for the public.Food included as taxable compensation to employees and included on the W-2.

What are three examples of excluded fringe benefits

Benefits not allowed.Archer MSAs. See Accident and Health Benefits in section 2.Athletic facilities.De minimis (minimal) benefits.Educational assistance.Employee discounts.Employer-provided cell phones.Lodging on your business premises.Meals.

What is considered a fringe benefit

A fringe benefit is a form of pay for the performance of services. For example, you provide an employee with a fringe benefit when you allow the employee to use a business vehicle to commute to and from work. Fringe benefits are generally included in an employee's gross income (there are some exceptions).