What is the 125% rule on investment bonds?

What is the 125% rule for bonds

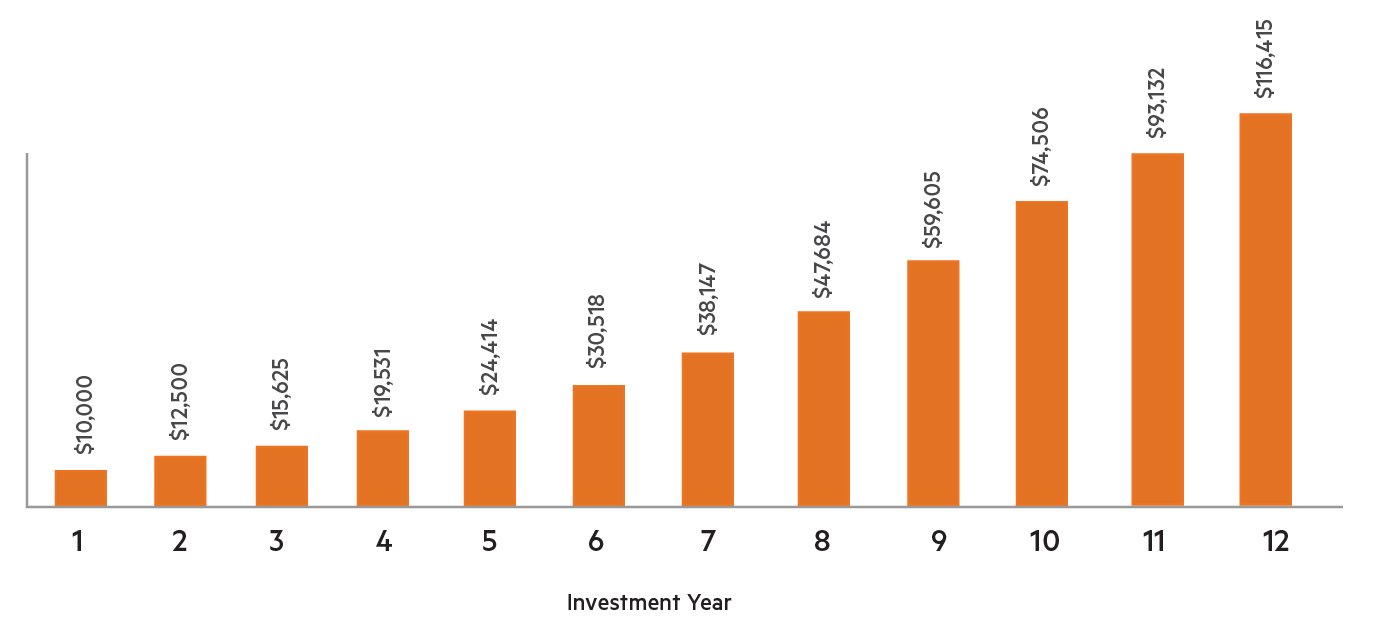

Effectively managing the 125% opportunity

If your contributions in an investment year exceed 125% of the previous investment year's contributions, your 10-year period will also re-start.

What is the 125% rule

This growth is effectively reinvested to deliver a compounding effect. Bonds have a valuable taxation status; as long as any additional investments you make do not exceed 125 per cent of the investments made in the previous year, then the taxation status will not be jeopardised. This is called the 125% rule.

What is the 10-year rule for investment bonds

If the investment bond is held for 10 years or more, there is no additional tax payable on the investment earnings. This is called the 10-year rule.

Do investment bonds form part of your estate

A bond provider may add interest for the period between the bond ending and the date the death claim is actually paid. This will be treated as income of the estate and will be subject tax at 20%. In addition the bond may contain a small amount life cover typically between 0.1% and 1% of the fund value.

How much of bonds should be in your portfolio

The rule of 110 is a rule of thumb that says the percentage of your money invested in stocks should be equal to 110 minus your age. If you are 30 years old, the rule of 110 states you should have 80% (110–30) of your money invested in stocks and 20% invested in bonds.

