What is an 80% conventional loan?

What does 80 conventional loan mean

The first loan is a traditional mortgage that covers 80% of the home's purchase price. The second loan covers 10% of the home's price and is usually a home equity loan or home equity line of credit (HELOC) that effectively “piggybacks” on the first. The remaining 10% is paid with a cash down payment.

Cached

What is the 80% mortgage rule

The first mortgage covers 80% of the price of your home, the second mortgage covers 10% and the remaining 10% is your down payment. An 80-10-10 mortgage is designed to help you avoid private mortgage insurance and sidestep the standard 20% down payment.

Cached

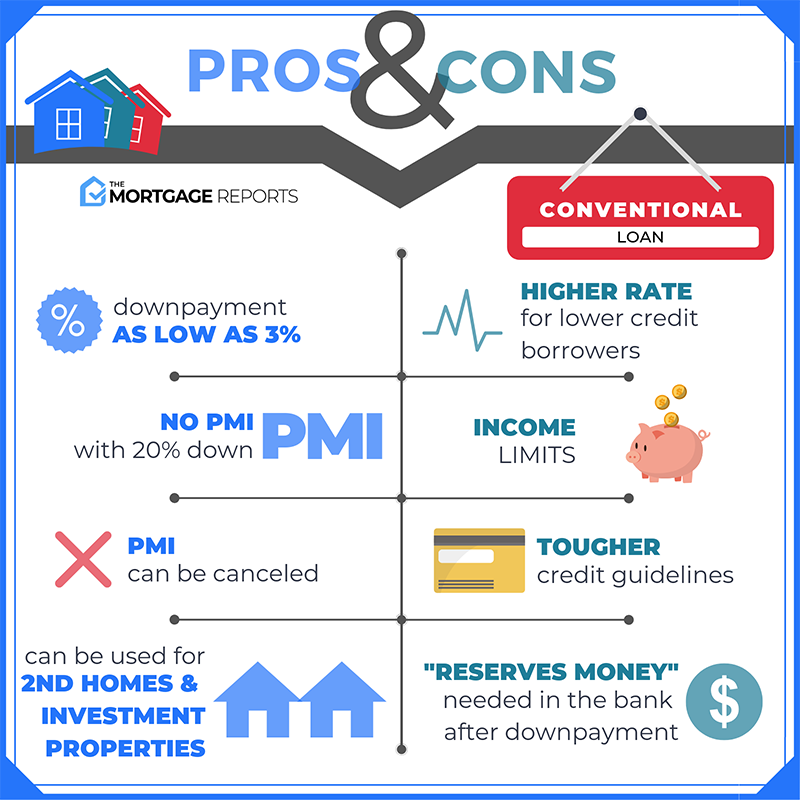

What’s a conventional loan mean

A conventional loan is any mortgage loan that is not insured or guaranteed by the government (such as under Federal Housing Administration, Department of Veterans Affairs, or Department of Agriculture loan programs). Conventional loans can be conforming or non-conforming.

What do conventional loans with a loan-to-value ratio that exceeds 80% generally require

If you're buying a house with a conventional loan—that is, a mortgage that's not backed by a federal program—an LTV ratio greater than 80% may mean you're required to buy private mortgage insurance (PMI), which covers the lender against loss if you fail to repay your loan.

What is the downside of a conventional loan

As noted above, conventional loans tend to have lower closing costs (and be cheaper in general) than government-backed options. However, the downside of conventional loans is that they don't offer as much flexibility to help you avoid paying those costs upfront.

Is it good to have a conventional loan

A conventional loan is a great option if you have a solid credit score and little debt. You can avoid needing to pay private mortgage insurance (PMI) by paying 20% of the loan upfront, which will lower your mortgage payments.

How does 80 15 5 mortgage work

The “80” refers to the first mortgage which finances the first 80% of the home's purchase price. The “15” refers to the second mortgage which finances another 15% of the purchase price. The “5” is the borrower's 5% down payment. There are two basic permutations to this: 80/15/5 or 80/10/10.

What is an 80 10 10 loan an example of

An 80-10-10 loan is a home loan that requires a 10% down payment. It's a common type of piggyback loan, which means that you actually take out two mortgages — the smaller one piggybacks on the bigger one.

Is a conventional loan good or bad

In general, a conventional mortgage is ideal for borrowers with good credit that can provide a larger down payment. Conventional loans are more affordable in the long run and can be a smart investment for your future. There are two types of conventional mortgages: fixed rate and adjustable rate.

What is a disadvantage of a conventional loan

Tougher credit score requirements than for government loan programs. Conventional loans often require a credit score of at least 620, which leaves out some homebuyers. Even if you qualify, you will likely pay a higher interest rate than if you had good credit.

What exceeds the conventional loan limit

If you need a home loan that exceeds the conforming loan limit for your county, you'll have to get a jumbo loan, which allows higher loan limits. However, these loans are typically harder to qualify for, requiring higher credit scores and larger down payments.

Which loan exceeds the conventional loan limit

jumbo loans

Conforming Loan Limit (CLL) VALUEs. Fannie Mae and Freddie Mac are restricted by law to purchasing single-family mortgages with origination balances below a specific amount, known as the “conforming loan limit” (CLL) value. Loans above this amount are known as jumbo loans.

Why would a buyer want a conventional loan

Conventional loans are ideal for borrowers with strong credit history, typically a credit score between 620 and 740, and a sum of money for about 20% of the down payment. Down payments that are less than 20% require private mortgage insurance (PMI). Your debt-to-income ratio (DTI) should be under 43%.

Are conventional loans good or bad

A conventional loan is a great option if you have a solid credit score and little debt. You can avoid needing to pay private mortgage insurance (PMI) by paying 20% of the loan upfront, which will lower your mortgage payments.

What is the downside to a conventional loan

As noted above, conventional loans tend to have lower closing costs (and be cheaper in general) than government-backed options. However, the downside of conventional loans is that they don't offer as much flexibility to help you avoid paying those costs upfront.

Is it better to have an FHA or conventional loan

A conventional loan is often better if you have good or excellent credit because your mortgage rate and PMI costs will go down. But an FHA loan can be perfect if your credit score is in the high-500s or low-600s. For lower-credit borrowers, FHA is often the cheaper option. These are only general guidelines, though.

What is a 70 30 mortgage

Example: you have found a house for $143,000. Your bank will lend you the mortgage money to buy the house at a 70/30 loan to value basis. This means to buy the house you will need to put up 30 percent of the total price, or approximately $43,000 as a down payment.

How to calculate 80% loan to value

For example, suppose you buy a home that appraises for $100,000. However, the owner is willing to sell it for $90,000. If you make a $10,000 down payment, your loan is for $80,000, which results in an LTV ratio of 80% (i.e., 80,000/100,000).

Can you avoid PMI with 10 down

How can I avoid PMI with 10 percent down If you can make a 10 percent down payment, you could avoid PMI if you use a second loan to finance another 10 percent of the home's purchase price. Combining these will satisfy your first mortgage lender's 20 percent down payment requirement, avoiding PMI.

Is it better to go conventional or FHA

A conventional loan is often better if you have good or excellent credit because your mortgage rate and PMI costs will go down. But an FHA loan can be perfect if your credit score is in the high-500s or low-600s. For lower-credit borrowers, FHA is often the cheaper option.