At what age should you stop investing in the stock market

You probably want to hang it up around the age of 70, if not before. That's not only because, by that age, you are aiming to conserve what you've got more than you are aiming to make more, so you're probably moving more money into bonds, or an immediate lifetime annuity.

How are investment bonds taxed

Individuals do not pay tax on their bond gains until a chargeable event occurs. This tax 'deferral' is one of the features that sets bonds aside from other investments. However, when a chargeable event does occur, a gain will be taxed in the tax year of that event.

Are investment bonds a good idea

BONDS are somewhat known as the steady Eddie of investments as they're comparatively low risk. And while they might not be as exciting as higher risk equities – including individual shares and equity funds – they have an important role to play in a well-diversified portfolio.

Do I bonds double in value after 20 years

EE Bond and I Bond Differences

The interest rate on EE bonds is fixed for at least the first 20 years, while I bonds offer rates that are adjusted twice a year to protect from inflation. EE bonds offer a guaranteed return that doubles your investment if held for 20 years. There is no guaranteed return with I bonds.

What happens after 20 years with an investment bond

Once the cumulative total of tax deferred withdrawals (i.e. those within the 5% allowance) is greater than the amount invested, all future withdrawals will be fully taxable. For someone, who has been taking 5% withdrawals from the outset this will mean withdrawals taken after 20 years will result in a chargeable gain.

Are investment bonds liable to inheritance tax

On the death of the last surviving policyholder, the bond can be inherited by a beneficiary of the policyholder's estate. There won't be any income tax to pay until the bond is surrendered or the last life assured dies but its value could be chargeable to inheritance tax.

What should a 70 year old retiree asset allocation be

At age 60–69, consider a moderate portfolio (60% stock, 35% bonds, 5% cash/cash investments); 70–79, moderately conservative (40% stock, 50% bonds, 10% cash/cash investments); 80 and above, conservative (20% stock, 50% bonds, 30% cash/cash investments).

What percentage of portfolio should be bonds in retirement

Once you're retired, you may prefer a more conservative allocation of 50% in stocks and 50% in bonds. Again, adjust this ratio based on your risk tolerance. Hold any money you'll need within the next five years in cash or investment-grade bonds with varying maturity dates.

How much should a 70 year old have in the stock market

If you're 70, you should keep 30% of your portfolio in stocks. However, with Americans living longer and longer, many financial planners are now recommending that the rule should be closer to 110 or 120 minus your age.

Should a 70 year old be in the stock market

Seniors should consider investing their money for several reasons: Generate Income: Investing in income-generating assets, such as stocks, bonds, or real estate, can provide a steady income stream during retirement. This can be especially important for seniors who no longer receive a regular paycheck from work.

How do I avoid paying taxes on bonds

You can skip paying taxes on interest earned with Series EE and Series I savings bonds if you're using the money to pay for qualified higher education costs. That includes expenses you pay for yourself, your spouse or a qualified dependent. Only certain qualified higher education costs are covered, including: Tuition.

Are I bonds taxed as income or capital gains

Is interest income from I bonds taxed as capital gains No, the interest income earned from I bonds is not considered a capital gain and is therefore taxed differently. Instead, it is taxed as regular income at the federal level and exempt from state and local taxes.

Is there a better investment than bonds

Historically, stocks have higher returns than bonds. According to the U.S. Securities and Exchange Commission (SEC), the stock market has provided annual returns of about 10% over the long term. By contrast, the typical returns for bonds are significantly lower. The average annual return on bonds is about 5%.

Are bonds a good investment in 2023

Longer-term bonds have yields of roughly 3.7% to 3.8%. Higher rates are good for 2023 bond returns for two reasons. One, even if rates stay where they are, you'll get a nice positive return from the interest your bonds generate.

Can I buy $10000 worth of I bonds every year

While there's no limit on how often you can buy I bonds, there is a limit on how much a given Social Security number can purchase annually. Here are the annual limits: Up to $10,000 in I bonds annually online. Up to $5,000 in paper I bonds with money from a tax refund.